How DeFi Goes Mainstream In 2022: Focus On Usability (#GotBitcoin)

2019 was an important year in the slow but steady march towards a future of decentralized finance (DeFi). How DeFi Goes Mainstream In 2022: Focus On Usability (#GotBitcoin?)

What Is DeFi?

DeFi is an abbreviation of the phrase decentralized finance which generally refers to the digital assets and financial smart contracts, protocols, and decentralized applications (DApps) built on Ethereum. In simpler terms, it’s financial software built on the blockchain that can be pieced together like Money Legos. Read more about DeFi.

What’s The Purpose of DeFi Pulse?

DeFi Pulse is a site where you can find the latest analytics and rankings of DeFi protocols. Our rankings track the total value locked into the smart contracts of popular DeFi applications and protocols. Additionally, we curate The DeFi List, a collection of the best resources in DeFi.

How Do We Calculate Total Value Locked(TVL)?

DeFi Pulse monitors each protocol’s underlying smart contracts on the Ethereum blockchain. Every hour, we refresh our charts by pulling the total balance of Ether (ETH) and ERC-20 tokens held by these smart contracts. TVL(USD) is calculated by taking these balances and multiplying them by their price in USD.

How Do I Get Involved In DeFi?

Decentralized finance is open for anyone to take part in. You can start by exploring the resources found on The DeFi List. And if you’re looking to dive head first into the world of DeFi, we’ve written a beginner’s guide called Zero to DeFi. It will teach you the basics, guiding you through how to start earning passive income via DeFi lending services.

Bitcoin once again hit five figures, cementing it position as digital gold (in the words of the Federal Reserve Chairman). The ethereum ecosystem continues to expand. Exciting new DeFi ventures are grabbing headlines every week, from decentralized VPN providers to blockchain infrastructure projects to payment providers.

Equally important, 2019 saw an acceleration of a global attitudinal trend: dissatisfaction with centralized powers. Popular mistrust of banks and financial institutions is deepening. Disinformation on social media platforms is on the rise. Corruption, inequality, and authoritarianism are driving people to the streets, from Hong Kong to Santiago, demanding structural change or new governments. The post-Cold War order has devolved into a tinderbox – which is why all roads lead to a decentralized future where people seize control of their assets, their data, and their financial future.

To be sure, the DeFi movement still has so very far to go. Today’s total crypto market cap of $195B (at the time of this writing) is over $150B shy of the assets managed by the 10th largest U.S. bank. The vast majority of consumers still do not hold cryptocurrencies. They store their money with banks and other centralized financial institutions, and invest only in stocks and bonds.

With 2020 upon us, the crypto community finds itself in an awkward position: we have been so busy building base layer infrastructure and shoring up support among enthusiasts that we practically forgot about the average consumer.

We need to bring DeFi into the fold of mainstream financial services. But, to do so, DeFi projects must build on-ramps – including better user interfaces, accessible products and services, and stablecoins – that make it easier for people who don’t know much about cryptocurrency to buy digital assets easily and participate in decentralized financial services.

A Road Map

First, DeFi needs interfaces that are familiar, intuitive, and enjoyable. DeFi projects can and should maintain multi-sig contracts, protection of data privacy, access to distributed blockchains, and all the other decentralized features. But they should lay them underneath the hood of applications that are consumer-friendly, like mainstream platforms or online banking services.

Second, the DeFi community should create products and services for a greater share of the population. Trading and arbitrage platforms are useful for day-traders and hedge funds, but the people who need DeFi the most are not looking to actively trade crypto assets. DeFi projects must rediscover the original purpose of bitcoin by focusing on peer-to-peer exchange and removing toll-collectors from financial services.

Projects like Celsius Network (of which I’m CEO), Voyager, Compound, and Monarch, among others, are providing more common financial services like lending, interest income, wealth management, and collateralized loans. Offering these services will allow DeFi projects to expand their reach by providing real value to more people across the world, no matter income, age or location.

Third, DeFi providers should be conscious of the fact that many people still feel uncomfortable investing in digital currencies due to price volatility. As such, stablecoins will be an important bridge from centralized fiat assets to decentralized cryptocurrencies. First-time buyers will be surprised to discover they can (a) earn more interest on stablecoins than on dollars in a savings account, and (b) not have to worry about depreciation in the value of their collateral. Resembling fiat currencies, stablecoins can function as a teaser for BTC, ETH, and other decentralized currencies and DeFi projects.

In sum, DeFi and cryptocurrencies can go mainstream, but they need to be as easy to use as Facebook or Google. Just as one cannot throw first-time swimmers into the deep end of the pool and expect them to swim, we cannot introduce crypto novices to complicated DeFi services and expect them to become Hodlers. Let’s concentrate our efforts in 2020 on making DeFi into a movement where everyone can participate and enjoy the fruits of decentralization. After all, Bitcoin just hit its 11th birthday and we’re only getting older.

Celsius To Begin Offering Compounding Interest On Crypto Deposits

Cryptocurrency lending and borrowing platform Celsius announced that it would be implementing compounding interest on cryptocurrencies deposited in its wallet, starting Feb. 1. The announcement came with a number of other updates in a Twitter AMA (ask me anything) with founder Alex Mashinsky on Jan. 22.

Compounding interest was a feature requested by the Celsius community, and brings the community-driven app in line with venture capital-backed competitors like BlockFi, and traditional financial services. In announcement sent to Cointelegraph the firm stated:

“You asked for it, and we delivered! Starting February 1, interest income on crypto deposits will officially be COMPOUNDING! That’s right – all the coins in your wallet will now be earning interest on interest!”

Other changes announced in the AMA covered revamped loyalty tiers, the ability to lend against EOS tokens, and a partnership with South Korean cryptocurrency exchange, Korbit.

Users can also now earn up to 8.1% APR on their first deposited Bitcoin (BTC).

Fastest Growing Crypto-Lender

As Cointelegraph reported lin August 2019, Celsius Network became the fastest growing crypto-lender with $2.2 billion in coin loan origination. By November, the total loan amount had almost doubled again, reaching $4.25 billion.

Crypto-lending platforms continue to grow in popularity, giving holders the opportunity to earn interest on their deposited assets, while also enabling the use of tokens as collateral against cash or stablecoin loans.

Celsius offers varying interest rates on deposits of a wide range of popular cryptocurrencies, including Bitcoin, Ether (ETH) and Litecoin (LTC), along with coins such as Bitcoin Gold (BTG), Dash (DASH), ZCash (ZEC) and EOS. Higher interest rates of up to 10% are also available on a selection of stablecoins.

Updated: 12-18-2019

Kyber Network Aims To Improve DeFi Liquidity With ‘Katalyst’ Protocol Upgrade

Kyber Network, the ethereum-based protocol focused on aggregating liquidity and facilitating swaps for ERC-20 tokens, is about to launch a major upgrade.

Planned to go live in the second quarter of 2020, Katalyst is said to be a major upgrade to the Kyber protocol to better meet the liquidity needs of the decentralized finance (DeFi) ecosystem.

Currently, the Kyber Network (KNC) design allows for any party to contribute to an aggregated pool of liquidity within each blockchain while providing a single endpoint for takers to execute trades using the best rates available.

Katalyst aims to reduce friction in liquidity contribution, introduce rebates for high-performing reserves (liquidity providers) and allow DApps integrated with Kyber to add a custom spread for flexible rates.

Simon Kim, CEO of Hashed, a blockchain venture capitalist firm based in Seoul and California’s Silicon Valley, said the introduction of Katalyst would be able to grow the network exponentially by providing greater incentives for its contributors.

“The Kyber Network has proven its utility as the most reliable liquidity pool for all the participants in the DeFi ecosystem on ethereum,” Kim said.

On top of liquidity optimization, the Katalyst upgrade will include a new staking mechanism and the launch of the KyberDAO, a community platform that allows KNC token holders to participate in governance for the first time.

Joshua Green, head of trading at Digital Asset Capital Management, a cryptocurrency trading firm based in Sydney, Australia, said as the DeFi space continues to move from its development phase to focus on users and transaction execution, liquidity becomes a more prominent driver of continued growth.

“We are excited by a number of projects and the disintermediating models they have developed,” Green said. “Higher levels of liquidity now need to follow to make them more efficient for the widest user base and make their value proposition as strong as possible against centralised peers.”

Trading on centralized exchanges is currently not compatible with DeFi applications since it is technically infeasible to bridge between decentralized applications and centralized servers without compromising the trust model.

KNC is currently up 27 percent over the last 30 days and is up 78 percent year-to-date making it one best-performing crypto assets for 2019. It is currently changing hands for $0.22, according to data provider Messari.

Kyber supports over 70 different tokens and powers close to 100 integrated projects including popular wallets MEW, Trust, Enjin, and the HTC Exodus smartphone.

