Definitive Resource Covering The Homeowner’s Insurance Market

Americans Are Bailing On Their Home Insurance. Definitive Resource Covering The Homeowner’s Insurance Market

Some homeowners who are skipping coverage say they can no longer afford rising premiums.

Homeowners are increasingly forgoing home insurance, gambling that the likelihood of a disaster isn’t high enough to justify the cost of a policy.

Related:

How To Prepare For The Expected And Unexpected Costs of Homeownership

Emergency Rental Assistance Program

Home Flippers Pulled Out of U.S. Housing Market As Prices Surged

Housing Insecurity Is Now A Concern In Addition To Food Insecurity

Smart Wall Street Money Builds Homes Only To Rent Them Out

No Grave Dancing For Sam Zell Now. He’s Paying Up For Hot Properties

Investors Are Buying More of The U.S. Housing Market Than Ever Before

Biden Lays Out His Blueprint For Fair Housing

Housing Boom Brings A Shortage Of Land To Build New Homes

Wave of Hispanic Buyers Boosts U.S. Housing Market

Phoenix Provides Us A Glimpse Into Future Of Housing

OK, Computer: How Much Is My House Worth?

Sell Your Home With A Realtor Or An Algorithm?

Others, particularly among the wealthy, say they have enough money saved to rebuild or move elsewhere should their home be destroyed.

The risks of forgoing a policy are significant. When you don’t have insurance and your home is destroyed by fire, you don’t just lose your house and its contents. You might also have to pay for removing your home’s remains as well as the costs to rebuild it.

Few people can financially withstand the loss of an uninsured home, according to financial advisers. It is particularly precarious considering the high price to rebuild or buy a home in many areas of the country.

“It is a risky proposition to go without home insurance, and you need to fully understand the financial consequences if you lose your home,” says Noah Damsky, a financial adviser in Los Angeles.

A standard insurance policy typically covers the cost of replacement of the home and some of its contents in the event of damage or theft. Most mortgage lenders require borrowers to have home insurance, so those skipping a policy often own their homes outright.

In the past three years or so, more people who own their homes without a mortgage or who have inherited a home are opting to drop insurance because they can’t afford or can’t accept the current high price of home insurance, says Amy Bach, executive director at United Policyholders, a national nonprofit insurance consumer-advocacy group.

The Uninsured

Larry Farinholt hasn’t had home insurance in more than 25 years. He estimates he has saved more than $50,000 on his roughly 1,100 square foot Los Angeles home.

Farinholt, a 73-year-old retired public defender, didn’t renew his policy when he paid off his mortgage. He says he could have afforded a policy, but thinks the risk of wildfire or flood is very low in his neighborhood.

He has always had at least one dog to scare away unwanted visitors and has been burglarized once in more than 40 years.

“It would probably be financially devastating if I lost my house, but I have enough money in savings to move into a condo in that event,” says Farinholt.

Others opting to “go bare,” in industry parlance, say they are doing so because their policy hasn’t been renewed by their insurer as a result of increased risk of severe weather damage.

Owners might not want to get a state-run policy that typically offers higher premiums and less coverage.

Twelve percent of homeowners in the U.S. don’t purchase homeowners’ insurance. About half of them have annual household incomes of less than $40,000, according to a 2023 survey by Insurance Information Institute, an industry trade group, and the reinsurer Munich Re.

If a homeowner has a mortgage and doesn’t purchase insurance, the lender will typically buy lender-placed insurance for that property, says David Sampson, president and chief executive officer of the American Property Casualty Insurance Association.

Lender-placed insurance is generally more expensive than the coverage homeowners would buy for themselves, financial advisers say.

The higher cost of policies is a blow to both existing and hopeful home buyers.

Some borrowers are delinquent on mortgage payments and are blaming their late or missed payments on unexpected increases in their insurance premiums, says Rick Sharga, founder and CEO of CJ Patrick, a real-estate consulting firm.

Compared with around four years ago, mortgage lenders are more focused on factoring in higher insurance costs when determining how much of a mortgage a borrower can qualify for, Sharga says.

This is particularly the case in areas that are experiencing more natural disasters such as California and Florida.

Ultimately, this will bump some prospective buyers out of the housing market. They will either be unable to afford a home, or won’t qualify for a mortgage, Sharga says.

Creative Fixes

People with money are finding ways around the problem.

A client of Angie Newman in coastal Florida figured that the total cost of replacing his vacation home and all of its contents would be about $1.5 million. His longtime insurer recently didn’t renew his policy.

The only remaining insurer in the area was offering a policy with flood insurance for about $17,000 a year, up from about $7,000 a year that he paid previously, says Newman, a financial adviser at UBS Financial Services in Florham Park, N.J.

The client separated the possible costs of repairs and rebuilding from his other investible assets and invested the funds instead.

He assumed he could make an average return of about 6% on the roughly $1.5 million while waiting for some other insurers to re-enter the market, Newman says.

Updated: 6-22-2022

Lower Your Home’s Fire Risk (And Insurance) With These Steps

A new standard — already being adopted by one burned-out California town — will designate homes as “wildfire prepared” if they follow certain criteria.

Homeowners in the US got new guidance today to help them defend against increasingly frequent wildfires and associated rising insurance premiums.

The Insurance Institute for Business & Home Safety, a research nonprofit funded by insurers, announced it has developed the first ever standard that can demonstrably lower a home’s risk of wildfire damage.

To earn the Wildfire Prepared Home designation, homeowners have to meet a series of criteria — including, for example, clearing anything flammable like shrubs five feet around their homes — and pass an annual inspection.

The guidance will be particularly useful for homeowners in western US states that have been plagued by wildfires. The town of Paradise, California, 90% of which was leveled by the infamous 2018 inferno, immediately announced that all new construction would have to meet these standards.

“This is a critical piece to our rebuild,” said Kevin Phillips, Paradise’s town manager. “We are doing everything we can to show the insurance companies we are mitigating against risk and that we are a community that you would come back to and invest in.”

The state of California already has strict building codes for new construction in areas known to be fire prone, but many houses pre-date these standards and therefore do not conform to them. The steps for meeting the IBHS are even tougher.

For many years the IBHS has done research for the insurance industry on how to keep homes and business safer from fire, including by building test homes and setting them on fire in their laboratory.

But Roy Wright, chief executive of the institute, said in recent years homeowners across the west have become hungry for this information as well.

“The catastrophic events in California 2017 and 2018, changed that conversation about fire insurance,” he said. “All of a sudden, climate change

comes marching through the front door, these California families, they want to know what they can do.”

IBHS said the designation was based on the latest science and included a list of concrete steps proven to reduce fire risk, such as including and adding fine mesh coverings to attic vents or outdoor decks to prevent the spread of embers and replacing old roofs made of cedar shingles with a nonflammable material.

The widespread adoption of such standards would also be appreciated by the insurance industry. The industry lost 25 years of underwriting profits after the disastrous 2017 and 2018 fire seasons, according to Milliman Inc, a risk assessment firm that works with insurers, and has been pushing for stricter building codes around fire.

It has also been raising rates in fire prone areas and pulling out entirely in some cases.

While there is currently no guarantee that meeting the IBHS standard will result in a decrease in insurance rates, new draft regulations from the California Bureau of Insurance include language indicating that insurance companies would have to give discounts to homes that meet this standard.

It might be costly and difficult to achieve higher fire standards, particularly for older homes, but Phillips said that for towns like Paradise, where insurance premiums can now top $6,000 a year, it is the only way forward.

“Even if it is a little more expensive” up front, he said, “the long term benefit is going to help make it the most affordable.”

Updated: 8-25-2023

Rising Insurance Costs Start To Hit Home Sales

Vulnerable areas on coasts are first to feel impact of higher premiums.

Cape Coral, Fla., was devastated by Hurricane Ian last year, but real-estate agents still pitch waterfront homes as “Gulf access haven.”

Insurers take a different view. Home-insurance premiums are soaring in the Southwest Florida city, and there is evidence that the higher costs are starting to affect the real-estate market.

Buyers’ concerns about insurance costs are slowing sales and causing some canceled deals in areas with particularly high flood or wildfire risks.

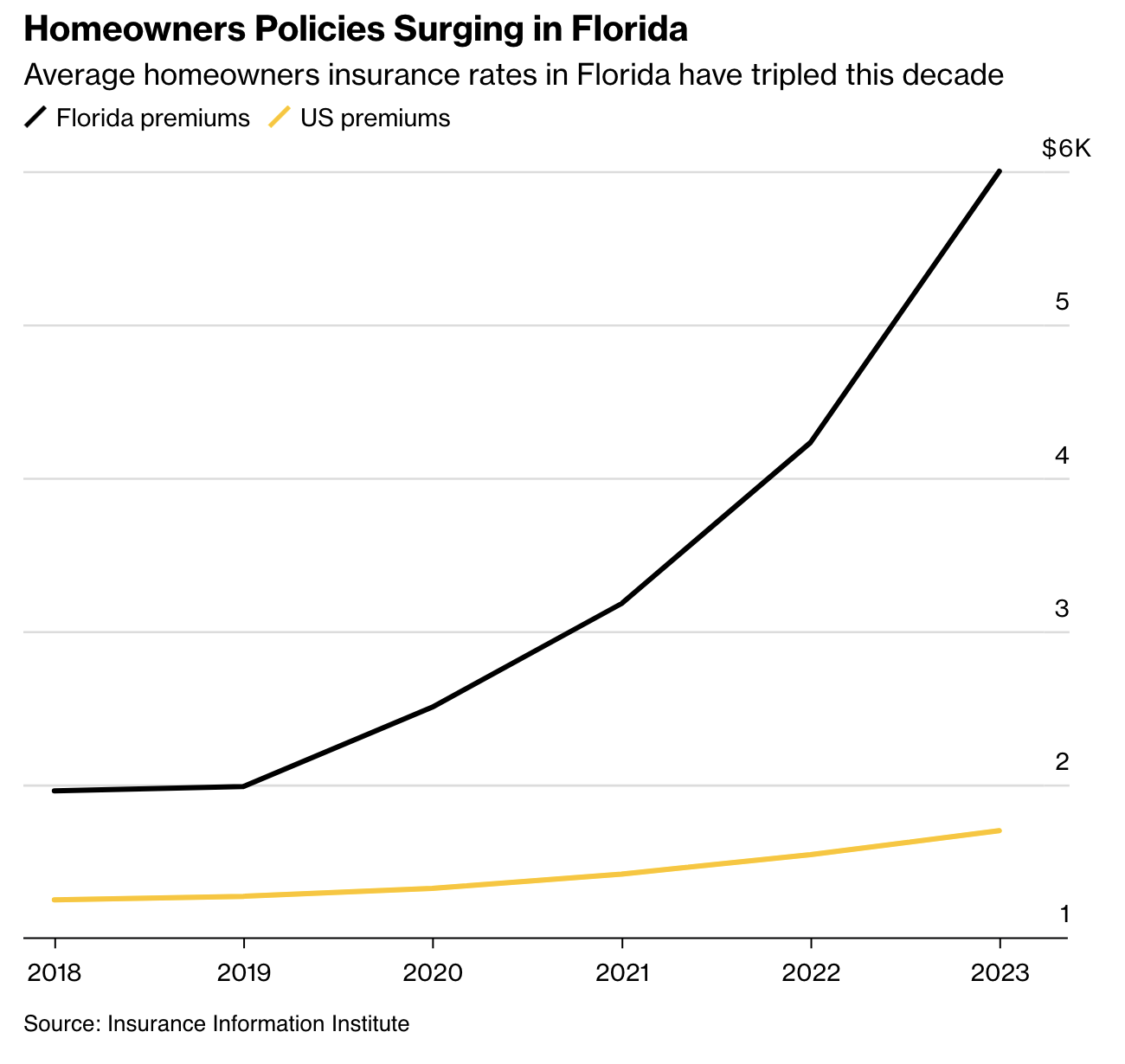

Home-insurance companies are trying to claw back steep underwriting losses by hiking rates, or pulling back from disaster-prone areas such as Cape Coral. The average annual home-insurance premium for Floridians has tripled in five years, from $1,988 in 2019 to $6,000, according to the Insurance Information Institute, an industry group.

The cost of flood insurance—mandatory for some in the Sunshine State—is rising faster still in many vulnerable areas. The federal National Flood Insurance Program, which provides most policies, recently changed its pricing to more closely tie premiums to risk. In Cape Coral, the average annual flood-insurance premium for a waterfront zip code has increased from $1,791 to $4,728 a year, federal data show.

Chance Hazeltine, a Sarasota, Fla.-based agent for Goosehead Insurance said flood rates in the Cape Coral area can be three or four times higher under the new system. While the local property market remains buoyant, he added, “at some point, as the cost to own the asset goes up, it’s going to affect its resale value.”

Higher insurance costs haven’t stopped Americans flocking to disaster-prone areas. Lower taxes, cheaper housing and sunnier weather have outweighed any concerns over floods or fires.

In the past two years, a net 60,000 people moved to Lee County, which includes Cape Coral, according to a study by online real-estate brokerage Redfin.

Nationally, the counties with the highest risks of wildfires and floods also enjoyed a collective postpandemic net bump in population, the study found.