Updated: 1-30-2020

Coinbase Custody And Bison Trails To Lobby Staking Adoption

Coinbase Custody and Bison Trails have joined the ranks of the Proof of Stake Alliance (POSA), a Jan. 30 press release announced. Together with the alliance, they will advocate for the adoption of clear regulations on staking proceeds, as well as other development initiatives.

The Proof of Stake Alliance is an advocacy group founded in 2019 and featuring more than 18 members. It engages in regulatory and congressional discussions to promote staking-friendly regulation, as well as organizing events and educational initiatives.

As COO at Polychain Capital and POSA board member Matt Perona explained to Cointelegraph, the organization’s primary goal is to change the taxation regime for staking rewards:

“First, POSA is working to address how staking rewards received by token holders are taxed. POSA is currently trying to differentiate tax treatment from bitcoin mining guidance so that staking rewards are taxed on the disposition of the asset (the sale of the reward) as opposed to the receipt.”

Both mining and staking rewards are currently taxed in the U.S. as direct income, which offers a much higher rate than capital gains tax normally reserved for traditional assets.

The Role of Coinbase Custody And Bison Trails

The new members of POSA will be helping the alliance to amend this regulation, as both organizations are deeply invested in the staking ecosystem by providing customers with the means to stake their assets.

A white paper drafted by Abraham Sutherland, a professor at University of Virginia School of Law, argues that the existing treatment is unfair.

In addition to its work on tax regulation, the alliance is also engaging with regulators such as the SEC and FinCEN to work on issues related to securities and money services regulation.

Both Coinbase Custody and Bison Trails will assist POSA in its initiatives. Replying to questions about their specific contribution, Perona explained:

“[They will conduct] meetings on the hill with congressional representatives educating them on Proof of Stake based technologies and their potential use cases. Meetings with regulators (SEC, IRS, Treasury, FinCEN) educating them on the intricacies of the technology and building a regulatory framework that allows for the growth and adoption of staking based technologies. Taking part in working groups and helping implement best practices industry standards”

The alliance’s educational efforts do not include institutions, however. When asked whether POSA is making efforts beyond regulator outreach, Perona replied:

“Currently, POSA is focused specifically on engaging with regulators and policymakers and trying to build a regulatory framework that is conducive to the growth of the staking industry. Our individual members might be having those types of conversations [with institutions] but POSA is not focused on that nor is it a function of POSA.”

Updated: 1-30-2020

Compared To Traditional Banks, Crypto Lenders See Booming Growth

A lukewarm U.S. economy is making big banks like JPMorgan Chase struggle to produce fast loan growth – even with interest rates close to historic lows. Yet, in the white-hot cryptocurrency industry, lenders are burgeoning.

The Commerce Department reported Thursday that U.S. gross domestic product rose at a 2.1 percent annual pace in the fourth quarter, on par with the third quarter’s clip, even after the Federal Reserve cut interest rates three times earlier in 2019 to stimulate growth. For the full year, the economy expanded 2.3 percent, a slowdown from 2018’s 2.9 percent, according to the report.

If there’s any softening in the economy, it hasn’t been felt by lenders like Genesis. The New York-based trading firm that lends cash alongside cryptocurrencies like bitcoin said Thursday in a report that loans increased by 21 percent during the fourth quarter to $545 million, driven by demand from big investors as well as aggregators of smaller loans in Asia and Europe.

Such growth was more than 10 times the pace at New York-based JPMorgan, the biggest U.S. bank, where loan balances increased by 2 percent – roughly the same pace as the economy – during the period to $959.8 billion.

Only a few lenders can be found in the decade-old digital asset industry, and they are starting from a smaller base. There’s also a dearth of competition from established banks for loans to crypto traders and businesses, due to conservative risk-management policies and restrictions imposed by regulators. Since a cryptocurrency like bitcoin can be a highly volatile collateral for loans, more traditional lenders are rare.

But crypto lenders are seeing strong demand from borrowers who want loans denominated in bitcoin, cash or “stablecoins” – digital tokens like tether and USD Coin whose price is linked to the U.S. dollar or other government-issued currencies. And there are plenty of investors willing to pledge cash to lenders like Genesis in exchange for interest rates of 7 or 8 percent.

BlockFi, a big crypto lender backed by the investment funds Galaxy Digital and Winklevoss Capital, said earlier this month it planned to add five to 10 new assets to its platform, including the cryptocurrency litecoin and a dollar-pegged digital token, USD Coin. Later this year BlockFi plans to launch a credit card that offers rewards in bitcoin.

Celsius Network, another crypto lender, said in December large institutional clients were becoming an increasingly key contributor to the platform’s loan growth.

“Obviously the crypto sector is not even a beauty mark right now compared with the banking sector, in terms of the size and maturity,” Genesis CEO Michael Moro said in a phone interview. “But there is rapid growth in this new market, and it’s not just us. There are other companies trying to accomplish similar things.”

Genesis is controlled by the crypto-focused investment firm Digital Currency Group, which also owns CoinDesk.

Bitcoin, the oldest and largest cryptocurrency, surged 94 percent in 2019, more than three times the gains in the Standard & Poor’s 500 Index of large U.S. stocks over the period.

So far in January, bitcoin is up another 30 percent to about $9,300, the best start to a year since 2013. Earlier this month, the professional-network website LinkedIn named blockchain – the cryptographically-enabled computer-network technology underpinning cryptocurrencies – as the most in-demand skill among employers.

Silvergate Capital, one of the few banking companies serving crypto-related businesses, said Wednesday total assets were flat in the fourth quarter at $2.13 billion. But the La Jolla, California-based publicly traded company said it added 48 digital currency customers during the period, bringing the total to 804, while transactions on its digital Silvergate Exchange Network rose by 17 percent from third-quarter levels.

A recently announced initiative at Silvergate will allow customers to obtain U.S. dollar-denominated loans collateralized by bitcoin.

Genesis said in its latest report a new source of demand for cash loans in 2020 could come from “mining” companies that need capital to build, expand or upgrade data centers used to process transactions on the bitcoin blockchain.

“We will likely see miners leverage their existing balance sheet and treasury to source the cash necessary to invest in their operation,” according to the report. “Those unable to source cash will be stuck mining on old-generation machines and might face serious profitability issues if the price of bitcoin doesn’t rise substantially.”

Updated: 1-31-2020

Genesis Crypto Lending Firm Hits New Record In Loan Originations In Q4 2019

Over-the-counter digital currency trading and lending firm Genesis closed the fourth quarter of 2019 with record high results in loan originations since its inception.

Per a Jan. 30 press release, Genesis facilitated over $4.25 billion in loans since its incorporation in March 2018, which made Q4 the best in company history. Genesis originated more than $1.1 billion in loans and borrows for its institutional customers, with total active loans of $545 million, showing a 23% increase compared to $450 million in Q3.

Genesis noted an increase in its active loan book and originations despite a 14% decline in the Bitcoin (BTC) price and other digital assets. The amount of borrowings in U.S. dollars also continued to grow and constituted 37% of the company’s active loan portfolio in Q4 2019.

Crypto Loans Market Highlights

As of December 2019, the entire crypto loaning industry was estimated to be worth $4.7 billion and the number of crypto loan platforms was growing rapidly, according to a report made by blockchain company Graychain Ltd.

While lenders had only earned a combined $86 million in interest since 2018, the demand for cryptocurrency loans was growing. In Q1 2019, over 5,400 new loans were issued, and in the second, at least 18,500. The volume of lending also increased, with lenders issuing $64.8 million in loans in the first quarter and $159.3 million in the second.

Just recently, major cryptocurrency lending company BlockFi added support for Litecoin (LTC) and USD Coin (USDC), and crypto lending and borrowing platform Celsius announced that it would be implementing compounding interest on cryptocurrencies deposited in its wallet.

Updated: 2-1-2020

How Fund Managers View Lending And Staking: 3 Takeaways From A CoinDesk Research Webinar

Not everyone is totally excited about DeFi.

Volatile crypto is nurturing its fixed-income side. Crypto lending activity is growing on decentralized finance (DeFi) networks. Staking, where investors reap payments for locking up assets in functions essential to network protocols, is moving into crypto’s mainstream, with large crypto exchanges offering staking services for users.

There’s some irony in this, like a penny stock offering a dividend, but both lending and staking are emerging as potential factors in investment decisions for crypto investors. In December, we invited two fund managers, both long bitcoin and other crypto assets, for a CoinDesk Research webinar on lending and staking.

Jordan Clifford of Scalar Capital and Kyle Samani of Multicoin Capital joined us to discuss how they evaluate risk and returns in crypto lending and staking, what crypto assets’ risk-free rate might look like and what DeFi needs to do to attract investors and new users.

1. DeFi Risk Factors Keep Some Investors Out.

Clifford and Samani had a back-and-forth about the decision to put assets to work in DeFi networks that earn returns. From Clifford’s perspective, the technology risks are manageable; Samani said at this point the returns don’t justify the risk of losing investor funds to a “smart contract” glitch, for any allocation of assets to DeFi.

Here’s Clifford on how Scalar evaluates risks. He mentioned bug bounties, security audits and formal verification as ways DeFi networks can de-risk themselves as platforms for earning fixed-income returns on crypto. Human risk is a factor, too: “You really are thinking about counterparty risk as the main one. … And that comes in many forms, actually.

Many of these DeFi contracts, they have administrator access that can do various things with those funds at the contract level. This is kind of an early stop-gate for many of these smart contracts to go live before they can be truly decentralized. That’s something to think about. It says it’s a DeFi protocol but often there’s a single organization that has keys to it.”

Whether or not there’s human counterparty risk to consider, there’s always technological counterparty risk, Clifford said, which can be evaluated along the lines of a Lindy effect: “Often, the smart contracts themselves, they act as a counterparty in a way, and they need to be vetted for technology risk. … What you’re really looking for is smart contracts that have had a lot of value custodied within them. The more time that’s elapsed, the safer it tends to be. If the contract’s held a billion dollars for several years the odds of it having a serious vulnerability diminish over time.”

For Samani, current interest rates on DeFilending networks don’t justify the risks, which include potentially having to send an email to investors explaining how the fund lost their money.

“It wouldn’t be meaningful to our portfolio, so it just wasn’t worth the time,” he said. “What rate would be meaningful? Samani said Multicoin hasn’t made that determination, yet. Is it a 1 percent premium over centralized? Is it a 2 percent premium? At what point are we willing to underwrite that? We’re not there yet; we hope to be there in the next six to 12 months.”

Samani said he’s not bullish that decentralized lending will be able to offer substantial premiums over centralized. “There are always going to be people who will bridge that arbitrage,” he said.

2. What Is Crypto’s Risk-Free Rate?

Decisions about what’s a meaningful rate come down to a premium earned for risk taken. This is usually calculated in reference to a “risk-free” rate. Of course, no investment is risk free, and that applies acutely in crypto assets. However, conversation in our crypto lending webinar turned to risk-free rates in crypto and how staking might play a role in determining such a reference point for pricing risk.

“In general my expectation is that lending and borrowing rates will be higher than staking rates,” Samani said. “I think for the most part staking rates, at least within each ecosystem, will be considered the risk-free rate.”

Factors like staking protocols’ programmed unbonding period make it different, but there will be workarounds to such lockups, Samani said. For example, exchanges offering staking services may be able to return capital to their users more quickly than direct staking would allow.

Staking isn’t free of risk by any means, Samani said, but it eliminates additional layers of risk on top of holding the asset itself.

“It’s native to the protocol,” he said. “There’s very few things that are native to the protocol and that is one of the things. My sense is, why deal with borrowing and counterparty risk when you can just rely on the protocol? You’re already relying on the protocol anyways, so if you’re going to rely on the protocol and add counterparty risk you should be compensated for that.”

3. What DeFi Needs In Order To Grow.

Samani wasn’t bullish on DeFi, either. “It’s pretty clear now that it’s pretty circular. There’s not too many people actually using the product. … The upper bound here seems to be the market cap of ETH or some fraction of that,” he said.

Clifford said DeFi needs better user interfaces and applications: “We need to polish off the rough edges, get more time, have people talk about their success stories,” he said. “I think organic growth will come, it’s just going to take a little while.”

Samani thinks DeFi’s growth challenges are more fundamental. Crypto-collateralized loans aren’t interesting beyond the bounds of existing ethereum investors. Uncollateralized loans, serving people excluded from the traditional financial system, would achieve that; they may not be practical without additional technology, like sovereign identity and credit scoring that can cross borders and operate outside traditional financial systems, he said.

Updated: 2-7-2020

Bitcoin DeFi Looms Closer As RSK Launches Ethereum Bridge

The RSK project announced the creation of Token Bridge, an interoperability protocol between the Bitcoin-pegged sidechain and Ethereum, on Feb. 6. It could have important implications for the burgeoning decentralized finance (DeFi) ecosystem.

RSK is a smart contract platform attached as a sidechain to the Bitcoin (BTC) blockchain. It uses a wrapped version of Bitcoin called rBTC as its native token. Users acquire the token by depositing BTC into RSK’s bridge wallet, which works as a two-way peg.

The team has now opened a similar bridge for the Ethereum blockchain. It allows a two-way transfer of any token between the RSK and Ethereum ecosystems. This means that Ethereum users can transact with wrapped representations of RSK’s rBTC and RIF tokens, thus gaining indirect exposure to the Bitcoin ecosystem. The same goes for RSK users, who are exposed to Ethereum-based stablecoins such as DAI.

How Does It Work?

When a user deposits a token from either blockchain to an address provided by RSK, an equivalent amount of the appropriate Side Token is minted in the other chain. The Side Token is written according to the ERC-777 specification, a newer token standard that is backward-compatible with the highly common ERC-20 specification.

Any standard token on either blockchain can be ported to the other through the bridge. The total supply does not change from this operation, as the original tokens are locked up until their mirror image is redeemed.

Cointelegraph reached out to Adrian Eidelman, RSK Strategist at parent company IOVLabs. He explained in more detail how the bridge works, revealing that the current system is not yet fully decentralized.

Eidelman said that to connect the two blockchains together, a federation of “well-known and respected community members” oversees the peg process. The procedure is triggered when developers on either chain interact with the bridge smart contract. Using Ethereum as an example, he explained what happens:

“The original tokens will now be locked on the Ethereum chain, and an “event” is created. At this point, the federation initiates the bridge and sends the information to the RSK chain. Once 50% or more of the federates have voted for the same transaction — the bridge on the RSK chain creates RRC20 tokens for the same amount locked on Ethereum.”

The team does not consider this a fully decentralized measure, but Eidelman reassured that the system should reach “full decentralization” by the end of Q3 2020.

Potential For Bitcoin DeFi

The DeFi movement is largely limited to Ethereum and its token ecosystem, where it recently surpassed $1 billion in locked assets. ETH is used as the main collateral asset to generate the DAI stablecoin through its complex lending system.

Nevertheless, Bitcoin-based DeFi is often considered DeFi’s next frontier. In a November 2019 interview with The Spartan Group, MakerDAO’s founder Rune Christensen said:

“When it comes to a solid decentralized collateral, I think ETH is king. The only thing that can come close to ETH in terms of its importance is of course Bitcoin.”

But Bitcoin has very limited smart contract functionality, which severely limits this use case. Christensen noted that porting Bitcoin into Ethereum would allow for it to be used as collateral, pointing to existing solutions such as Wrapped BTC (WBTC).

However, WBTC’s transfer process is custodial, instead of being a decentralized atomic swap. He explained that “it is essentially impossible to build more decentralized cross-chain solutions.”

The Only Available Solution, According To Christensen, Is To Have Many Providers Of Bitcoin On Ethereum:

“The way that we have to try to solve that with Maker is rather than just for WBTC to be the sole source of Bitcoin on Ethereum, we want to have hundreds of different versions of wrapped Bitcoin.”

Thus the release of RSK’s Ethereum bridge could be an additional step toward Bitcoin-collateralized DAI living on Ethereum.

Though Maker is the biggest decentralized stablecoin provider, it is not the only one. Money on Chain is a similar project built on RSK, which uses rBTC for collateral. The project already expressed interest in using the RSK bridge to enter the Ethereum ecosystem.

RSK also sees a potential use case for Ethereum DeFi to transfer to its platform. Eidelman claimed that the Ethereum market is “experiencing many difficulties,” pointing to higher fees and lower capacity. The project sees itself as an extension of Bitcoin, which it believes is the “strongest ecosystem in the blockchain space.” Despite the close association, RSK is still its own network.

Bitcoin DeFi could be close, but it seems unlikely that it will be based on the Bitcoin blockchain.