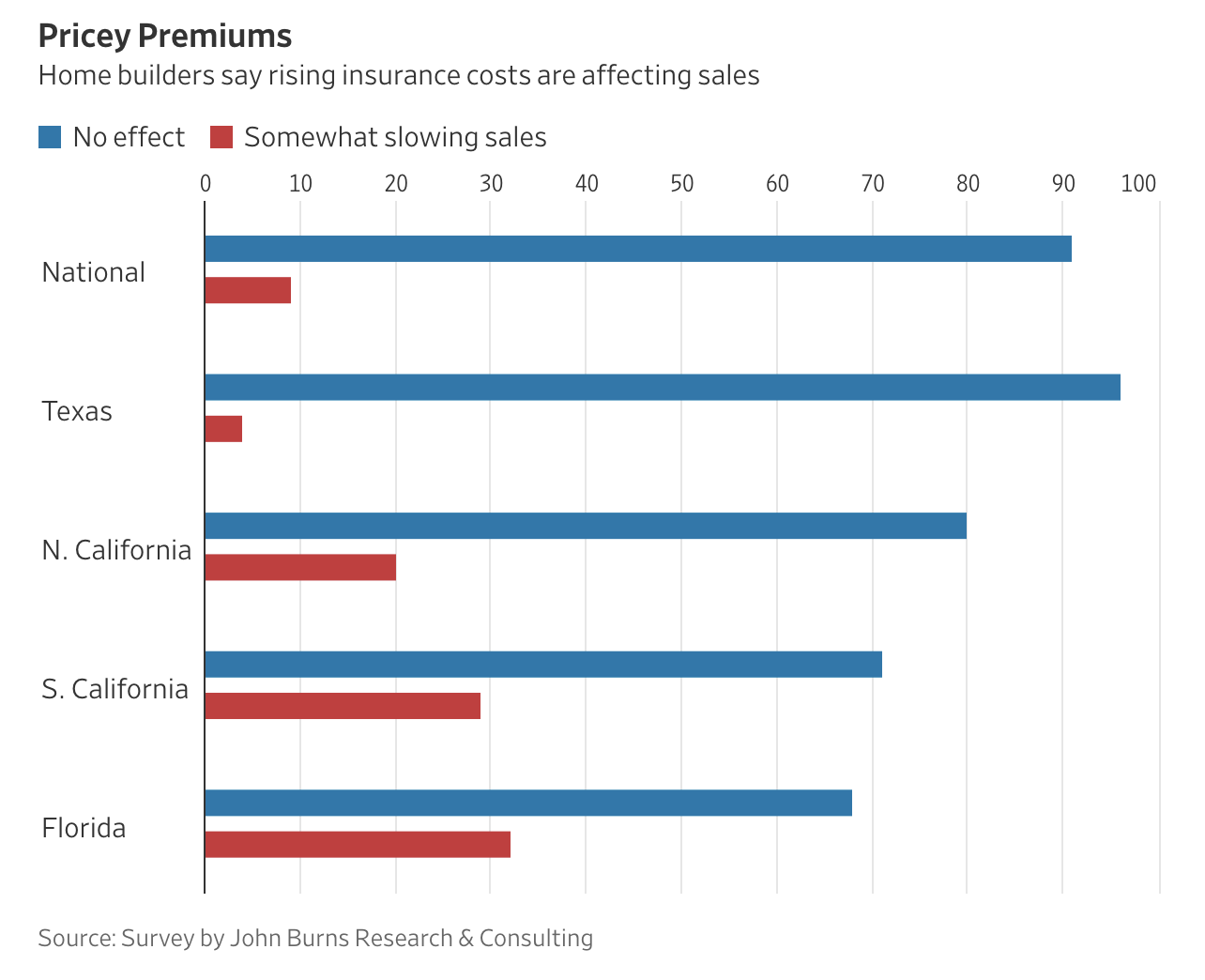

There are signs that buyers are growing more cautious. In a recent survey, almost a third of house builders in Florida said buyers’ concerns about home insurance were “somewhat slowing sales.”

The proportion in Southern California was very similar, at 29%, the survey by John Burns Research & Consulting found. That is much higher than the national figure of 9% of builders reporting sales affected by insurance concerns.

“Insurance is absolutely having an impact on house purchases—and that’s going to continue to happen,” said Alexandra Glickman, the Los Angeles-based global head of real estate and hospitality at insurance broker Arthur J. Gallagher.

She cited an example of a client who was considering buying a $13.5 million home in the Pacific Palisades, an affluent region of Southern California tucked between the Santa Monica Mountains and the Pacific Ocean.

The home-insurance premiums quoted were $100,000 to $300,000 a year. As a result, the client decided not to go ahead with the deal, Glickman said.

The cost “is laying a damp towel” on buyer enthusiasm for disaster-prone locations, Glickman added.

The risks of disasters haven’t been fully priced into property markets, partly because of flaws in the way federal flood insurance was priced, researchers say.

If flood risks were taken into account, U.S. residential properties would be worth at least $121 billion less, according to a study earlier this year by nonprofit the First Street Foundation, the Federal Reserve and others.

In Florida alone, properties in flood zones are overvalued by more than $50 billion, the study found.

Fewer than five million people have federal flood insurance, according to government data. Even in the highest-risk areas, on average 30% of homes have policies, a study by the Wharton School at the University of Pennsylvania found.

Flood insurance is required for homes in high-risk flood zones with government-backed mortgages.

The relatively small numbers mean the pricing change is “not likely enough to tip the scale” against continuing construction of new homes in flood plains, according to Susan Asmus, head of regulatory affairs for the National Association of Home Builders.

The most affected spots are likely to be lower-income regions. The flood-insurance program’s new pricing system “will have devastating consequences for the Louisiana housing market,” said Nicholas Hebert, chairman of the Houma-Terrebonne Chamber of Commerce in the southeastern part of the state, in a filing that is part of a 10-state lawsuit seeking an injunction against the new flood-pricing system.

Hebert said the premium for his own home, which is more than 30 miles from the coast, is set to rise the maximum permitted of 18% a year until it hits $7,000, from the current $790.

Local lender Gulf Coast Bank & Trust has “already experienced sales contracts being canceled before the loan application was even complete,” due to higher flood-insurance costs, according to Louis Uzee, head of its residential-mortgage division.

He fears sky-high insurance rates will lead to more people being unable to afford to stay in their homes.

David Maurstad, the senior executive for the National Flood Insurance Program, said the new pricing system would help people in lower-risk states.

If it was stopped, “policyholders in 40 states would have to pay more so that policyholders in the high flood risk areas of Louisiana, Florida, Mississippi, and Texas could pay a lot less,” he wrote in a court filing this month seeking to have the states’ lawsuit tossed.

The law doesn’t give the Federal Emergency Management Agency, which runs the flood program, any authority or discretion to address the affordability concerns of policyholders, he added.

Updated: 9-11-2023

What Rising Rates And Surging Insurance Prices Are Doing To Real Estate

In some respects, the real estate market has been surprisingly resilient in the face of rising interest rates. Homebuilders have generally performed well and home prices have not tumbled the way many might have expected.

But looked at in another light, rising interest rates and reduced credit availability mean some real estate projects that might have made sense a year or two ago are no longer penciling out.

On this episode of the podcast, we speak with David O’Reilly, the CEO of Howard Hughes Holdings, a major publicly-traded real estate developer with Master Planned Communities all over the country.

Thanks to the company’s role in the real estate market, David has perspective on all aspects of real estate, from housing to offices to retail development. We discuss the impact of higher rates, costlier insurance, and inflation.

Updated: 9-18-2023

Homeowners Take Risks To Lower Their Insurance Bills

Higher deductibles can lower insurance premiums—but they are a gamble.

Homeowners in search of relief from rising insurance bills are offering to pay more out of pocket in the event of fire, theft or other damage to their property.

In practice, consumers are doing this by raising their deductible. A deductible is the amount paid by a policyholder before insurance kicks in. Higher deductibles generally mean lower premiums, but it is risky.

While the standard home-insurance deductible typically ranges from $500 to $1,000, according to an analysis of millions of policies by digital insurance marketplace Matic Insurance, more homeowners are choosing higher deductibles.

The number of new policies with $2,000 to $2,500 deductibles nearly tripled from 2019 to August of this year. The number of policies with $500 deductibles fell by about two-thirds during that time.

The decision to increase their deductible comes as the national average for home-insurance premiums based on $250,000 in dwelling coverage increased this year to $1,428 annually, up 20% from 2022, according to Bankrate.

Boosting their deductible is one of the few strategies homeowners can use to reduce their premiums and keep their home insured as inflation continues to put pressure on their budgets.

Even shopping around has a limited benefit since rising construction costs and natural disasters are leading nearly all insurers to raise their prices and cover less.

“Homeowners are desperately looking for ways to save on their premiums right now,” said John Costello, former chairman of the Independent Insurance Agents and Brokers of America, a national trade association.

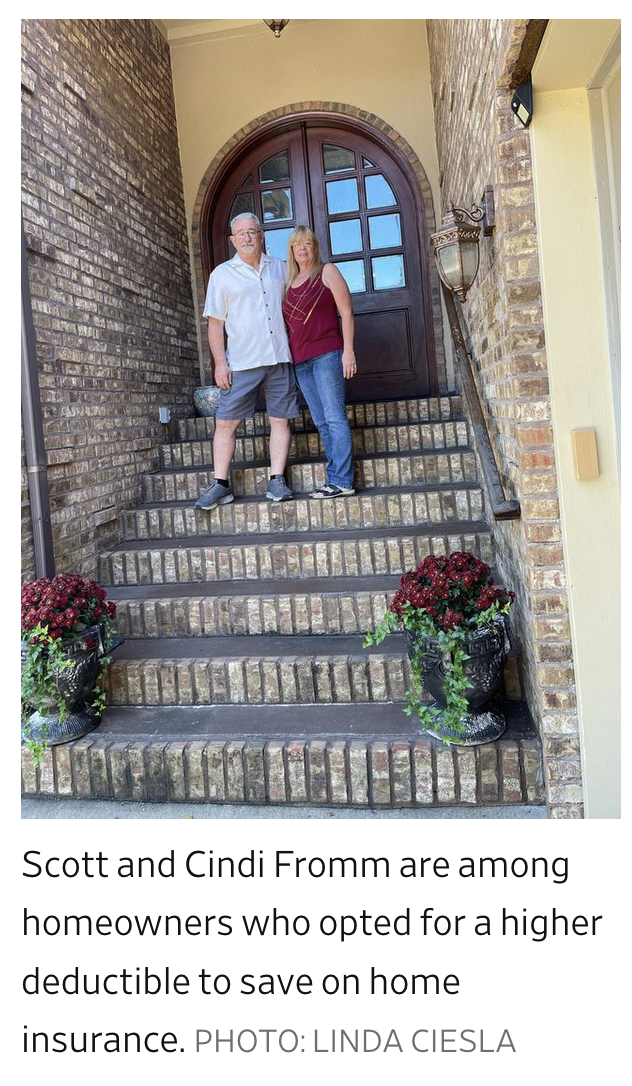

Scott and Cindi Fromm’s home-insurance premium rose to $2,700 from $1,600 a year. The Bella Vista, Ark., retirees hadn’t made any claims on their policy with a $5,000 deductible, but their insurer said roof damage in the area from hail was pushing premiums higher.

The Fromms switched their home-insurance policy to a new carrier, with a $10,000 annual deductible and a $1,100 yearly premium. They said they have enough savings should they have to foot the bill for $10,000 of damage before their insurance starts to cover repairs.

“We think in the long run, the high-deductible strategy will pay off for us, especially as we invest the savings,” Scott said.

Raising your deductible to $1,000 from $500 might decrease the cost of your homeowner’s insurance by 6%, on average, according to a recent analysis by insurance-research site ValuePenguin.com.

Some homeowners are choosing to increase their deductibles unprompted, while others are being effectively nudged by their insurance companies to consider the higher-deductible policies, say homeowners and insurance companies.

More people have dropped their coverage entirely. As of June of this year, 88% of owners carry homeowner insurance nationally, down from 95% in 2016, according to the Insurance Information Institute, also known as Triple-I.

How much you save on home insurance by increasing the deductible depends on your insurance company, where you live and claims history, said Loretta Worters, a spokeswoman at Triple-I.

While high deductibles can help lower costs, your premiums may still rise, she said.

Understand Your Deductibles

Standard homeowners insurance covers wind and hail damage from storms and hurricanes. Flood and earthquake policies are typically purchased separately.

But each of these natural disasters has its own deductible rules. If you live in an area with a high risk for one of these disasters, there are different deductibles, said Worters at Triple-I.

For instance, whether a hurricane deductible applies to a claim depends on the specific “trigger” selected by the insurance company.

These triggers vary by state and insurer and usually apply when the National Weather Service or National Hurricane Center officially names a tropical storm, declares a hurricane watch or warning, or defines a hurricane’s intensity in terms of wind speed, said Worters.

Hurricane deductibles are generally higher than traditional dollar deductibles and usually take the form of a percentage of the policy limits. For example, in Florida, most insurance policies have a hurricane deductible of 2% to 10% of a home’s insured value.

Homeowners are typically able to raise their standard homeowners deductible, but they don’t always have that option with a percentage deductible, Worters said.

Homeowners can find their deductible amounts on their insurance policy’s declaration page.

Consider The Risks

With severe weather and natural disasters on the rise, it is risky to raise your deductible if your home might be vulnerable to damage, said Pat Howard, property and casualty insurance specialist at Policygenius, an online insurance broker.

If you live in an area where the chance of expensive home damage is low and you haven’t had to file a claim in the past, it might be worth boosting your deductible to lower your premiums, said Howard.

Prepare For The Upfront Expense

A higher-deductible option can help you save on monthly premiums, but make sure you can afford to pay for damage before your insurance starts to cover repairs.

For example, if you have a $5,000 deductible and your home gets $4,500 in hail damage, you will have to pay for the repairs out of pocket.

Many losses, including post-hurricane roof damage, often won’t rise to a level above the deductible, which means the homeowner will need to absorb the entire cost of the repair, said Harold Lewis, a real-estate lawyer in Miami.

You will want to be able to pay for the repairs without running up high-interest credit-card debt, financial advisers say.

Consider saving more than the deductible amount in an emergency fund, said Noah Schwartz, a financial planner in Newtown, Conn.

Updated: 10-17-2023

Home Insurance Is So High In This Florida Town, Residents Are Leaving

In West Palm Beach’s Flamingo Park neighborhood, some homeowners are dropping insurance, and others who can’t are selling.

WEST PALM BEACH, Fla.—James and Laura Molinari left Chicago for a two-story stucco home in this city’s historic Flamingo Park neighborhood. The four-bedroom house was a short bridge away from Palm Beach island and walking distance to downtown West Palm Beach.

“We love it here,” said James, who plays golf with his 3-year-old son on Saturdays and can swim year-round in his backyard pool.

Then the renewal for his home insurance arrived. The new rate for the year starting in September was around $121,000—more than seven times what the Molinaris said they paid last year, and more than 13 times what they paid when the family moved to Florida in 2019.

While they found a better rate from another insurer, at about $33,000 it is still nearly double what they paid last year. The family this month listed the home for sale with an asking price of nearly $3.5 million after determining that insurance costs made staying there too expensive. Others in Flamingo Park told The Wall Street Journal they are drawing the same conclusion.

“The for-sale signs are going up left and right,” James said of the neighborhood.

Florida’s explosion in insurance premiums threatens to ground the state’s highflying housing market. Florida home prices soared more than 60% since 2019, according to real-estate brokerage Redfin.

That rate has slowed more recently, and the state’s home prices in September edged up 2.7% over the previous year, Redfin said.

While rising interest rates and the large price run-up are the biggest factors, higher insurance costs are starting to play a role, brokers say.

Home-insurance costs are rising everywhere, but they are rising especially fast in Florida where premiums have tripled in the past five years. Some premiums have increased by about nine times what they were last year, according to Oscar Seikaly, chief executive of NSI Insurance Group, who said he has handled insurance premiums that cost as much as $600,000 a year for multimillion-dollar homes.

“When you have a home that’s one million dollars or less, your insurance premium becomes higher than your mortgage,” he said.

A combination of extreme weather events, higher costs to rebuild and a rise in litigation has put the state’s insurance industry into crisis. Multiple insurers have pulled out of the state altogether.

Gov. Ron DeSantis last year signed a bill meant to reduce some of the litigation and bring insurance costs down, but many in the industry say it isn’t enough.

The surge in insurance premiums has led many people who own their homes outright to drop insurance. While some of these homeowners without mortgages have gotten rid of all their insurance, others have dropped only their wind coverage, which pays off after a hurricane and where the prices have risen the fastest. Newer homes generally have experienced smaller run-ups in insurance costs.

In few places are soaring premiums more apparent than in Flamingo Park, where a combination of older, historic homes and ballooning property values have caused insurance costs to double for many homeowners in the past year.

Even though the West Palm Beach neighborhood resides on a coastal ridge, where most of the homes are well above sea level and outside the flood zone, insurance rates for wind coverage are soaring there.

Mortgage lenders typically require borrowers to take out home insurance. But in Flamingo Park, more than a dozen homeowners who have paid off their mortgage said they have dropped some of their insurance coverage this year because they could no longer afford—or stomach—the payments.

Those who go without it are taking a risk, especially in a state where powerful tropical storms and hurricanes are a frequent occurrence. The homeowner could be on the hook not only for the house if it is destroyed by a weather event, but also for all contents and any costs related to removing what remains.

Even so, Pete and Susan Sinclair say that everyone they know in Flamingo Park who owns a home outright has dropped hurricane insurance.

The Sinclairs bought a 1,000-square-foot New England-style cottage in the West Palm Beach neighborhood 18 years ago. When their renewal came in at around $10,000 this year, up 40% from last year, they decided to drop their insurance and “go bare,” as the practice is known.

“It’s lunacy. You feel like you’re being played for a fool,” said Pete, 72 years old, a retired boat painter.

“If the house does blow over, we can sell the land and move on,” Susan said.

Even the mayor of Palm Beach County, Gregg Weiss, who lives in the neighborhood, decided to drop his insurance when the premium doubled to about $20,000. Instead of paying the insurance, he paid off what was left on his mortgage.

“I know a lot of people who have done the same thing,” Weiss said. “The market doesn’t make sense anymore.”

Scott Smith, 51, moved to the neighborhood from Atlanta three years ago. His insurance doubled to around $14,000 this year. When he first moved to Florida, he was surprised to learn that his insurer in Atlanta didn’t operate in the state. If he is unable to bring down his premium this year, he says he will probably have to sell.

“This is robbery,” he said, adding that he paid only about $2,000 in insurance for a $2 million home in Atlanta. “Between taxes and home insurance, it is more than what we pay in our mortgage.”

Updated: 11-12-2023

The Coastal State Where Home Insurance Is Relatively Affordable

Homeowners in Alabama have a stable market thanks in part to the way some homes are built there.

MOBILE, Ala.—When Kelly and Mike Francis saw the home-insurance quotes for the house they wanted to buy here last spring, they had sticker shock.

The couple decided to take out a different policy from a little-known insurer that included reduced coverage of an aging roof, which made the house vulnerable to hurricanes and other fierce weather that batter the Gulf Coast.

At about $4,500 a year, it was cheaper than a comprehensive policy, but they could still barely swing it.

Now they are poised to secure a comprehensive policy from an established carrier, along with a roughly $1,000 discount on their premium, thanks to a new storm-resistant roof they had installed in September with the help of a $10,000 grant from a state program.

Financially, “it lets us breathe more,” said Kelly Francis, 34 years old.

This state is bucking a national trend. Home insurers across the U.S. are insuring less and charging more as they try to claw their way back to profitability after losing money in recent years.

Premiums have skyrocketed in Florida. And in some parts of the Gulf and East coasts, carriers are pulling back.

A driving force keeping Alabama’s insurance market in check, according to industry specialists, is that it leads the nation in building homes and roofs like the one now atop the Francis home.

Their roof complies with a set of resilience standards developed by the Insurance Institute for Business & Home Safety, or IBHS, a research group funded by insurers.

“At a time when there’s tremendous tumult in the Gulf Coast insurance marketplace, coastal Alabama has stability and predictability,” said Roy Wright, chief executive of IBHS.

Dubbed the Fortified program, its so-called Gold specifications exceed those of most state and local building codes and include elements such as sealing roof decks, installing impact-resistant windows and doors, and tightly fastening roofs to walls.

Alabama has embraced the program—with a tally of about 43,000 Fortified homes and roofs so far, making up more than 80% of all such construction in the U.S.

Alabama’s efforts illustrate a promising response to an issue confronting many U.S. coastal areas: how to make homes more resilient in the face of stronger storms brought in part by climate change, and to persuade insurers to keep providing coverage for them.

Failure on either front could threaten real-estate markets and residents’ ability to continue living in vulnerable areas.

Alabama frequently is struck by hurricanes and tropical storms but, because of its smaller coastline, less than Florida and Louisiana.

Alabama’s coastline comprises two counties—Mobile and Baldwin—that are home to large shipbuilding and aerospace employers, rapidly growing residential developments and beaches popular with tourists.

Home-insurance premiums in the counties have fluctuated but generally declined in recent years, according to data compiled by Lars Powell, director of the Alabama Center for Insurance Information and Research at the University of Alabama.

The average premium was $1,243 in 2021, the most recent year for which data is available, compared with $1,396 in 2015.

In Florida, the average premium tripled from 2019 to 2023, when it reached $6,000, according to the Insurance Information Institute, an industry group.

Alabama’s insurance market faces some of the same challenges as those of other coastal states, including the rising cost of reinsurance—backup coverage insurers buy—said Mark Fowler, Alabama’s insurance commissioner.

Though some insurers have retrenched, most large national carriers continue to write policies for homes built to Fortified standards in coastal Alabama, he said.

The Alabama market is sufficiently competitive that homeowners can shop around for policies and receive multiple quotes.

Carl Schneider, an insurance agent based in Mobile, said the availability of home insurance in Alabama is much greater than in other areas where his agency operates, including Mississippi, Louisiana and the Florida panhandle.

State-backed insurers of last resort in troubled markets such as Florida and Louisiana have absorbed a surge of new customers as private carriers retreat, but the equivalent entity in Alabama has experienced more moderate growth.

In August, the Alabama Insurance Underwriting Association had nearly 19,000 policies in force, up 15% from a low period three years earlier but down 41% from August 2015, according to association data.

Over about the same period, the number of policies in Florida shot up 169% to more than 1.3 million, state data show.

Alabama also created a grant program, with awards of up to $10,000, for owners of existing homes to upgrade roofs, windows and doors to Fortified standards. Funding comes from fees paid by the insurance industry, not from the state’s general fund.

When new rounds of grants become available each quarter, the state’s website for applicants gets deluged, said Brian Powell, deputy commissioner at the Alabama Department of Insurance. Available awards usually get snapped up within 15 minutes, he said.

Mike Henriksen, a builder, recently visited a Fortified Gold home in Fairhope, part of Baldwin County, that he had just completed and highlighted some of the features that protect the building against hurricanes.

The roof deck was sealed with a water-resistant membrane, then covered with metal roof panels fastened with stainless steel screws every 4 inches. Metal straps secure the entire structure, from floors to walls to the roof.

White-oak doors and windows are designed to withstand 160-mile-an-hour winds.

“I wouldn’t hesitate to be in this house during a bad storm,” Henriksen said.

Other states such as North Carolina are pursuing similar programs. Louisiana lawmakers this year appropriated $30 million for a roof grant program modeled on Alabama’s, said Jim Donelon, Louisiana’s insurance commissioner.

Another measure requires insurers to file proposed discounts for homeowners who get Fortified roofs, he said.

In 2020, Hurricane Sally put Alabama’s Fortified constructions to the test when it made landfall in Baldwin County as a Category 2 storm, with 105-mile-an-hour winds.

Warren Hopper rode out the storm at his home in a subdivision with 84 Fortified Gold houses. The structures suffered minimal damage and none had water intrusion, he said.

Meanwhile, a nearby neighborhood with non-Fortified homes fared far worse, he said. Roughly three-quarters of the houses sustained roof damage and wound up covered in the familiar post-hurricane blue tarps.

“They saw the brunt of what happens without Fortified,” said Hopper, 56, who recently had a plaque made for his neighborhood’s entrance that nods to Saddlewood being a “Fortified Community.”

Studies of insurance-claims data from several hurricanes in recent years have shown that homes with Fortified designations had fewer claims—and less loss per building—than non-Fortified ones.

Separately, one study found home buyers were willing to pay more for Fortified houses.

Alabama officials began considering the Fortified program after hurricanes including Ivan and Katrina struck the Gulf Coast in 2004 and 2005. The resulting losses and insurance-market turmoil prompted state lawmakers and others to explore potential mitigation programs to protect homes.

Developers such as Truland Homes and D.R. Horton have adopted the Fortified program and made it part of their sales pitch to customers.

“Basically, if you build in coastal Alabama, you have to be Fortified,” said Ben Murphy, owner of a building and roofing company in Foley, Ala., near the Gulf.

Home buyers have gone from knowing little about the program to actively seeking homes with that designation, said Kendall Wahlert, a real-estate agent in Fairhope. Buyers like the insurance discount and the sense of security in the event of a storm, she said.

Andretta Montgomery landed a $10,000 grant last year to redo the roof of the home in Daphne, part of Baldwin County, that she had bought the previous year.

As a result of the upgrade, she was able to change insurers and snap up a plan with higher dwelling coverage, a lower hurricane deductible and a premium that is about $500 cheaper a year.

“It is nothing short of a gift,” said Montgomery, 58.