Updated: 2-7-2020

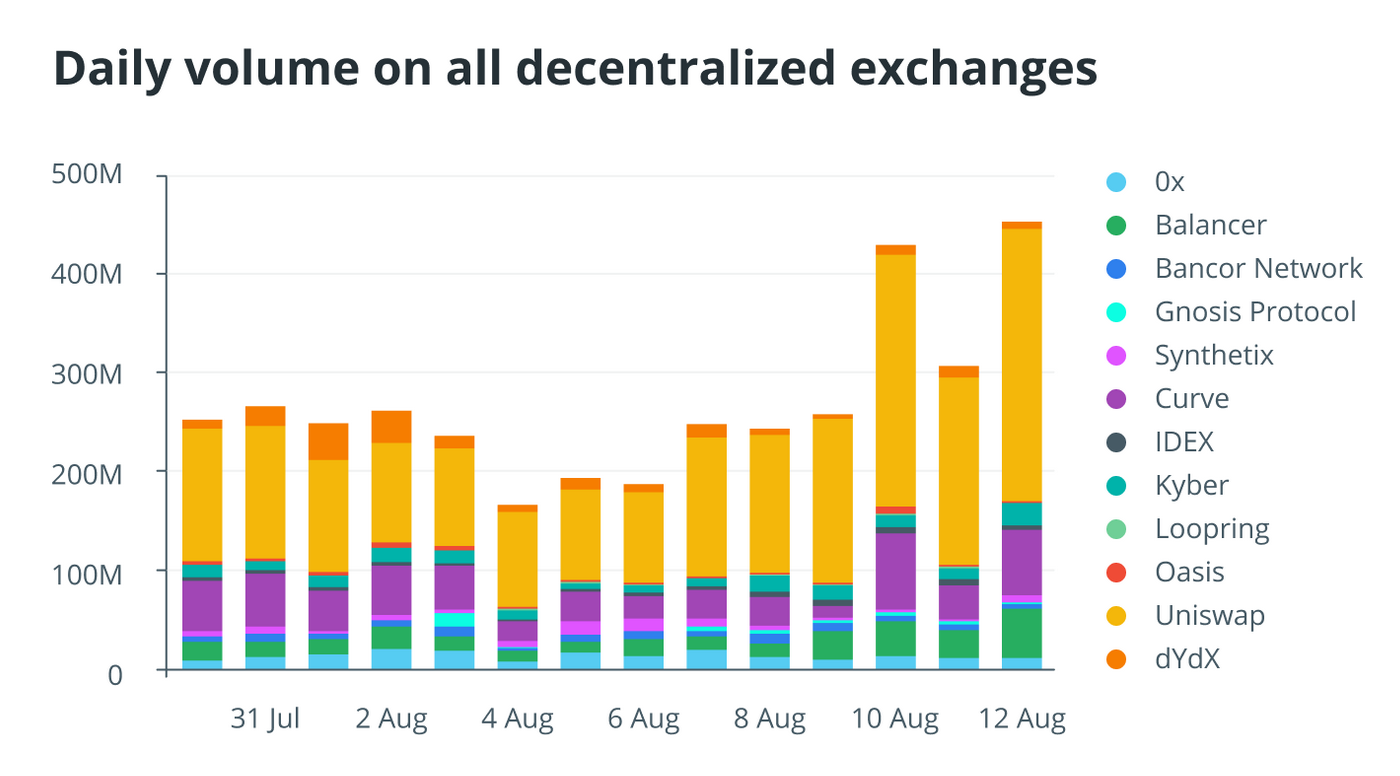

Value Locked In Crypto DeFi Markets Hits $1 Billion Milestone

With Ether (ETH) breaking through the $200 mark yesterday, $1 billion in value is now locked in the DeFi markets.

As of Feb. 7, ETH is trading close to $220 — up 4.5% on the day and almost 22% on the week.

Broadly speaking, DeFi is shorthand for decentralized finance, referring to the use of blockchain, digital assets and smart contracts in financial services such as credit and lending.

According to analytics site Defipulse.com, the $1 billion locked in the markets — i.e. across the spectrum of smart contracts, protocols and decentralized applications (DApps) built on Ethereum — is almost 60% denominated in MakerDAO’s DAI stablecoin.

Defipulse stats reveal that one year ago today, the value locked in DeFi was roughly a quarter of what it is now, at $276 million.

As it celebrates the milestone, some in the Ethereum community have pointed to the role played by the Bitcoin (BTC) lightning network, which accounts for 1.7% of the value ($8.5 million) — making it into the top ten digital assets used for DeFi contracts and applications:

As the site notes, the total value figure is calculated hourly by pulling the total balance of Ether (ETH) and ERC-20 tokens held in DeFi smart contracts and multiplying these balances by their spot prices in USD.

ETH Price Correlation

As Cointelegraph reported last fall, while the dollar value chart of digital assets locked in DeFi shows some correlation to Ether’s price, it is not entirely dependent on it.

After falling with Ether’s price in July 2019, the value of assets locked in DeFi apps resumed its growth even as the altcoin’s price continued largely to fall. In a short time period, the correlation is tighter.

Updated: 2-13-2020

Bitcoin Lender BlockFi Raises $30M In Series B Led By Peter Thiel’s Valar Ventures

Fresh on the heels of an $18.3 million Series A funding round in August, crypto lending startup BlockFi has secured a $30 million Series B.

Announced Thursday, the new funding will help the firm expand both its product offering and geographic footprint.

“We decided to opportunistically raise the Series B to expand the balance sheet and give ourselves the ability to invest in the things we’re doing this year,” BlockFi CEO Zac Prince said in an interview.

The Series B was led by Peter Thiel’s Valar Ventures with participation from repeat investors Morgan Creek Digital, PJC, Akuna Capital, CMT Digital, Winklevoss Capital and Avon Ventures. New investors included Castle Island Ventures, Purple Arch Ventures, Kenetic Capital, Arrington XRP Capital and HashKey Capital.

Having Hong Kong-based HashKey as an investor will help BlockFi expand into Singapore later this year, Prince said. While the company has been serving customers in the region, this would be its first physical presence there.

In the Asia-Pacific region, BlockFi expects to attract a lot of institutional customers, Prince said, given the number of mining companies, asset managers, exchanges and market makers that exist there. BlockFi also plans to begin attracting more retail customers in the region as it translates its site and products into local Asian languages.

In the first quarter of this year, the startup plans to develop a mobile app and the ability to send fiat wire transfers. In Q2 2020, BlockFi plans to offer Automated Clearing House (ACH) payments.

It also expects to double the size of its 75-person team by the end of 2020, Prince said.

BlockFi has been providing fiat loans with bitcoin (BTC) and ether (ETH) collateral since the beginning of last year. In March, it launched a service offering clients interest on their crypto, which the company then loaned out to institutions. BlockFi has had to cut rates more than once because borrower supply has not been able to meet depositor demand.

The firm reports having more than $650 million in assets on its platform, a 160 percent increase from the $250 million in assets it reported in August, with a 0 percent loan loss rate.

Last month, BlockFi announced a slight reduction in yield for customers lending bitcoin and ether, caused by a more bullish crypto market.

Updated: 2-16-2020

DeFi Begins To Move From A Sub-Niche Market To Mainstream Finance

In one year, the total value of Ether (ETH) locked in DeFi markets has increased from $317 million to over $1 billion. With the increasing level of activity in the market sector, the next logical progression appears to be focused on making DeFi solutions more mainstream.

However, like other decentralized apps, DeFi protocols still have issues with usability among everyday users. Factors such as liquidity and governance could also hold serious implications for introducing DeFi products to the broader financial market.

With lending products occupying the greater majority in the current DeFi ecosystem, DApp developers have to consider real-world hitches like loan repayment and defaults. Also, the volatility of crypto prices that act as collateral can exert significant stress on the market.

Currently, solutions like multi-collateralized and non-collateralized lending appear to be gaining some popularity in the market. However, these systems might still require more robust stress testing to evaluate their effectiveness in dealing with internal and external stressors.

Apart from handling price instability, a larger DeFi market could mean greater regulatory scrutiny and more significant competition with legacy finance systems. The crypto market as a whole continues to be subject to even tighter regulatory standards with Anti-Money Laundering being a major focus for governments across the world.

DeFi Market Growth Crosses $1 Billion Milestone

As previously reported by Cointelegraph, the total ETH value locked in the DeFi market has crossed the $1-billion mark. Data from analytics platform Defipulse.com reveals that the current value of the market represents an almost-300% increase from 12 months ago.

In an email to Cointelegraph, a spokesperson for the Maker Foundation highlighted the growth rate of the DeFi market, stating that the pace is exciting, adding: “I believe it speaks to the shared human desire to have more control over critical elements of our lives, like our financial futures and opportunities.” Akiva Lai, chief product officer at blockchain governance and auditing platform Maxonrow, highlighted the significant growth in the DeFi market for Cointelegraph. According to Lai:

“It’s pretty astounding, to be honest. $1 billion in locked DeFi value may seem minuscule compared to legacy finance, but we need to examine it for what it could be — not what it currently is. Paired with the ballooning growth of exchange products, from derivatives to staking services, and it’s only natural that more users will tap DeFi products in the never-ending search for yield amid an uncertain economic backdrop of negative interest rates and slow growth.”