Updated: 2-14-2024

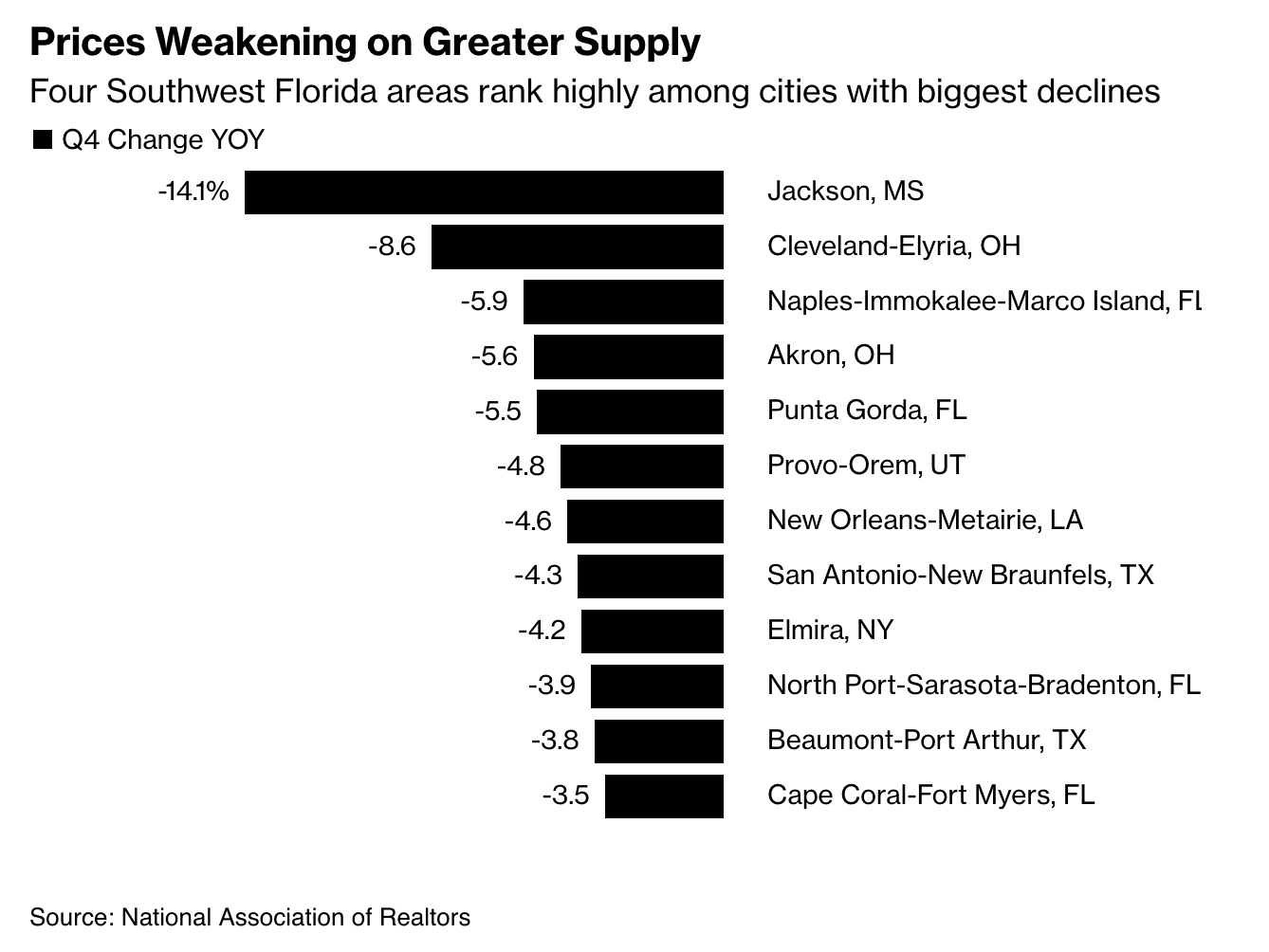

In Southwest Florida, High Home Insurance Rates Are Driving Away Would-Be Buyers

* Cape Coral, Sarasota, Naples See Prices Fall On Higher Supply

* Hurricane Ian Worsened Already Rising Homeowners Rates

Florida’s southwestern coast — long one of America’s fastest-growing regions — is losing some of its boomtown swagger as a home-insurance crisis and other soaring costs make homes unaffordable.

Homeowners from Sarasota south to Naples, known for its eight-figure waterfront mansions, are having a tougher time selling their properties, and the buildup in inventory has caused home prices to fall at some of the fastest rates in the nation.

Realtors point to rising insurance costs that were exacerbated by Hurricane Ian in 2022, prompting some homeowners to list their homes for sale and would-be buyers to walk.

“You’ve got people that went through the storm and just want to move on, and don’t really think the affordability is here anymore because of insurance,” said Marlissa Gervasoni, president of the Royal Palm Coast Realtor Association.

“From what I’m seeing, I believe they are looking for areas that might be less costly.”

Southwest Florida has been one of America’s fastest-growing regions for decades, historically luring retirees from the Midwest drawn to its warm winters, prevalence of golf courses and relatively affordable housing.

In recent years, agents have said they’re seeing more newcomers from the Northeast and other regions, and the area’s rise in home prices has outpaced the nation overall.

However, several factors are converging and hitting the region’s normally hot real estate industry all at once, said Amir Neto, director of the Regional Economic Research Institute at Florida Gulf Coast University.

Developers are bringing a wave of multifamily residential projects online just as a pandemic-fueled surge of migration slows and high mortgage rates weigh on housing demand, Neto said.

Add to the mix an insurance crisis, and a seller’s market is becoming a buyer’s one, he said.

Homeowners policies across Florida started soaring in 2020 because of what insurers and state regulators attributed to rampant lawsuits and fraud.

Rates in the state climbed as much as 33% annually, then shot up another 42% last year in the aftermath of Hurricane Ian, according to the industry-funded Insurance Information Institute.

Ian, a Category 5 storm that was the third-costliest in US history, led some insurers to pull out of the state or limit new policies.

Floridians paid $6,000 on average for insurance last year, about triple what they paid in 2019. By comparison, the average US homeowner paid about $1,700 in 2023, the III said.

In Fort Myers, where hundreds of homes and business were destroyed by Ian, “we’re seeing anywhere from a 50-to-100% increase in spending depending on the age of the home,” said Gervasoni, head of that area’s Realtors board.

Florida legislators have passed laws recently to bring insurers back into the state and lower rates, but they remain high.

Today, Cindy Blackburn and her husband feel stuck in what was once their Cape Coral dream home, unable to sell and move closer to family up north.

Hurricane Ian blew ashore not far away on a barrier island called Cayo Costa, damaging the Blackburns’ roof and everything underneath.

For a time, they lived in an RV while contractors rebuilt their house, all the while battling with an insurance company that put up obstacles to getting reimbursed, Blackburn said. Ultimately, they self-funded most of the $250,000 in repairs.

By last summer, the Blackburns were ready to sell their home and move to Tennessee or North Carolina. They listed it in August, but it languished until last month and they took it off the market.

Their broker at the time never disclosed they couldn’t sell the property while they still had an insurance claim pending, Blackburn said. They’ve since found a new agent, Gervasoni, and are hoping a lawyer can resolve their insurance claim.

“This was to be our retirement house, and having gone through what we’ve gone through, we’ve realized this is not where we belong,” said Blackburn, 59.

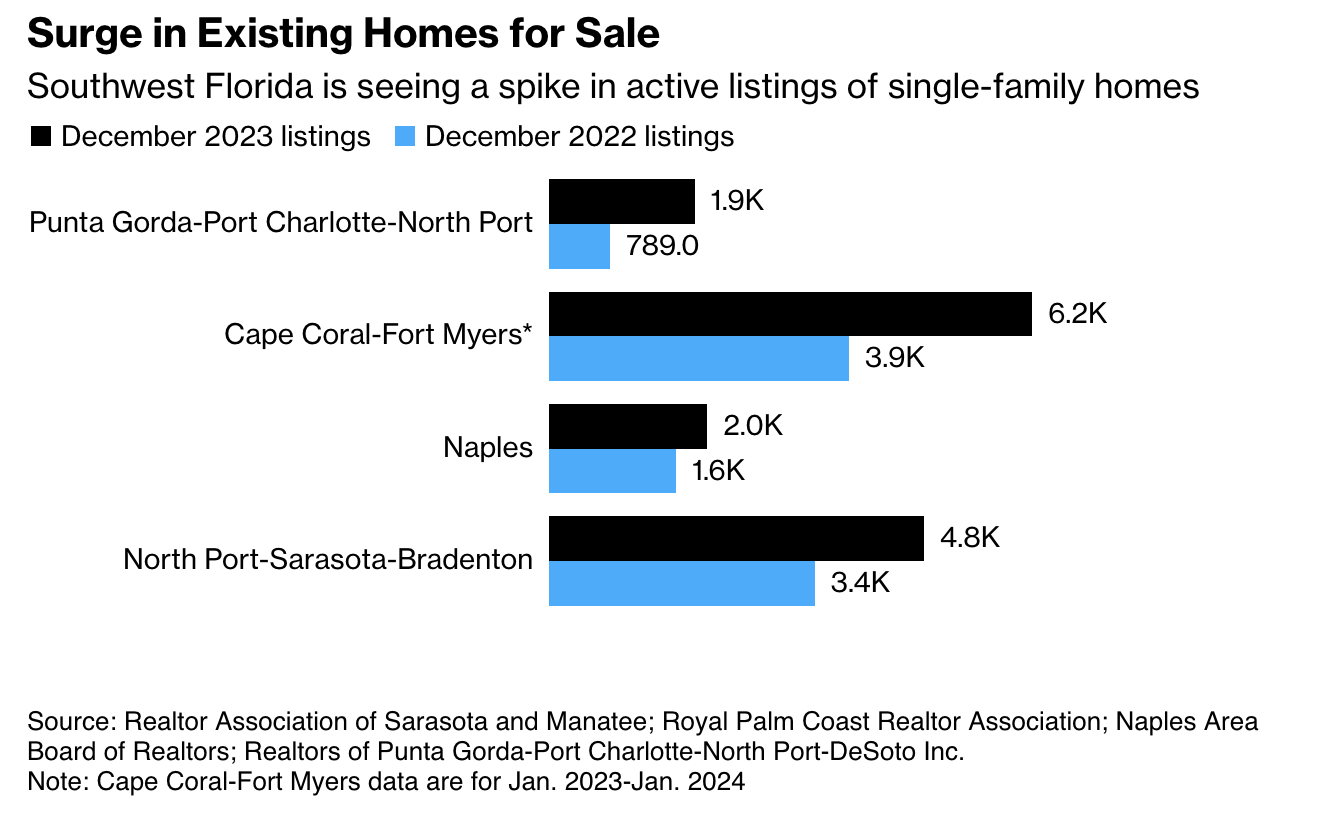

Likewise, homes for sale are piling up in some cities.

Active listings of single-family homes in the Cape Coral-Fort Myers area were up 62% last month compared with a year earlier, while those in Punta Gorda — which is 100 miles south of Tampa — were up 139% in December from a year ago, according to local Realtors boards. Supply is up in Naples, too, but not by as much.

Some of the spike is a fluke. After Hurricane Ian ravaged the region in September 2022, thousands of people, like the Blackburns, suffered damage to their homes and filed insurance claims. Now that most of those claims have been resolved, people can put their homes up for sale.

Prices have taken a hit. Of the 12 metropolitan areas with the sharpest drops in median sales prices in the past year, four are in Southwest Florida, according to the National Association of Realtors.

Prices in the Naples-Immokalee-Marco Island area fell 5.9% in the fourth quarter of 2023 from a year earlier, the third-steepest drop in the group, NAR data show.

“It needed to happen, or else we were going to price everyone out of the market,” said Tony Barrett, president of the Realtor Association of Sarasota and Manatee. He calls the slowdown a “reset” rather than a down market.

The rise in listings — which is also happening in the broader state of Florida, but to a lesser degree — stands in contrast to the national trend, as high mortgage rates have discouraged homeowners from moving.

To be sure, some of the state’s increase in supply represents a normalization from extremely low levels, but it’s also due to higher insurance costs and the rise in home prices in recent years, said Brad O’Connor, chief economist at the statewide Florida Realtors.

“Affordability has eroded in a big way,” O’Connor said.

Updated: 3-25-2024

A Hidden Crisis In US Housing

In places most prone to wildfires and hurricanes, state “insurers of last resort” are absorbing trillions of dollars in risk.

It is so easy to start a wildfire. A smoldering campfire, a lightning strike, an errant firework or a spark from a power line or a hot muffler: However California’s next monumental blaze begins, the toll will be vast.

People will be injured, some will die. Thousands of homes will be destroyed.

When the smoke clears, the most populous US state, home to Hollywood, Silicon Valley and a real estate market worth more than $9 trillion, will be ground zero for a sweeping financial crisis.

Some 11 million people live in California’s high-risk wildfire zones, areas that include Los Angeles county, San Diego and the vineyards of Napa and Sonoma.

Not long ago, they and homeowners in natural disaster regions around the US would have almost certainly had insurance through a big, national company like State Farm General Insurance Co., Allstate Corp. or Hartford Financial Services Group Inc.

But a growing number of insurers are cutting their business in those areas, deterred by more intense and frequent natural disasters, plus state-imposed limits on how much they can charge.

Homeowners in the most risky places are now more likely to be covered by state-created, “last resort” insurance programs that provide protection where the private market won’t.

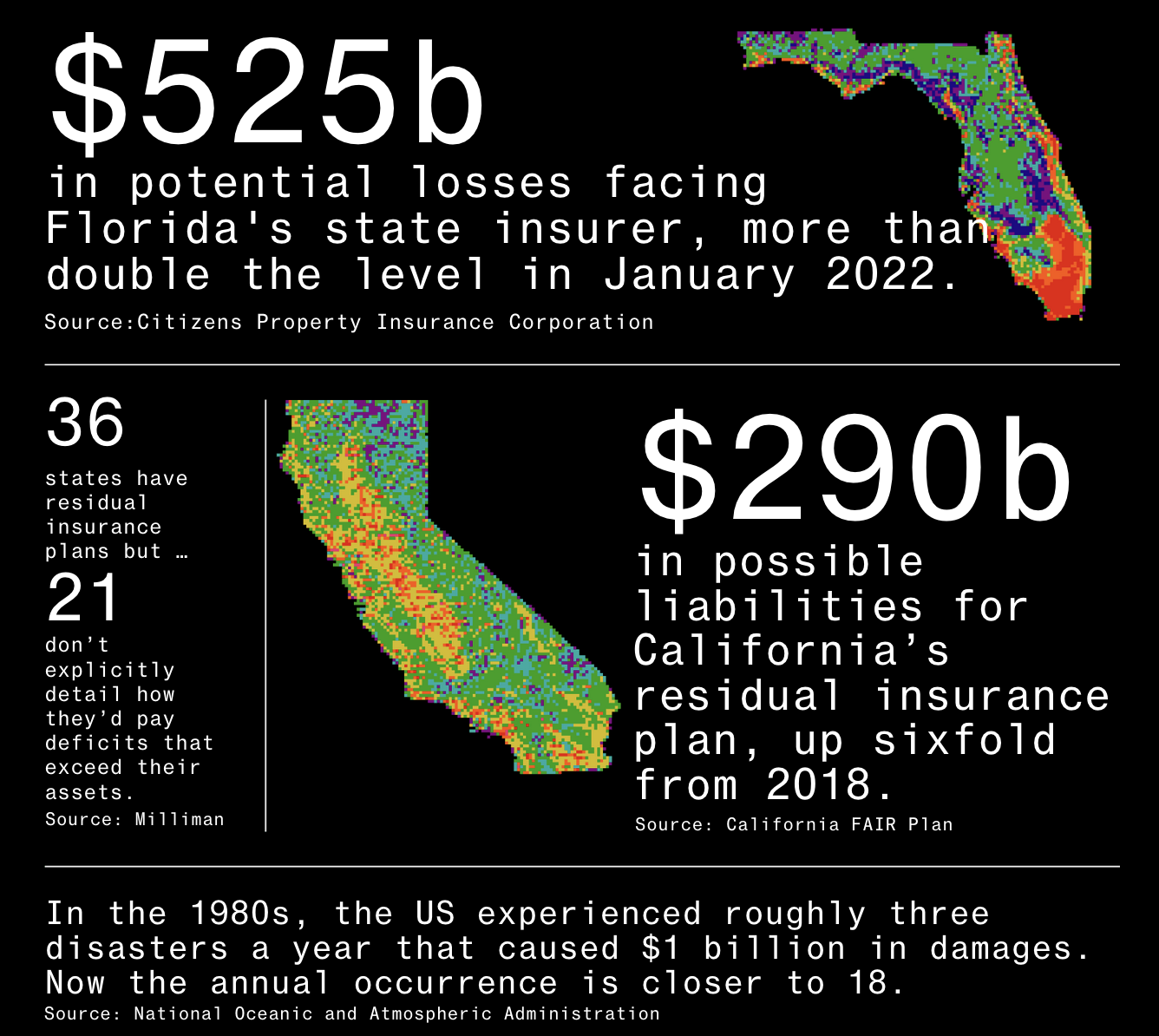

Those plans have more than doubled their market share since 2018, and their liabilities crossed the $1 trillion threshold for the first time in 2022, according to Property Insurance Plans Service Office Inc., a research firm that tracks the programs.

The most climate-vulnerable states are the most exposed: As of now, Florida’s plan could suffer $525 billion in losses; In California, it’s at least $290 billion, up sixfold from 2018.

But even as states have assumed more and more risk, they’ve largely dodged a fundamental question: How will they cover claims in the wake of a truly major catastrophe? There are limited options—levies on private insurers or state residents, or more state borrowing—and none of them are good.

Most states haven’t thought this far ahead, or if they have, they’re not explicit about where the money will come from. Out of 36 residual insurance plans that offer coverage for natural catastrophes, 21 don’t explicitly detail how they’d pay deficits, according to new research from consulting group Milliman.

States have turned these plans into “a magic hiding place to disappear risk that just gets too big for the private market,” said Nancy Watkins, a principal and consulting actuary based in Milliman’s San Francisco office.

Federal lawmakers have begun to take notice of the conjoined problems of rising risks and higher costs. US Senator Sheldon Whitehouse, a Democrat from Rhode Island, is investigating the possibility that a big-enough disaster on Florida’s coast might trigger a national real estate crisis, or push the state’s residual insurer to seek a federal bailout.

Meanwhile, Representative Adam Schiff, a Democrat from California, has proposed a national catastrophic reinsurance program, similar to the longstanding—and chronically indebted—National Flood Insurance Program.

California is one of those states that doesn’t explicitly spell out what it will do if claims force it into deficit. The state department of insurance says that current rates are adequate to cover losses, and that there are safeguards in place to make policyholders whole.

But the Personal Insurance Federation of California, an industry trade group, disagrees.

It points out that the state can’t know whether rates would cover losses because the plan hasn’t performed the kinds of stress tests designed to understand the consequences of another bad fire season.

California’s plan has no more than a general idea of what it could owe, how much it could fall short, or what kind of burden might fall to the private insurers—companies that have already declined to cover the riskiest parts of the state.

In a statement, the California Department of Insurance said it performs a triennial examination of the residual insurer to “evaluate the financial condition, assess corporate governance, identify current and prospective risks, and evaluate system controls and procedures used to mitigate those risks.”

The plan isn’t subject to the kinds of capital requirements designed to prevent private insurers from taking on too much risk, according to the statement. A spokesperson for the plan said that “information regarding [its] financial situation isn’t publicly disclosed.”

It’s hard to overstate the role that insurance plays in the modern American economy. Banks won’t make mortgage loans for uninsurable properties; without those loans, the real estate market slows to a crawl, which in turn eats away household wealth and the tax revenue that state and local governments rely on.

For insurers to play their part, they have to feel confident predicting how much damage they might have to cover. To do that, they build models of the future based on what’s happened in the past.

They don’t have to be right all the time, just enough to win more than they lose.

Climate change has made that much harder. A warming world is more dangerous and unpredictable. In the 1980s, the US experienced roughly three disasters a year that did at least $1 billion in damage.

Now the annual occurrence is closer to 18, according to the National Oceanic and Atmospheric Administration, and likely to rise.

Private insurance companies are required by law to balance those risks with assets, typically a mix of plain vanilla investments, and hedges that include more complicated products like catastrophe bonds or reinsurance.

They feed that stockpile with revenue from premiums. As the risks rise, so do the prices, sometimes to levels beyond what state regulators or policyholders will accept.

When market conditions become too hostile, private insurers limit their exposure in a different way: They stop writing new policies.

When property owners see premiums skyrocketing or private insurers leaving, it’s one signal that the risks of disaster have grown beyond what the market will bear. Maybe it’s no longer safe to live—or at least, to invest significant wealth—in such places. Maybe it’s time to move.

That’s not a popular message for homeowners or their elected representatives, a group that includes, in 11 states, the insurance commissioner.

Given the central role that insurance plays in the real estate market and, therefore, state revenue and population growth, politicians are tremendously motivated to keep insurance prices low, muting that market signal.

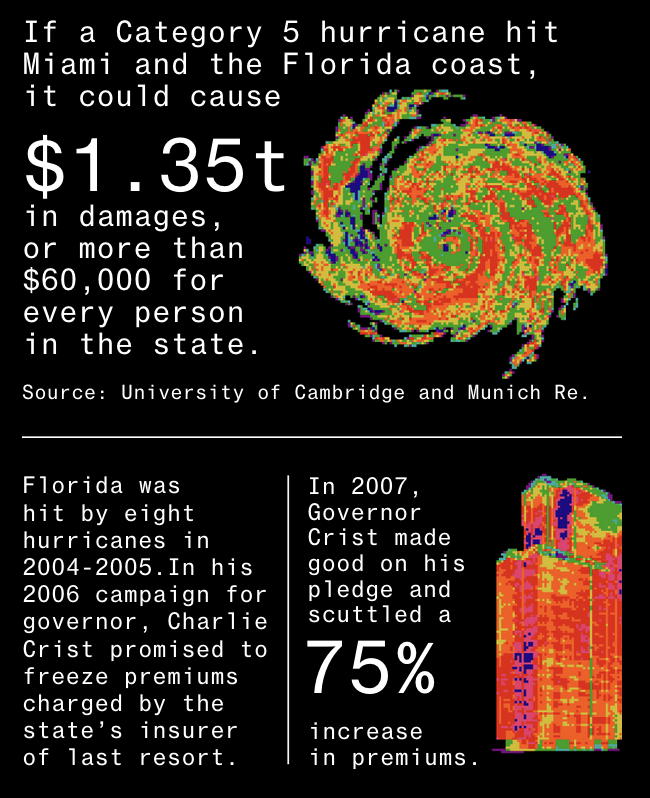

Florida, for example, was hit by eight hurricanes in 2004 and 2005. In his campaign for governor the next year, then-Republican Charlie Crist promised to freeze premiums charged by Citizens Property Insurance Corp., the state’s insurer of last resort.

When he took office in 2007, he scuttled a 75% planned increase.

He set an important precedent. Florida, which has some of the riskiest assets in the US, has kept Citizens’ premiums at far less than the private market for storm insurance. Its policy count has almost tripled since 2018.

If Citizens faces a shortfall, it will allow insurance companies to levy a fee on every policy in the state. That means anyone with property insurance would be on the hook.

Historically, those assessments have been small, but that’s no guarantee. According to a 2018 study by the University of Cambridge and Munich Re, if a Category 5 hurricane hit Miami and the Florida coast, it could cause a staggering $1.35 trillion in damages, more than $60,000 for every person in the state.

Even a much smaller amount could stretch the means of the state’s significant retiree population, said Whitehouse, who leads the Senate Budget Committee. In November, he launched a probe into Citizens, asking for information about how it manages climate-related losses.

“The problem is that the numbers spin out of control once you look at them,” he said in an interview. “We’re afraid that’s a sign, that they know perfectly well that their numbers don’t add up and that they’re in deep, deep trouble. They just don’t want to admit it.”

Michael Peltier, a spokesperson for Citizens, referred Bloomberg Green to a letter the organization sent to Whitehouse in December, which says that it buys reinsurance and has ample reserves and financing options.

It also noted that it can levy assessments on policyholders across the state and said its structure ensures it will always be able to pay its claims.

Whitehouse, though, is concerned that Citizens might need to appeal to the federal government for help, with Lehman Brothers-style arguments both for and against. “If Florida is the leading edge of the predicted coastal property values crash, it could lead to an economic meltdown similar to 2008,” he said.

California’s insurance crisis dates to Proposition 103, a 1988 ballot initiative that rolled back existing rates, then among America’s highest, and subjected future increases to state approval.

Its supporters like to point out that Californians have saved $150 billion in premiums over the last 25 years. The insurance industry says those price caps have undermined its ability to do business in the state.

Thirty years later, a spark from a faulty electric transmission line started a fire that quickly spread over tinder parched by years of drought.

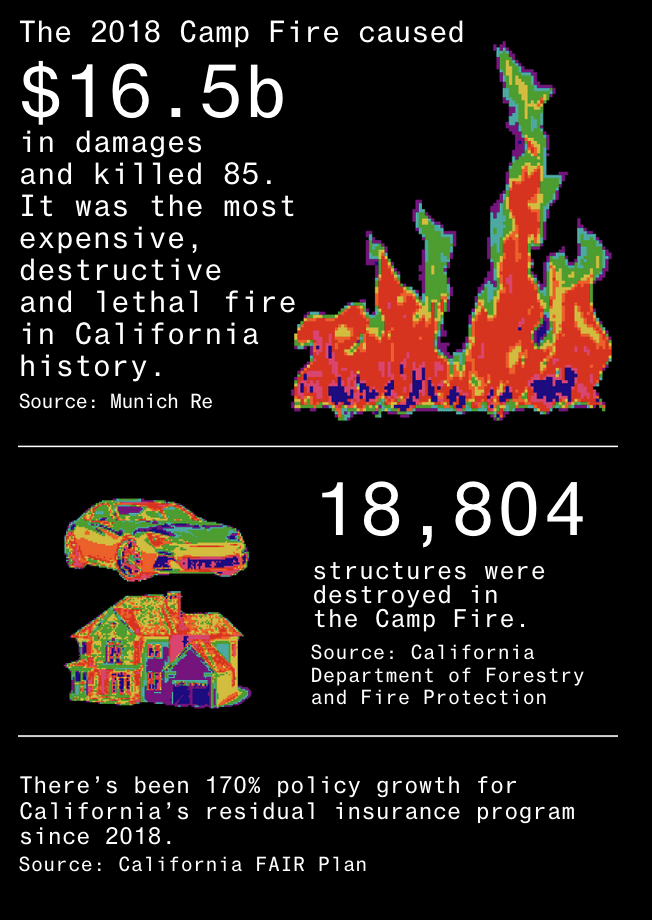

What became known as the Camp Fire burned for more than two weeks in 2018, demolished almost 19,000 buildings, caused $16.5 billion in damage, killed at least 85 people, and left dozens more missing—making it the most expensive, catastrophic and lethal fire in the state’s history.