According to Defipulse data, lending DApps command the largest share of the DeFi market, and MarketWatch forecasts that the lending market will reach a valuation of $8 trillion within the next two years. For Jonathan Loi, founder of derivatives exchange platform Level01, the DeFi market is on course for continued growth. In a private note to Cointelegraph, Loi said that the pace of growth is a vote of confidence, adding:

“The majority of value is staked in lending protocols: Because of these protocols collateralized and transparent nature with potential dividend upside, it becomes attractive to investors leading to the quick pace of adoption. Other industries such as financial trading is also gaining pace as evident in the growing interest in direct P2P trading platforms that facilitates transparent and autonomous settlement for the trading of options contracts.”

Lending Holds The Lion Share

Indeed, MakerDAO’s DAI stablecoin accounts for more than 60% of the DeFi market. Thus, lending controls the greater majority of activities in ETH-based decentralized finance. Other major lending products include Compound, InstaDApp and dYdX.

The popularity of lending within the DeFi market space comes as no surprise, given that the total crypto loan industry currently stands at about $4.7 billion. As previously reported by Cointelegraph, the presence of higher interest rates within the sector is driving adoption.

The robust growth in the crypto loan industry comes despite the bear market conditions that characterized the crypto scene in 2018 and 2019. Even with the close to 90% drop in the underlying collateral (usually ETH), crypto loan products have shown some degree of robustness.

DeFi lending proponents will be hoping that such resilience will be pivotal in attracting greater institutional interest in the market. Lai of Maxonrow is of the opinion that DeFi-based lending products could be major drivers for the market as a whole, telling Cointelegraph:

“The biggest impact areas will likely continue to be borrowing/lending because debt is such an integral component of a growing economy. However, collateralized loans still preclude many poorer people from the financial system without collateral to offer, so developments that can lower the barrier in terms of friendly rates and maybe non-collateralized crypto lending are important.”

With greater penetration of DeFi lending, certain market realities like bad debt and loan defaults could come to fruition. Developers and entrepreneurs in the industry will have to contend with the effects of such stressors not only on their products but on the entire crypto market when having to liquidate the collateral backing the bad debt.

According to the Maker Foundation, it is the responsibility of regulated lenders to do their due diligence while offering services to customers. As part of its email to Cointelegraph, a spokesperson for the foundation explained:

“Maker provides the building blocks along with the built-in checks and balances for regulated organizations to provide financial products like loans. Consequently, a regulated loan originator would integrate Maker’s architecture to issue loans that they ultimately are responsible for operating. Originators would do so with the full knowledge that Maker uses a collection of smart contracts to ensure the system on the backend remains secure and robust.”

For Michael Gasiorek, head of growth at stablecoin platform TrustToken, overcollateralized loans will give way to undercollateralized loans as market risks become better understood. Writing to Cointelegraph, Gasiorek explained that they will require to be backed by something additional to crypto, like the trading/loan history reputation, Know Your Customer or AML information, or lead to the creation of a credit score system:

“These opportunities will become mainstream only once the mechanisms, returns and risks are well understood and will most likely happen slowly as institutions (the real mainstream when it comes to making loans at eye-popping quantities) watch crypto-savvy consumers test the market and technology.”

DeFi Moving Toward Mainstream Adoption

The question for DeFi as it moves toward mainstream adoption is whether the emerging market will seek to dislodge legacy systems or run concurrent perhaps maybe even collaboratively with mainstream finance. For Lai, the latter appears most likely:

“Crypto and DeFi won’t subvert conventional finance, it will coexist — with some hybrid components shared between the two. Who knows, maybe in the future, banks will rely on DeFi lending platforms to manage repayment, collateralization and debt swaps while building the liquidity fail-safes and regulatory components (e.g., KYC) on their back-end.”

A mature DeFi market brings with it the possibility of more flexible options for retail investors with some products likely possessing useful trade-offs in comparison to legacy systems. For Alex Melikhov, CEO of stablecoin platform Equilibrium, DeFi’s march toward greater global adoption follows two paths. Writing to Cointelegraph, Melikhov anticipates two scenarios:

“The first is a long-awaited mass adoption that goes beyond the retail approach. This scenario requires that DeFi developers and entrepreneurs have more usability, wider community education, UX simplification, and so on. At some point, we will see ordinary households investing in liquidity pools on Compound.”

According to Melikhov, the second pathway is more sophisticated, and it involves developers expanding their focus from building financial primitives toward more cutting-edge DeFi-based offerings, like the multiple Dai extensions already on offer.

But, to achieve mainstream adoption, DeFi might also need to undergo a simplification of many of the available products. To this end, developers may need to consider on-ramps that ease the transition between fiat-based systems to more digitized marketplaces.

Pain Points For Decentralized Finance

While developers and entrepreneurs work toward enhancing the penetration of the DeFi market, these DApps still require some work in making them more suitable for everyday users. Several commentators agree that improvements of the in-app user interface remain a key factor not just for DeFi products but for blockchain DApps in general.

Regarding the issue, Lai told Cointelegraph: “The problem with DeFi right now is that it’s really only used by crypto enthusiasts in developed countries.” Likewise, Gasiorek identified UI issues as one of the four pain points for DeFi:

“The user experience needs to dramatically improve so as to be usable by the non-crypto layperson from both the user interface and ‘requisite starting knowledge’ level.”

For Gasiorek, moving past the usability hurdle will allow stakeholders to focus on matters like liquidity, which becomes even more significant once scalability increases. Then comes the need to properly gauge the risks associated with the market and the creation of robust regulatory provisions to prevent the emergence of problems like a crypto collateral loan bubble.

The growth in the DeFi market marked one of the main developments in the crypto market for 2019. The focus for 2020 appears to be one of consolidation and more gains that could put the industry in the spotlight of financial regulators, given the increased level of attention being paid to the crypto space.

Updated: 2-16-2020

Ethereum Based Fulcrum Platform Loses 350K USD In ETH

Ethereum-based lending platform Fulcrum has lost 350K USD in ETH due to a flaw in a smart contract that was exploited.

The platform has been shut down for “maintenance” and an investigation is underway to determine details.

The Ethereum based lending platform Fulcrum has fallen victim to a malicious attack. The attack occurred between February 14 and 15 when the attackers took advantage of a vulnerability in the platform’s lending protocol.

The attack occurred in several stages. First, the attacker took a 10,000 ETH flash loan. Then, he used half of the ETH to obtain another loan in wrapped Bitcoin (wBTC) through the Compound protocol. The other half of the ETH went to Fulcrum as collateral in a wBTC bet. The attacker bet that the price of the wBTCs was going to short. The attacker then dumped the wBTCs on Uniswap and caused the price to fall to collect the profits from the short on Fulcrum and pay off the initial flash loan.

The Fulcrum platform was shut down while investigations are underway. Fulcrum is a UX-focused dapp for lending and trading launched in June 2019. The dapp uses the decentralized bZx protocol that allows its native dapps to trade and lend on margin and leverage.

bZx Offers Details Post-Mortem

The attack on Fulcrum was complicated by several reasons. The company behind the platform, bZx, was in a hackathon with the Ethereum community. Therefore, bZx’s responsiveness was delayed.

bZx co-founder Kyle Kistner offered a statement on February 15. Kistner claimed that there was a breach against the contract and a portion of ETH was lost in the process. The loan contract was paused for all operations. Kitstner claimed that no further funds were compromised, but did not offer a specific figure on the amount that was lost. It is estimated that the attacker could have made a profit of 350K USD in ETH.

The company behind bZx said that due to the complexity of the transaction it takes time to understand exactly what the losses are. Furthermore, it claimed that the attacks were not just a swap in Uniswap and that bZx does not use Uniswap as an oracle. bZx claimed:

We have deployed a contract upgrade that we believe will make our system more robust against these type of actions in the future. The upgrade is currently being processed through our timelock. It will pass through in the next 12 hours. At that time we hope to restart the UI.

The company reiterated that users have zero losses. bZx also revealed that the attacker left 600K of wBTC as collateral:

We will be using this to stream interest and exit liquidity to existing iETH holders. This will be done using our admin key. This is an extremely difficult decision for us that we don’t take lightly.

It is estimated that Fulcrum will be back online at 10:30pm MTS. They will then publish a more detailed report on the attack and its complexity. However, the company was criticized by many Fulcrum users. Some demanded more transparency about the facts and others criticized the use of the administration key. This mechanism gives bZx full control over the contract at Fulcrum.

The full report is still awaited for further details. In the crypto-community, the attack has been used to exemplify the vulnerabilities of the DeFi sector. MyCrypto founder Taylor Monahan stated:

Just because your code works doesn’t mean it’s safe.

Updated: 2-16-2020

Mind The Gap: Why ETH Price And DeFi Adoption Aren’t In Sync

In his 1991 book, “Crossing the Chasm,” management consultant Geoffrey Moore defined a crucial gap between the early adopters of a new technology and the larger populations of users that come later. Decentralized finance (DeFi) may now be approaching a gap of its own.