For private insurers, the losses were stunning. Fire damage from 2017 and 2018 wiped out more than twice the previous 25 years’s worth of underwriting profits for the California insurance market, according to Milliman.

The industry recouped some money from the utility that owned the transmission lines and premium increases as much as the state allowed, but it was still an ominous sign. The five biggest blazes of the 2020 season destroyed another 7,800 structures across almost two million acres.

Combined with state restrictions on how insurers are allowed to account for climate change, a growing number of big insurers have decided that California’s no longer viable.

State Farm, USAA, Allstate, and the Hartford have either stopped writing new homeowners policies or limited coverage across the state. In 2021, roughly 13% of total voluntary home and fire insurance policies weren’t renewed.

State Farm and USAA didn’t respond to messages seeking comment. A spokesperson for Allstate said the company is working with California’s insurance commission to help improve coverage availability, and offer more policies using wildfire modeling and reinsurance.

A spokesperson for Hartford Financial said the insurer stopped offering new homeowners policies in February. “We need to be able to price our homeowners’ insurance appropriately for the risks we are protecting against,” she said.

California’s newly uninsurable homeowners have turned to the state’s residual insurance plan. Since 2018, the number of policies has grown 170%.

Now it typically receives 1,000 new applications a day. Though the plan doesn’t make its finances public, a state report estimates it’s holding roughly $100 million in reserves as of 2021—less than 1% of the insured losses from Camp Fire.

To cover any shortfall, the state plan will assess private insurers proportionally to their market share. As far as the state’s concerned, the insurers are on the hook for the most fire-prone properties, even if they’ve already decided the numbers don’t add up.

If a catastrophic event triggers a massive assessment, it could force some insurers into bankruptcy, said Rex Frazier, head of PIFC. “Or would the state step in and say, ‘no, we’ll allow them to put a surcharge on all of their policyholders.’ Who knows? We don’t have the answer.”

For companies that live and die by their ability to forecast and manage risk, that kind of uncertainty poses a real problem. Ultimately, a critical mass of insurers could exit California.

Or they could start to exclude wildfire coverage. In that case, the state could have to step in with its own plan at a cost borne by everyone in the state.

“It would be like Obamacare for property insurance,” said Jeff Engelstad, a professor of real estate and construction management at the University of Denver. “That would be a shame, because it’s not the most efficient model. But a market solution would be too severe.”

Ricardo Lara, California’s insurance commissioner, is advocating for what he calls “the largest insurance reform” in the state since Proposition 103.

His plan would enable insurers to raise rates more quickly and to allow for increases based on forward-looking climate change data and reinsurance costs, changes he says will stabilize the market.

Homeowners don’t understand disaster risk the same way that actuaries do. Moving is a headache under the best of circumstances; for individuals or families, it can seem like a crazy response to a theoretical future disaster.

And while humans expect risks in general, we tend to discount the likelihood that any particular bad event will happen to us.

Thad Eggen co-owns an 18-room lodge and steakhouse near Colorado’s Rocky Mountain National Park, about 66 miles (106km) northwest of Denver. During 2020’s East Troublesome wildfire, guests could see thick plumes of smoke billowing up over nearby mountains from the lodge dining room.

Snow and firefighters stopped the flames before they reached Eggen, but it left him with fear. “We’re sitting in a tinderbox,” he said “I constantly worry that this park could go up in flames.”

Insurance companies were prone to agree. Damage from wildfires and hailstorms made Colorado one of the least profitable states for home insurers in the five years through 2021.

As a result, premiums in the state jumped more than 50% between 2019 and October 2022. Even so, three-quarters of home insurers reduced their exposure to the state in the first 10 months of 2022.

Last year, Eggen discovered his premium would surge from $40,000 to $400,000. His insurance broker told him it wasn’t a typo. “It was bizarre, I was in denial,” Eggen said. “I thought I may as well hand the keys to my business to the bank.”

What he didn’t consider, though, was moving. Other places have their share of natural disasters, he figured. Eventually, he found another insurance company willing to cover him for a relative bargain of $70,000. “I am just taking it year by year.”

Last spring, Colorado passed a law to create a new insurance plan, the first state to do so in decades. They had no other choice, said state Representative Judy Amabile, a Democrat who co-sponsored the legislation.

Without affordable insurance, she said, “there’ll be no real estate transactions, no businesses, hotels, stores. Insurance is pretty fundamental to keep things going.”

As in other states, Colorado will require private insurers to participate in order to do other business in the state. It’s supposed to be financially sound and providing coverage only to those turned down by the private insurers at premiums that reflect risk.

Details about how the plan will manage the risk or what it will charge haven’t yet been made public. It’s scheduled to start writing policies in 2025.

One way or another, it may come back to taxpayers, said Colorado Insurance Commissioner Michael Conway. “If climate change is beginning to increase claims and payments, which ultimately it is, it’s fundamentally the consumer and society in general that bears the brunt of that,” he said.

When insurers and consumer advocates talk about how to address the growing risks presented by climate change, they often mention the importance of “hardening,” the industry term for how individual homeowners can limit damage.

In a fire zone, that includes using “ignition resistant” building materials and creating a buffer zone with no vegetation; in flood-prone areas, it could include battery-operated sump pumps, or elevating houses with stilts.

There are essentially two tools to encourage homeowners to make these kinds of changes, often at considerable cost. Insurers can offer discounts, and the state and local governments can update the building codes.

The latter is immediately effective for new construction. Older homes typically don’t have to conform until their owner wants to renovate or sell.

Even then, there are limits. Improvements in Florida’s building codes mitigated exposure by more than 90% compared with the 1970s, according to recent analysis by Swiss Re.

But at the same time, strong hurricanes have become more frequent, and with the state-sponsored insurance program backstopping real estate transactions in the riskiest areas, more people have moved in.

This “population-amplifying loss potential,” as the study calls it, rose to more than 180%.

In the effort to shield residents from short-term price hikes, residual insurers effectively subsidize the owners of vast swaths of real estate, said Robert Hartwig, a director at the Risk and Uncertainty Management Center at the University of South Carolina.

“We’ve been incentivizing people to locate properties in hazard-prone areas for many decades,” he said. “It’s a legacy that we’re going to have to deal with.”

California State Senator Brian Dahle, a Republican whose district was ravaged by the Camp Fire, says catastrophes cast a long shadow. Many communities have yet to fully recover from their financial and personal losses.

Not everyone has chosen to stay—the population of Butte County has declined 10% since 2018, compared with a 1% drop for the state as a whole during the same period.

Those who remain call Dahle’s office to say they can’t find insurance or are paying premiums higher than their mortgages, even after “fire-proofing” their properties. He’s a strong advocate of home hardening and has backed several bills designed to decrease the risks to his constituents and provide some measures of relief.

Ultimately, though, he says, this is the insurance commissioner’s problem to fix.

“I don’t know what the future holds,” he said. “I know one thing: There’s some things we can do and some things we just have to just pray about and wait and see what happens.”

Updated: 4-1-2024

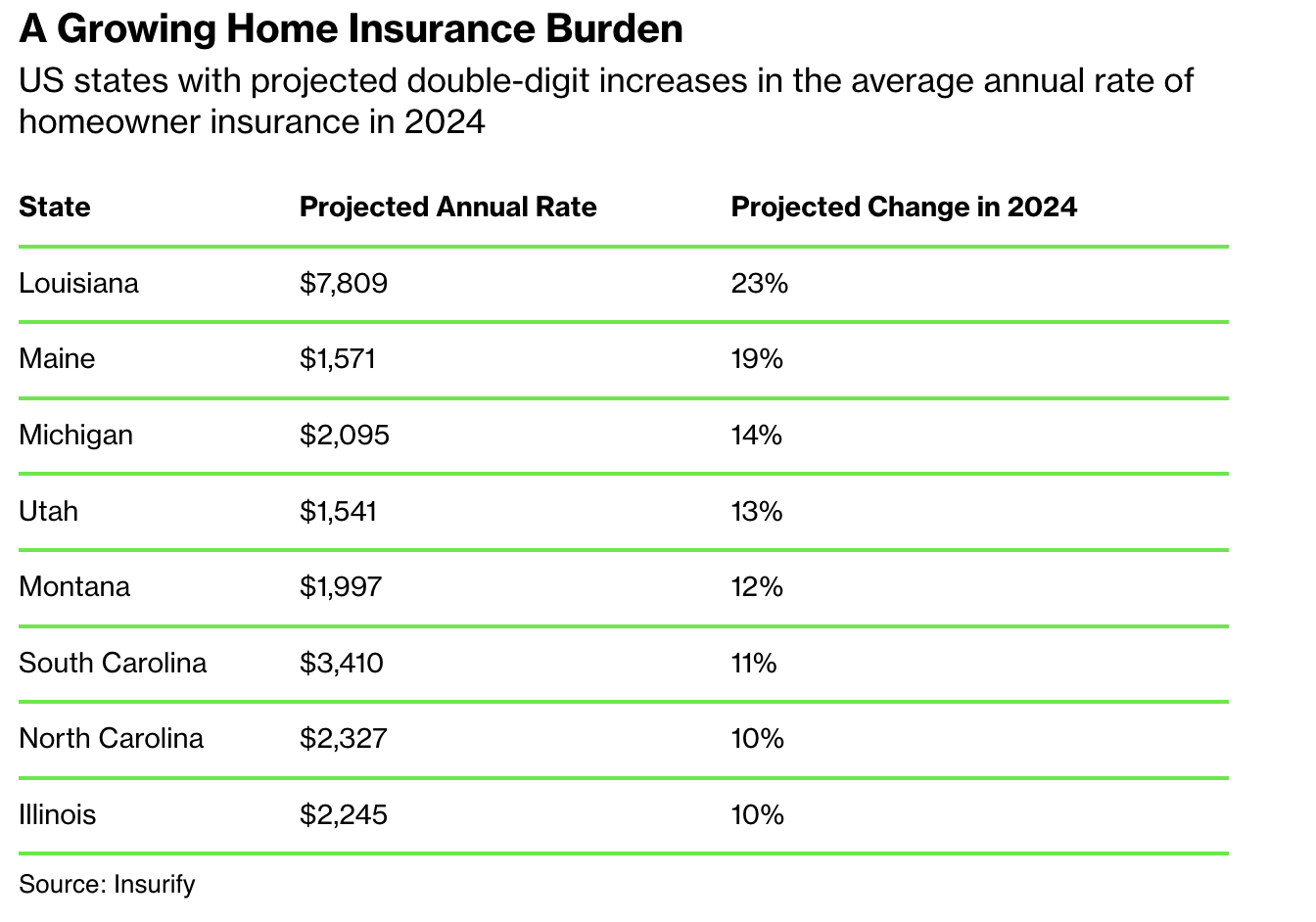

US Home Insurance Premiums May Hit A Record This Year, Report Warns

The average premium for US homeowners insurance is expected to hit $2,522 this year, up 6% from the end of 2023. Premiums in Florida will approach $12,000.

US home insurance rates are expected to reach a record high this year, with the biggest increases occurring in states prone to severe weather events, according to a new analysis.

The average premium for homeowners insurance in the US is expected to hit $2,522 by the end of the year, driven largely by intensifying natural disasters, rising reinsurance costs and higher fees for home repair, according to Insurify, a Massachusetts-based insurance-comparison platform.

That figure would represent a 6% increase over the average US premium at the end of 2023, and follows a roughly 20% increase over the past two years.

“Many Americans are motivated to buy a home because they think their housing costs will remain fixed or stable when compared to renting,” says Cassie Sheets at Insurify, who co-authored the analysis.

“But this trend of significant insurance rate hikes makes housing costs more unpredictable.”

Home insurance is becoming a flashpoint in the US as damage from thunderstorms picks up and as climate change increases the frequency and severity of natural disasters. In the 1980s, the country experienced about three disasters a year that caused damages of at least $1 billion each.

In the 2010s, that climbed to 13 per year, according to the National Oceanic and Atmospheric Administration. Last year, the US endured a record 28 weather and climate disasters that caused at least $1 billion in damages each.

Responding to climate-induced threats, a growing number of insurance companies are pulling out of California and Florida, where those impacts are frequently felt. To fill the gap, state “insurers of last resort” are absorbing trillions of dollars in risk.

“It’s possible that the highest-risk areas will become uninsurable,” says Betsy Stella, vice president of carrier management and operations at Insurify.

“However, where there’s demand, typically a supplier will appear. The question will be, at what cost?”

For Insurify’s analysis, researchers collected real-time quotes from the platform and combined them with aggregate rate filings from a third-party data provider.

They then analyzed how often and by how much insurers implemented rate increases during the second half of 2023 and the beginning of 2024 and applied that pattern to the rest of this year.

Insurify only looked at data for single-family frame houses that met a list of criteria around insurance type, coverage limits and homeowners’ credit score and claim history.

The steepest premiums are expected for states that also have the highest risk of natural disasters. Homeowners in Florida, who already pay the highest rates of home insurance in the country, are expected to see another 7% increase this year — bringing the state average to $11,759, more than four times the national average.

Six states, including Texas and Washington, will see their premiums remain almost flat this year, according to the analysis, which cited a healthier insurance market and the stabilizing effect of local legislation.

South Dakota is the only state likely to see a meaningful drop in premiums: Its average is expected to fall about 3% to $2,488.

For states with rising premiums, Insurify’s researchers largely point the finger at the increase in natural catastrophes. According to AccuWeather, the US can expect an “explosive” hurricane season this year, with the potential for as many as 25 named storms between June and November, compared with about 14 on average.

Meanwhile, sea-level rise and other adverse climate impacts are catching up with historically low-risk states like Maine.

The rising cost of reinsurance — through which insurers can hedge their risk by buying protection from other insurers — is also playing a role in higher premiums, as are the growing costs associated with home reconstruction.

Insurance fraud and legal disputes also contribute to higher rates, the analysis notes. That problem is particularly acute in Florida, which accounts for 9% of home insurance claims but 79% of lawsuits over filed claims, according to a 2022 statement from Governor Ron DeSantis.

RBNZ Says Insurance May Become Unaffordable For High-Risk Homes

New Zealanders who own properties in areas prone to flooding or earthquakes may find they can’t afford insurance or may not be offered cover for specific risks, according to the Reserve Bank.

Rising premiums or the inability to insure are a signal to homeowners that they need to reduce exposure to risks, which could include moving away from the area, the RBNZ said in a report Monday in Wellington. The central bank said so-called insurance retreat is also a long-term challenge for the financial system.

“Owners of properties where natural hazard risks have already manifested through claims are unlikely to be able to obtain comparable cover in the future, unless there has been a substantial mitigation of the now known risks,” the central bank said.

“Even if the complete withdrawal of insurance availability in certain areas is some time away, owners of high-risk properties may find insurance increasingly unaffordable.”

New Zealand insurers have moved to risk-based pricing, pushing up costs in earthquake-prone areas such as capital city Wellington.

More frequent climate change-related weather events — including the flooding and landslides caused by Cyclone Gabrielle in early 2023 — are also impacting prices and posing the question of whether some houses should be rebuilt in risky areas.

“It is difficult to pinpoint if and when insurers will completely withdraw the availability of insurance for certain properties, areas or risks, although it could occur relatively quickly given that contracts are typically annual,” the RBNZ said. “Withdrawal would tend to first occur in communities where these physical risks are already well known.”

A potential outcome of risk-based pricing is that insurers begin to unbundle different risks, particularly if one type of peril is a dominant driver of the unaffordability of premiums, it said. For example, unbundling could take the form of removal of flood cover for a flood-prone property in an area with low seismic risk.

The RBNZ said more work is needed to improve collection of natural hazard data, which will help insurers’ risk modeling and improve the price signals.

Banks need to be conscious of the ongoing insurability of the properties they lend against, which will require greater scrutiny in their lending decisions, the RBNZ said.

“Banks also need to pay close attention to insurance coverage given the increasing risks of under-insurance of high-risk properties over time,” it said. “Banks need to work with insurers to obtain better and more regular information on mortgaged properties’ insurance status.”

Updated: 4-9-2024

If US Inflation Reflected Rising Home Insurance Costs, It’d Be Even Higher

Soaring home insurance premiums could have added about 0.8% to last year’s consumer price index increase of 3.4%, according to Bloomberg Intelligence.

If the rising price of homeowners insurance were factored into the US Consumer Price Index — a key metric of inflation — it could have added 80 basis points, or about 0.8%, to last year’s CPI increase of 3.4%, according to an analysis from Bloomberg Intelligence.

By not including home insurance, the CPI “ignores climate costs,” writes BI senior analyst Andrew Stevenson in his April 9 note.

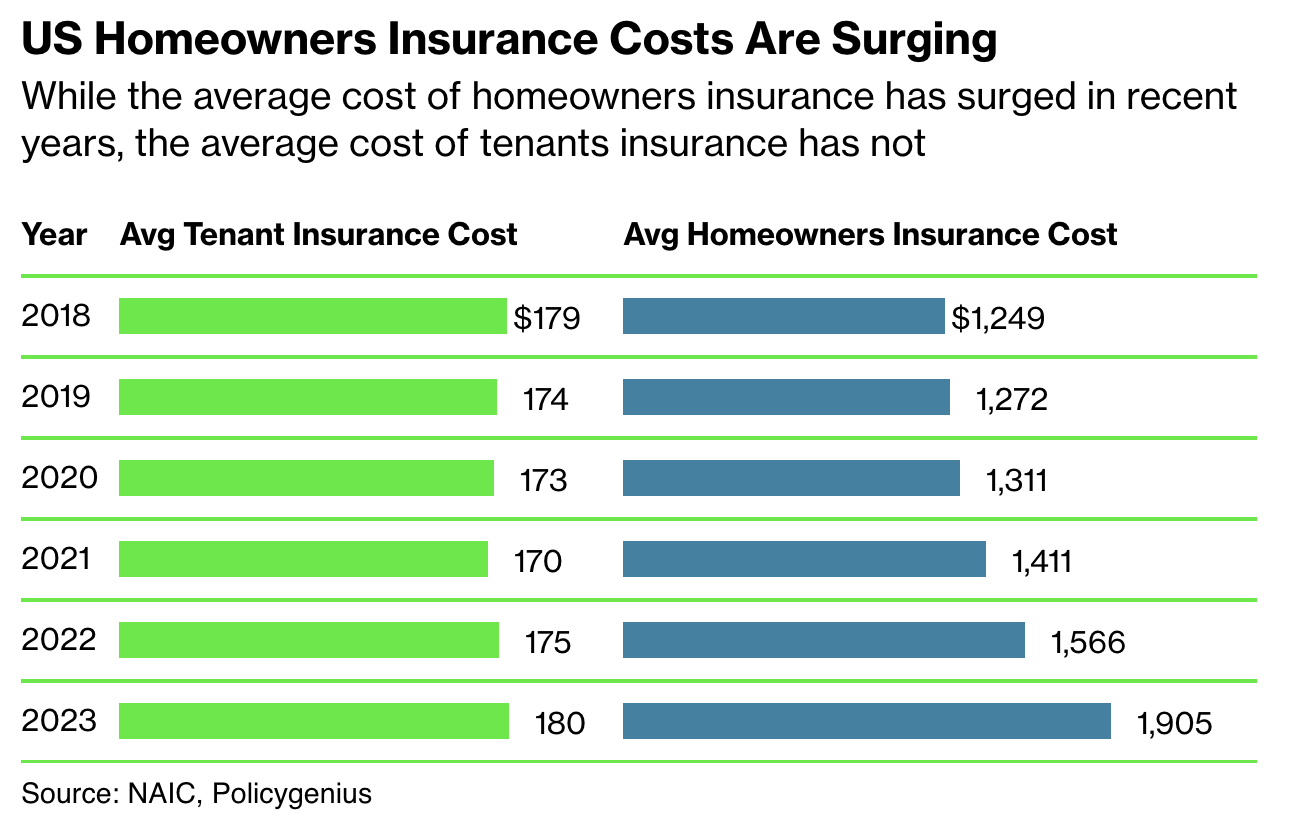

Homeowners insurance costs in the US hit roughly $175 billion in 2023, up 21% over the previous year, according to insurance brokerage Policygenius. The increase is in large part due to climate change, which is driving more extreme fires, floods and storms.

The US endured a record 28 weather and climate disasters that caused at least $1 billion in damage last year.

As insurers incur higher costs, homeowners are facing higher premiums. Inflation itself is also making it more expensive to pay out claims.

The average cost of insuring a US home last year was $1,905 — 50% higher than the average of $1,272 in 2019, according to the National Association of Insurance Commissioners and Policygenius.

Calculated by the US Bureau of Labor Statistics, CPI measures the average change in prices paid by urban consumers for various goods and services, including both food and fuel.

(“Core CPI” excludes food and energy.) CPI includes the category “tenants and household insurance,” but this is more colloquially known as renters insurance. Last year, the average renters insurance cost in the US was $180, up 3% from a year earlier.

Stevenson looked at what would happen if the $1,905 average for home insurance were given the same CPI weight as “tenants and household insurance,” which accounted for just 0.01% of the overall increase in CPI last year.

He found that the 21% increase in home insurance could have contributed as much as “84 bps to the index vs a 1-bp gain realized by the 3% rise in tenant and homeowner insurance costs.” (A basis point is equal to 0.01 percentage point.)

Just five years ago, homeowners insurance and renters insurance were increasing at similar rates year over year. But while home insurance costs have since surged, renters insurance has largely held steady.

The difference “might be meaningful enough” for federal officials to “reconsider” the inclusion of homeowners insurance in the CPI basket, Stevenson writes.

“We are unable to provide any insight into custom calculations created outside BLS,” Gerald Perrins, a BLS section chief working on the CPI, told Bloomberg Green.

The cost of US homeowners insurance stands to keep growing, with average premiums in the US predicted to hit a potential record of $2,552 by the end of 2024, according to Insurify.

Researchers at the Massachusetts-based insurance-comparison platform attribute the expected increase to intensifying weather disasters, rising reinsurance rates and high home repair fees.

Updated: 5-7-2024

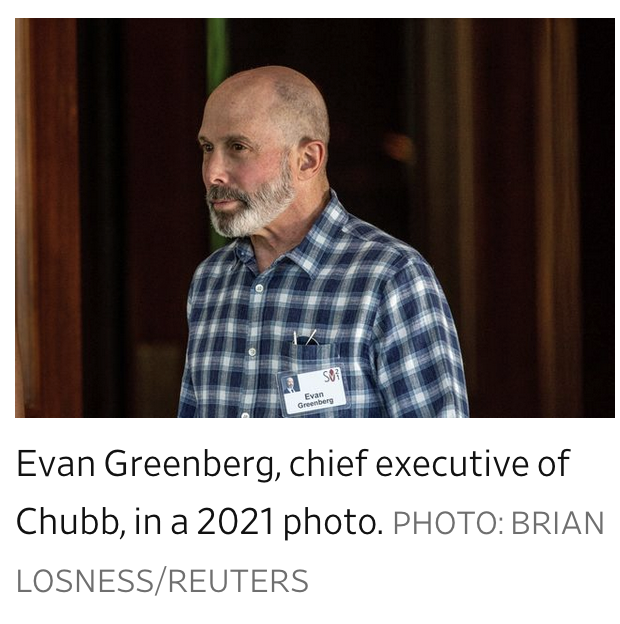

Pricier Insurance Makes Sense As Climate Risk Grows, Chubb CEO Says

Speaking in California, Evan Greenberg says industry has been setting premiums ‘very rationally,’ adding that it didn’t tell people to ‘build magnificent homes in a wildfire zone’.

SAN DIEGO, Calif.—Surging insurance premiums in regions vulnerable to climate change make sense, and government efforts to hold back those increases won’t work in the long term, Chubb Chief Executive Evan Greenberg said.

U.S. states themselves are driving a crisis of insurance availability by blocking insurers from pricing climate change into policies, Greenberg said on Tuesday in San Diego at the RIMS Riskworld conference, an annual gathering of about 10,000 risk and insurance professionals.’

“Climate change is sending price signals. Society will not adjust its behavior to the change of climate just because people talk about it,” Greenberg said. “We’re sending price signals very rationally. That starts driving behaviors.”

Americans and businesses across the country have seen insurance become far more expensive—in some cases nearly impossible to obtain—particularly in areas exposed to wildfire, floods and other damaging weather.

Zurich-based Chubb, one of the most important insurers in the U.S., has been on the front lines of the issue.

California and other jurisdictions are trying to “deny” the ability to charge the “right price” for risk, said Greenberg. Several large carriers have stopped writing new policies in California, with the industry blaming state policies that block insurers from using forward-looking climate-risk models to set prices.

The state is working on changing its regulations. California Insurance Commissioner Ricardo Lara didn’t immediately respond to a request for comment.

Insurers have shelled out billions of dollars in recent years as losses from wildfires and other climate-related events have piled up. The industry isn’t ultimately to blame for affordability problems, Greenberg stated.

“We haven’t told people to live in a high-wildfire zone, and we haven’t told them to build magnificent homes in a wildfire zone,” Greenberg said. “I’m willing to insure them if I can charge the right price for the risk.”

In trying to keep rates down, states are effectively attempting to blunt price signals, Greenberg said. But the net effect is that insurers will stop writing policies—leaving taxpayers on the hook for the risk, he added.