This article focuses on DeFi services that allow deposits of ether (ETH), ethereum’s native asset, as collateral for loans issued in a dollar-pegged stablecoin, DAI. Lending is decentralized to the extent it is managed by an open network of participants, governed by rules and incentives established in a computer program. Borrowers may deposit these stablecoins to earn income, convert them to cash or use them to make leveraged investments in ETH and other crypto assets.

DeFi lending’s gains are impressive, but their relationship to the ETH price bears watching.

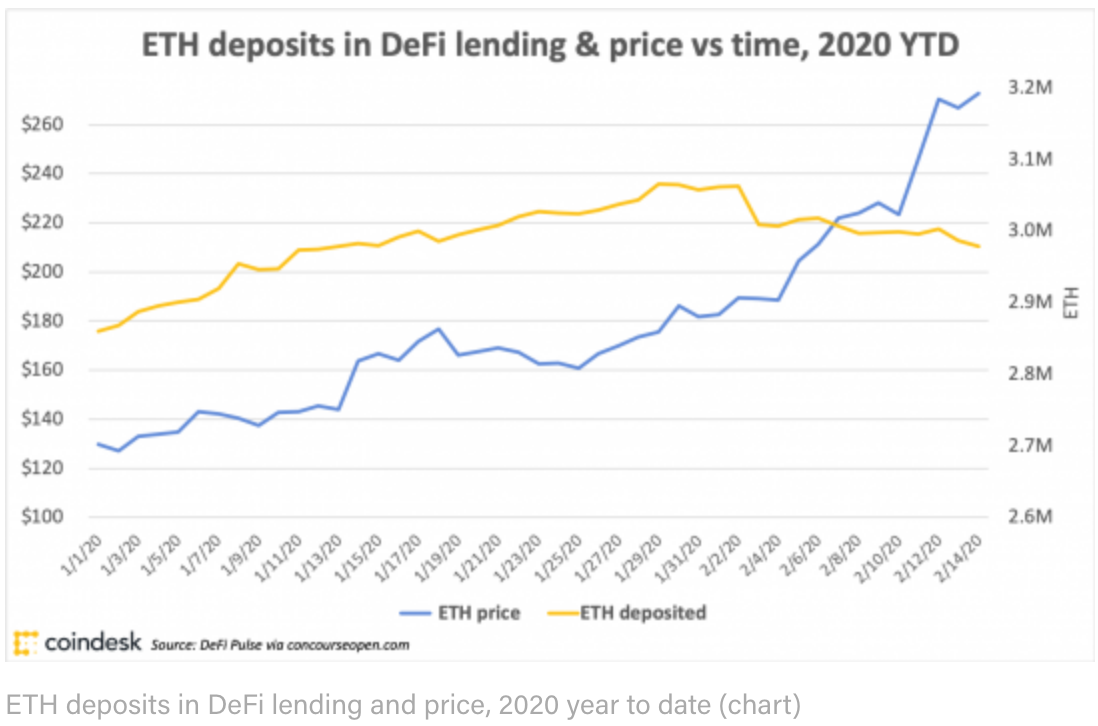

Demand for DeFi lending services built on ethereum shows a pattern of inverse relationship to the price of ETH. When ether prices are falling, the amount of ETH locked in DeFi tends to rise. Most recent data indicate the relationship operates the other way, too. (Data is from DeFi Pulse via Concourse Open.)

If this apparent relationship persists, it may indicate a circular user adoption of DeFi lending that could be limited to a small percentage of the number of existing ETH holders. That is, existing DeFi lending offerings may not be sufficiently attractive to cross the chasm and draw new users into ethereum.

The early adopter in this analysis is the long-term holder of ETH, motivated by conviction that ETH’s value will increase in the future. For such investors, DeFi lending offers a way to earn income or free up capital, as outlined above.

Some of these uses, such as income-earning deposits and cash conversions, may accelerate during dips in price, explaining the apparent inverse pattern between ETH price and ETH locked in DeFi lending. A declining price increases the cost of selling under duress.

Leveraged buying is a possible exception, and proponents of DeFi lending point this way. “What DeFi is creating is a virtuous cycle where investors who have higher risk tolerance are locking up ETH to generate Dai and leverage long ETH,” Mariano Conti, head of smart contracts at MakerDAO, told CoinDesk Research.

Currently, Maker, the largest DeFi lending operation by ETH deposits, has a minimum collateralization ratio of 150 percent, meaning $150 worth of ether is required as collateral to borrow $100 worth of DAI. The leverage implied by this ratio is 1.67X.

Liquid derivatives markets like BitMEX, Huobi and OKEx offer up to 100x leverage on crypto assets including ETH. With these options before them, how many long-ETH investors are likely to choose DeFi lending as a means to leveraged trading?

It’s also difficult to envision adoption among a wider market of borrowers not yet initiated into crypto investing. Would a Main Street borrower purchase ETH in order to obtain a cash loan worth less than said ETH? Perhaps, if DeFi lenders could accept non-crypto collateral. This would not be a trivial development.

“I see lots of startups playing with identity type solutions to reduce collateral requirements, but I think these are a long ways out from meaningfully impacting the market,” Kyle Samani, managing partner of Multicoin Capital, told CoinDesk Research. “There are a lot of hard, intertwined problems to make this work.”

As for that inverse relationship between ETH price and ETH deposits in DeFi lending, if it persists it may indicate the category is approaching an adoption limit. If the inverse relationship is broken or reversed, that may signal DeFi lending has indeed found a set of use cases capable of bringing it, and ethereum, to a wider market.

Updated: 2-18-2020

Meet The Network Investor: A Venture Capitalist Who Invests In DeFi

As initial coin offerings and their derivatives continue to fade, venture investment in the space has steadily picked up pace. Cointelegraph sat down with Michael Anderson, co-founder of Framework Ventures, to learn more about his investment philosophy and outlook on the ecosystem.

Anderson’s most notable investments are Chainlink (LINK) and Synthetix, both of which grew tremendously in 2019. Predictably, he is quite positive about decentralized finance (DeFi), sharing his thoughts on the evolution of the ecosystem after a round of questions on venture investment in crypto.

Venturing Out To Crypto

Anderson came on the venture capitalist (VC) path by passing through tech companies first. Introducing himself, he said:

“My background largely stems from traditional technology. I started working at Dropbox, worked there for four years and then moved to Snapchat. For both of those companies I was a product manager, focused mostly on payments and commerce […] I’ve seen what it was like on the traditional side during the day, and then on nights and weekends I was studying, researching and playing around with all of this new novel technology.”

Together with his partner Vance Spencer he founded Hashletes, a company releasing non-fungible tokens. The company was later sold, with both of them subsequently founding Framework Ventures.

Anderson Explained What Compelled The Duo To Open An Investment Fund:

“One of the things that we realized when we were starting the firm is that there was a major gap for protocol investing. Traditional VCs were just buying and holding or biasing towards equity. Tech companies were building on top of these protocols or building protocols themselves.

Hedge Funds Were Just Trading These Or Thinking In Short Terms.”

The Framework founders believed that investing in protocols required a change of principles. For this reason, Anderson referred to his fund as “Network Capital,” in a wish to not be conflated with traditional venture investors.

The fund primarily deals with token-based investment, as “that is where most of the value accrue is.” But it also invests in company equity and builds tools on top of the protocols with which it is involved.

Crypto Investment Philosophy

Both Spencer and Anderson were active as angel investors in the years before founding Framework. That may explain why some of the fund’s principles have a lot in common with angel investment.

Anderson emphasized that Framework has a long-term vision for all the projects it invests in — even at the cost of delaying an exit. Despite the significant rallies that both Chainlink and Synthetix saw last year, the fund is still deeply invested in both projects.

When asked how Framework feels about investing in a space where companies and projects generally have little to no revenue, Anderson noted that “it is different and it requires a different mindset.”

While the fund will also invest in more traditional companies that have a clearly defined legal entity and revenue, Anderson believes that the value of an open network flows to its token.

Without clearly defined metrics, the valuation method of a project has to change as well. Anderson explained:

“The general idea of what we evaluate, frankly, has nothing to do with price. It has something to do with comparative price to other comparable projects. But frankly, all we look at is qualitative analysis.”

The project’s roadmap holds some weight in this analysis, allowing the investors to gauge its potential. Market evaluation is also crucial, with the duo identifying the importance of oracles and synthetic assets even before any investment.

Yet, the final investment decision still hinges on the personalities behind the project — like with angel-based seed funding. When discussing what compelled the venture fund to invest in both Chainlink and Synthetix, Anderson focused on the founders:

“Our view was that this guy, Sergey [Nazarov, founder of Chainlink], has been in the space since 2013. He’s tried to build smart contract platforms before, and Ethereum kind of beat him out there. So he knows what it’s like to go through the rigamarole. But then also the implicit backing of Cornell and the Cornell research team at IC3 […] That’s what gave us confidence in Chainlink.”

As for Synthetix, Anderson met with its founder, Kain Warwick, even before any kind of investment discussion:

“I ended up sitting next to Kain from Synthetix at a Chainlink dinner at ETHBerlin last summer. And I just got to know him and really got to know what he was about.”

Nevertheless, Framework’s broader investment strategy is dictated by its vision for the future of crypto.

DeFi’s Potential

Framework Ventures currently focuses on decentralized finance, a niche that has steadily grown in 2019. Anderson laid out the investment thesis:

“If we break down what blockchain enables in the core function itself, it’s trustless transfer of value. And when you have trustless transfer of value, its programmability is essentially what DeFi is.”

He added that he believes a broader Web 3.0 is still coming in the future, but DeFi is the current focus of the fund. Yet in its existing form, DeFi is mostly used for leveraged trading of crypto assets. As Anderson explained:

“A lot of the stuff that’s going on right now is almost recursive […] especially Maker. Over-collateralized loans as a concept is just a very inefficient model.”

Answering a question whether DeFi will branch out into non-trading use cases, Anderson replied: “Quick answer is yes. I think the bigger, broader question is when.”

He revealed that Framework is currently looking into under-collateralized loans, powered by social or identity checks.

Decentralized Insurance

As DeFi continues to mature, the space where Anderson currently sees the clearest potential is insurance:

“Insurance could also be a huge thing. Fifty percent of the cost of an insurance company, which usually has a one to two percent profit margin, is based around the headcount and the claims process. So if you can streamline even just a small portion of that 50% of the cost structure, there is a highly profitable insurance company coming out of there.”

Decentralized insurance is one of the potential applications of highly advanced oracles, and both Framework and Chainlink are aware of that, as Anderson revealed.

He envisioned a potential scenario where car sensors would pick up all the necessary data and send it to a smart contract for processing claims — streamlining the existing process. “Obviously, this is a further out vision than where we are right now,” he conceded.

When asked whether smart contracts and blockchain really have a use in this vision, he noted that an open network for insurance would have a strong competitive advantage over traditional companies, taking Geico as an example:

“I think one of the one of the benefits of having an open network is that you’re able to build the collateral pool that Geico currently has based on finding counterparties to underwrite risk. […] Geico […] has been around for almost 100 years, if not over 100 years. So they’ve been able to build this war chest of collateral. […] If we can bootstrap that in an almost peer to peer manner and in a distributed network, I think that’s a huge advantage.”

Updated: 2-20-2020

Celsius Joins Major Cryptocurrency Firms Using Simplex’s Fiat Onramp

Cryptocurrency businesses worldwide are continuing to integrate fiat onramps into their operations in an effort to make it easier for customers to jump into crypto.

United Kingdom-based cryptocurrency lending startup Celsius Network has launched in-app crypto purchases via a new partnership with Simplex, according to a Feb. 18 announcement.

Simplex, a popular fiat-to-crypto payments provider servicing major crypto exchanges like Binance, will now unlock direct crypto purchases for Celsius app users.

Celsius clients will now be able to buy cryptocurrencies like Bitcoin (BTC) and Ether (ETH) via credit or debit cards. Similar to other Simplex-powered fiat onramps, the new feature supports major credit card issuers including Visa and Mastercard.

The U.S. Dollar Is The Only Fiat Currency Accepted At Launch

Apart from providing Celsius users with in-app crypto purchases, the new partnership will significantly cut the cost of unloading Bitcoin on the platform. According to Celsius, the addition of Simplex cuts transaction fees by at least 50%, providing crypto purchases through credit cards at a 3.5% fee.

At launch, Celsius will only accept the United States dollar for the new payment option, a company spokesperson said in an email to Cointelegraph. Additionally, the amount of monthly crypto purchases will be limited at $20,000.

Founded in 2014, Simplex has emerged as a major crypto-enabled payment processor. On Feb. 14, Simplex unlocked 15 new fiat currency payment options for Visa and Mastercard purchases on major cryptocurrency exchange Binance. Previously, Simplex provided its services to major fiat-crypto trading platform OKCoin as well as Singapore-based crypto exchange KuCoin.

Total crypt loan origination on the Celsius Network reached $4.25 billion in late 2019.

Updated: 2-20-2020

Everything You Ever Wanted To Know About The DeFi ‘Flash Loan’ Attack

There’s now a case study for how DeFi can go awry.

bZx, the eighth-largest decentralized finance project according to DeFi Pulse, suffered two attacks last weekend following the introduction of “flash loans,” a new DeFi feature that limits a trader’s risk while improving the upside.

Led by CEO Tom Bean, the bZx team was attending ETHDenver, a major ethereum conference in Colorado’s capital, on Friday when an unknown attacker drained about $350,000 worth of ether (ETH) from Fulcrum, the startup’s lending platform. As a post-mortem from the firm describes, the attacker took advantage of pricing data and a bug within the bZx protocol’s code to secure the payout.

bZx quickly shut down Fulcrum using a decidedly non-decentralized master key. Users and analysts saw an update hit GitHub, the code repository, that supposedly locked down endangered funds.

Trading resumed over the weekend with the firm announcing its intention to contain the damage in a variety of ways, including liquidating collateral to pay a now-uncovered loan, building an insurance fund and spreading losses across platform users.

Despite the shocking incident, traders who had deposited money on bZx will barely feel the effects of the attack.

But that wasn’t the end of it. On Tuesday, Feb. 18, attackers hit bZx again, netting $633,000.

While the amounts of money lost are still relatively small for the world of cryptocurrency, the attacks demonstrate DeFi’s move into the big leagues and the attention it will now receive from manipulators and thieves.

If all this has been making your head spin, you’re in good company. Blockchain technology was complicated and abstract enough before people started building lending and trading services on top of it.

For the perplexed, CoinDesk offers the following explainer of the bZx hack and its broader lessons.

The New Frontier

As the name implies, DeFi, or decentralized finance, aspires to one day offer a democratized alternative to the legacy financial system, where individuals can obtain credit on a peer-to-peer basis without relying on banks or other middlemen. For now, though, it’s a playground for traders – and a rough one at that.

Since the participants don’t know each other, DeFi lending is all based on collateral. Digital assets such as bitcoin (BTC) and ether (the native cryptocurrency of the ethereum network) are notoriously volatile. To deal with this, DeFi lending applications such as MakerDAO let you borrow only 75 percent of your available collateral.

If the price of your asset begins to drop against the market, the smart contract underpinning the DeFi application will sell your asset at a certain spot price in order to protect the parties who loaned you money against your asset. Think of a pawnbroker who will only advance you $225 for an electric guitar worth $300.

The DeFi ecosystem also includes decentralized exchanges (DEX), where traders swap crypto assets without a central authority’s permission, their orders executed algorithmically on the ethereum blockchain.

Trading on-chain limits the range of assets involved to those that run on ethereum (native currency ether and various flavors of ERC tokens). But it allows sophisticated users to do some interesting tricks, as we’ll see shortly.

For a DeFi credit market to run properly, lenders must know the value of the collateral, so they need pricing information. This is data often gathered from crypto exchanges. In bZx’s case, the source was Kyber, a DEX.

The trouble is, crypto exchanges’ price information is all over the place.

Take as a loose example the spot-value differences between the top five exchanges by 24-hour volume for the most liquid digital asset, bitcoin.

Spot prices are often very different from one another because no single venue owns a crypto trade pairing product, said Sergey Nazarov, CEO of Chainlink, a crypto price data firm. Unlike in the traditional markets, where trading of, say, Apple shares happens only on Nasdaq, in crypto most anyone with the technical know-how can spin up an exchange on their laptop – in fact, that’s how the first exchanges started. Aggregating prices across such a fragmented market is a Herculean task, Nazarov said.

As in other financial markets, the wide discrepancy in prices also creates opportunities for traders to make money. Enter flash loans.

Too much information? For a simpler explanation, listen to our Markets Daily podcast.

Flash loans are a further innovation on top of DeFi and ethereum, the blockchain most often associated with the concept of “programmable money.” The product was first released by DeFi protocol Aave this January and then by bZx on Feb. 10.

In short, flash loans allow traders to take out uncollateralized loans to increase the payout of a singular trade. Returning to the pawnshop analogy, you can borrow the cash without surrendering your guitar.

Why would any lender agree to this, especially in a market where participants are anonymous? Because as the name implies, flash loans are paid back quickly – in the same transaction in which they are taken out.

Who would borrow money just to pay it back immediately? Clever arbitrageurs, that’s who.