Florida, California and Louisiana have all seen policyholders flock to state-backed insurance plans that are meant to be a last resort.

Many jurisdictions are adopting policies that aren’t sustainable, Greenberg said.

“The cost of climate change, to state the obvious: Going up,” he said. “This is not a short-term thing that’s going to go away.”

Updated: 5-24-2024

The Hidden Driver of Soaring Home Insurance Costs

A looming round of reinsurance renewals could signal slowdown in premium increases.

Joshua Enloe has gone from home-insurance paragon to pariah in just three years. Since 2021, the 36-year-old Texan has been twice dropped by insurers, and his annual rate has almost tripled to $13,000 from $5,000, before ending up with a bare-bones state insurer of last resort.

His offense? Living in El Lago, a coastal suburb of Houston. The 1960s, 2,200-square-foot home Enloe shares with his wife and dogs is in Harris County, hammered by 2017’s Hurricane Harvey. Last week the city’s latest deadly storm swept through El Lago.

One leading, but little-discussed, cause of this coverage crunch: a big increase in the cost of reinsurance policies. Now all eyes are on a round of reinsurance renewals currently under way in Florida and elsewhere that will help determine whether more premium increases are in store for homeowners.

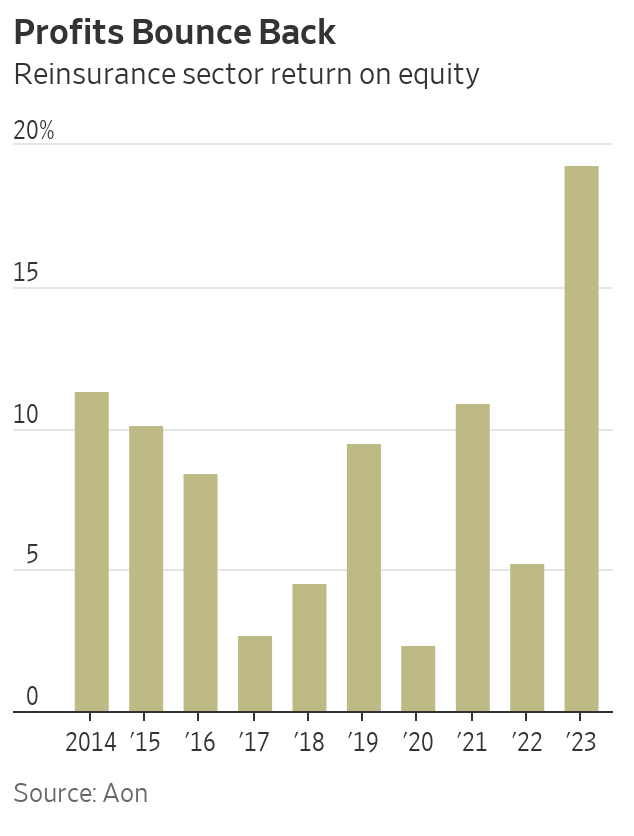

Insurers buy reinsurance policies to limit their risks. After suffering a sharp drop in profits, reinsurers raised rates and cut coverage at the start of last year.

That hit home insurers, making it harder to manage their losses from storms and other extreme-weather events. Many of them passed on the higher costs and reduced coverage to their customers.

“The unregulated, global reinsurance market is a significant driver of the high cost of property coverage across the country, including in Houston,” said Douglas Heller, director of insurance at the Consumer Federation of America.

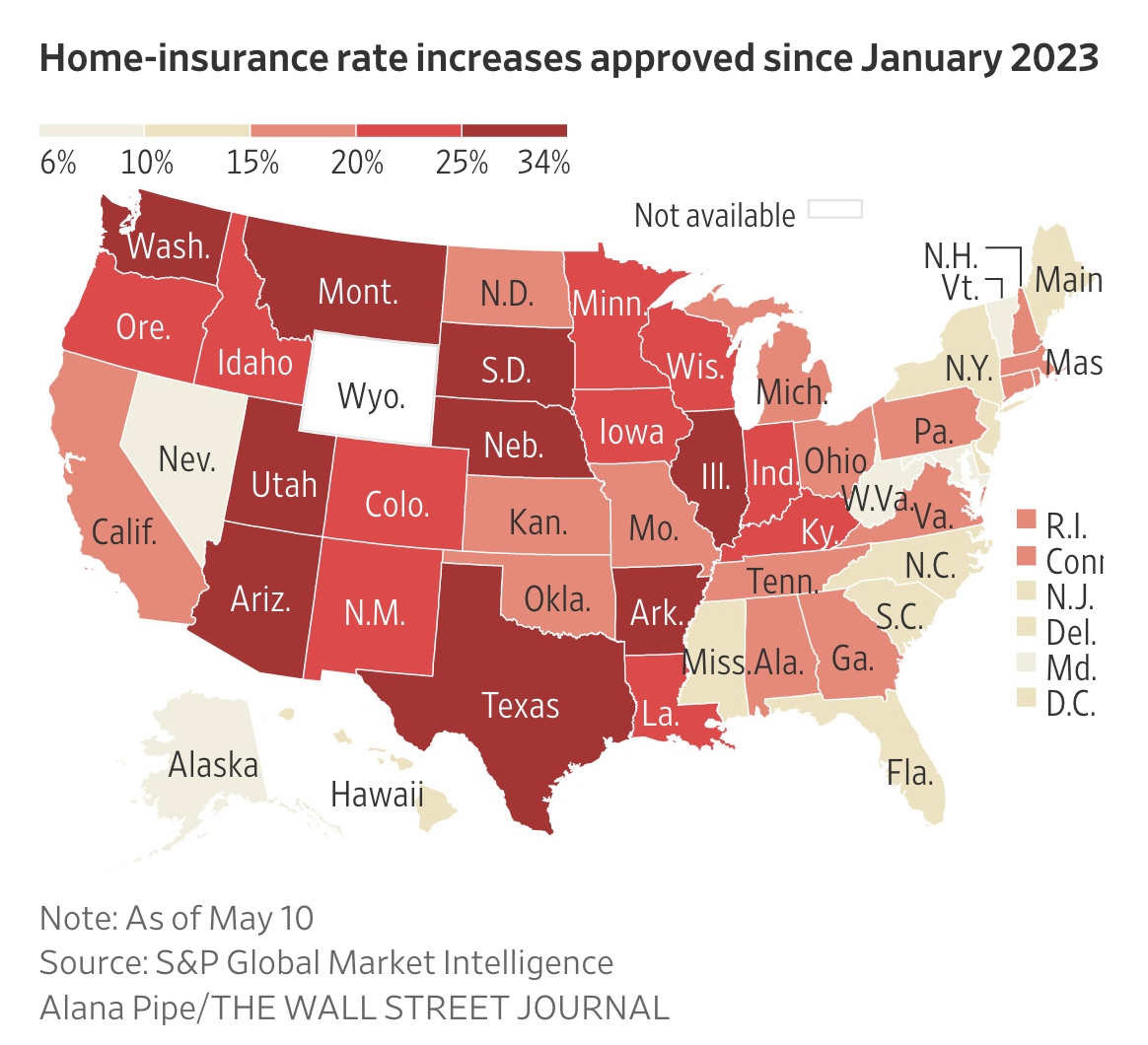

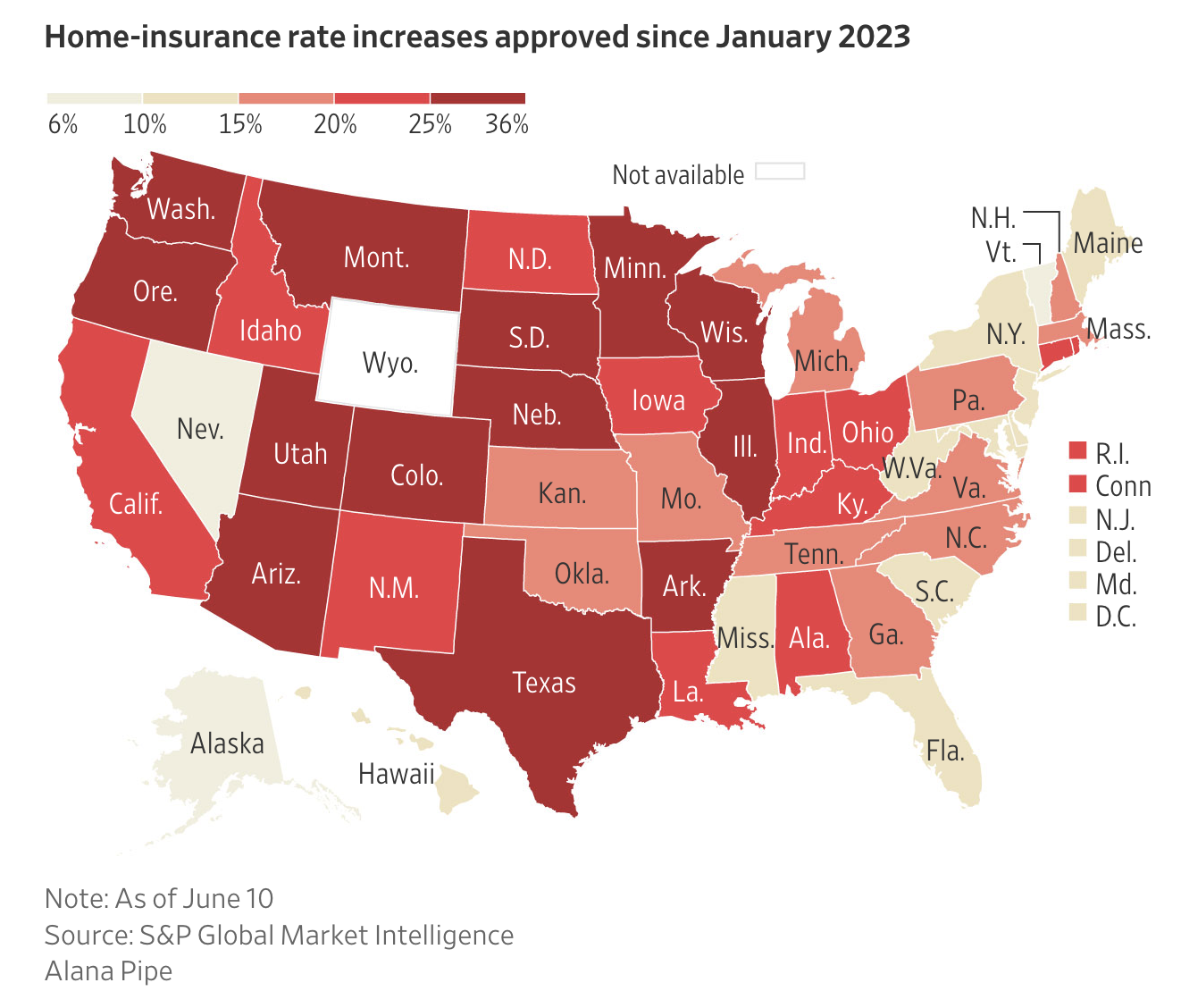

Home insurers are hiking rates and pulling back from disaster-prone areas, such as Houston. Since the start of last year, regulators have greenlighted a 26% home-insurance rate increase in Texas, one of 45 states to suffer a double-digit increase, according to an analysis by S&P Global Market Intelligence for The Wall Street Journal.

Related:

Enloe now has very basic coverage from the state’s FAIR Plan insurer of last resort. The Texas FAIR Plan, which has more than half of its policies in Enloe’s Harris County, reported a 41% increase in its reinsurance premiums last year.

Reinsurance lets insurers sell policies in vulnerable areas without the risk of being wiped out by one big disaster. Those policies have become increasingly expensive. A 63% rate increase last year by Louisiana’s Citizens plan was “almost totally a result of the increased cost of reinsurance,” state insurance regulators said.

David Duffy, head of global clients at the reinsurance broker Guy Carpenter, said: “The whole premise of the reinsurance industry is that you can be a Florida or a Louisiana homeowners insurer and you can spread your very concentrated catastrophe risk…to the global insurance market.”

The cost of this industry safety net increased sharply at the start of last year, after reinsurers suffered a yearslong profits slide. “The companies decided they weren’t getting the returns their investors needed,” said Brian Schneider, a senior director at Fitch Ratings. “We saw 30%, 40%, even 50% rate increases.”

Most states, including Texas, allow insurers to share this pricing pain with their customers. The impact can be particularly marked in disaster-prone states, such as North Carolina. Insurers there say soaring reinsurance costs are a “major driver” of their requests to regulators to raise home-insurance rates by 99% in coastal areas, or 42% on average across the state. The request is due to go to a hearing this fall.

The tough reinsurance market is affecting the availability of home insurance, as well as its cost. The shift goes back to late 2022, when reinsurers significantly hardened their policy terms. The companies raised the level of losses at which they would typically pay out and reduced coverage for rapidly rising losses from perils such as thunderstorms.

“The market restructuring shifted a lot of the risk of relatively frequent catastrophes back to insurers,” said David Flandro, head of strategic advisory at the reinsurance broker Howden Re. “Reinsurers by and large have stood their ground since then,” he added, leaving insurers saddled with greater exposure to storms and wildfires.