As we’ve seen, different crypto markets have different prices for a given digital asset. A user can turn a quick profit by borrowing funds; buying low on one market; selling high on the other market; repaying the loan; and pocketing the profit.

Again, this is all done within the same on-chain transaction, since the markets are DEXs often running on ethereum. The arbitrageur just had to code all the steps into the same computer program, known as a smart contract.

To boot, flash loans are nearly risk-free, at least for the borrower. Since the ethereum network settles transactions atomically, meaning all transactions on a book execute or none do, a trader who cannot pay back his loan with his trade loses nothing.

Why? Because the transaction never occurs.

As Aave writes, all transactions, from the loan to the trade, take place at once on the network. If the network sees that a flash loan would not be instantly repaid, it will refuse every transaction associated with it, in effect canceling the whole thing. No harm, no foul.

If it goes through, however, everything is executed at the same time, resulting in a successful trade. The lender collects a small fee, the trader is richer. Everybody wins.

If only it were so simple.

The Attack

As bZx’s weekend woes showed, flash loans can be dangerous when combined with buggy code, janky price feeds or both.

Instead of just buying low and selling high, the attacker or attackers used the borrowed funds to manipulate markets that were unusually vulnerable to it. In both attacks, bZx got the short end of the stick.

In the first attack, for example, through a complex web of transactions, the attacker pumped and then dumped WBTC (“wrapped bitcoin,” an ethereum token backed by actual bitcoin) on a DEX called Uniswap; took profits in ether; repaid the flash loan — and stiffed bzX on another loan related to the WBTC pumping.

“The magic under the hood is the fact how the Uniswap WBTC/ETH was manipulated up to 61.4 for profit,” according to an analysis by blockchain security firm PeckShield. “The WBTC/ETH price was even pumped up to 109.8 when the normal market price was at only around 38. In other words, there is an intentional huge price slippage triggered for exploitation.”

In this attack, a poorly set-up price feed certainly did not help, but the blame falls on the code, PeckShield CEO Jiang Xuxian told CoinDesk. Where a security wire should have been tripped as the price got out of whack, it failed to go off, Xuxian said.

The second attack came down to bad price data, specifically from DeFi network Kyber, bZx co-founder Kyle Kistner told CoinDesk. This time, the attacker focused on Synthetix USD (SUSD), a dollar-pegged stablecoin on the Synthetix Network.

The attacker borrowed 7,500 ether on bZx then pumped the value of SUSD on Kyber by swapping ether for SUSD. The purchase of so much SUSD caused the price to jump 2.5x the prevailing market rate of $1, writes PeckShield.

The attacker then took advantage of bZx’s dependency on Kyber for pricing data, putting up the SUSD as collateral for a large sum of ether on bZx; in fact, 2,000 more ether than the same amount of SUSD would have normally purchased on an open market.

After paying back the flash loan, the attacker reneged on paying back the under collateralized SUSD/ETH loan just taken out on bZx, resulting in a tidy 2,378 ETH profit and bZx holding buttons.

Lessons For DeFi

For smaller exchanges such as bZx, and DeFi in general, the pairing of innovative financial features like flash loans with systematic reliance on bad pricing data is exposing exchanges to new attacks, said Chainlink’s Nazarov.

“Do not use [a] single specific exchange as a price feed,” Nazarov said, “If it becomes thinly traded, people look at and they say, ‘Okay, this is how I’m building a product against this market or against that piece of data.’”

In fact, the specific attack against bZx was described months before it occurred by white-hat hacker Samczsun in a detailed blog post. As Samczun wrote at the time, hypothesizing an exploit involving bZx, the ethereum token known as DAI and another decentralized exchanges called DDEX:

“By relying on an on-chain decentralized price oracle without validating the rates returned, DDEX and bZx were susceptible to atomic price manipulation. This would have resulted in the loss of liquid ETH in the ETH/DAI market for DDEX, and loss of all liquid funds in bZx.”

Nazarov said the issue is not specific to bZx, but many exchanges within DeFi which rely upon a few on-chain pricing APIs. His firm is now working with bZx on addressing the issue, he added.

Kistner acknowledged the bZx team believed the oracle problems were considered fixed after Samczsun’s disclosures and even had the code independently audited. As Tuesday’s attack showed, the problems were not fixed.

“It’s terrible to have consulted with security professionals but then be made a laughingstock when you follow their advice,” Kistner said.

As Nazarov pointed out, you can have all the auditors in the world greenlighting your code, but if it is based on poor data such as on-chain pricing, failure is inevitable.

“The technical risk here is not just about contract code. The code can be fantastic and audited as much as you want. But what’s going on is that you’re creating new functionality which creates new surface areas which need to be secured,” Nazarov said.

Nazarov said the attacks, although unfortunate, are a lesson for DeFi in general. Pricing data is “a well-known architectural issue” that needs to be addressed, he said. “If you’re building an app that’s going to hold client funds, the fact that it’s automated is great, but it doesn’t mean that your work from a security point of view is done because the contract goes on ethereum.”

At bZx, the team has turned its attention toward securing the network. Kistner said trading will resume again shortly using Chainlink oracles for pricing, although no new users will be onboarded. For the future, Kistner said bZx will look at replicating the infrastructure of MakerDAO, the largest DeFi provider.

“When we are done revamping our internal processes, we want to set a standard for both security and transparency,” he said.

Updated: 2-20-2020

DeFi Insurance Firm Nexus Mutual Makes Its First Payout Following bZx Attacks

Insurance works in crypto so far, though it hasn’t had many big tests yet.

Not many people had insurance on assets locked up in bZx’s Fulcrum, but after a bug yielded an exploit of its smart contract, a couple of accounts that did were covered by Nexus Mutual, the London-based crypto insurance company.

Nexus Mutual is an insurance company that works as a cooperative (as any company with “mutual” in its name does), so there’s been lingering doubts that its members would actually pay out against valid claims. But after the post-mortem from bZx came out on Monday, two claims worth approximately $31,000 were paid out, according to the company.

“It’s never good that people are losing money because there’s a hack, but we are able to prove that the system works,” Nexus Mutual founder Hugh Karp told CoinDesk.

In a mutual insurance company, policyholders govern the insurance pool. In Nexus Mutual’s case, that means actually voting to render a decision on each claim.

The money in the mutual account is actually held by the people who hold the Nexus token, NXM. So the question has been: Will people vote to pay out of what is their pool of money when a valid claim gets filed?

Nexus did so, but only on the second try. The company detailed its logic in a blog post Wednesday.

Lasse Clausen, a founding partner at 1kx Capital and early backer of Nexus Mutual, is very happy the policies were honored.

“I do think it’s important that the mutual pays out so that people actually trust it,” Clausen told CoinDesk.

Nexus is a pioneer in insuring smart contract risk. Opyn recently launched a hedging option with similar benefits, but it has a higher collateralization threshold. Nexus, though it introduces more friction to policyholders, can likely provide policies more “capital efficiently,” Karp explained.

How Nexus Works

Right now, people can take out policies against any valid smart contract on ethereum. The policies are just bets against whether or not the smart contract will fail in some way.

“It’s not like an indemnity contract, where we only cover the actual loss,” Karp explained. That is, it doesn’t work like most insurance that retail customers would be familiar with from the analog world.

In fact, a person doesn’t even need to be a user of a smart contract to take out a policy. They just name an amount of insurance, a time period and a smart contract. Then Nexus gives them a price.

If an exploit occurs on a smart contract that mutual members agree represents a failure of the smart contract, then policies get paid out. In that way, it’s basically a bet on the soundness of a product.

All voters have to stake NXM to vote. In order to make sure mutual members participate, voters get paid in new NXM tokens to participate. New token emissions are proportional to the size of the payout, and only those who vote on the winning side earn the new emissions.

Nexus is a venture-backed company, whose lead investors are 1confirmation and Blockchain Capital. At launch in May 2019, three million NXM tokens were created and parceled out to the company and its investors.

More tokens can be purchased on the site at any time but they become more expensive when Nexus has its insurance obligations well-covered. When more policies get taken out and the mutual needs more funds, the prices drop to entice new investors to join in.

After a vote, token stakes only get slashed if the Nexus Mutual board determines malicious behavior. Otherwise, voters just get their stakes back.

“It’s very hard to determine the difference between a difference of opinion and a malicious outcome,” Karp said.

Two Votes

It took two votes to get to the payout in the bZx case.

As soon as the attack was found, claims were made on the Fulcrum smart contract. Mutual fund holders voted those down because at that point it looked like attackers had manipulated the oracles Fulcrum looked at, which didn’t count as a failure of the smart contract itself, in Nexus Mutual’s documentation.

“For the first attack, it’s a smart-contract vulnerability, which they subsequently fixed. This is basically based on my opinion as a smart-contract auditor,” Quantstamp’s Richard Ma told CoinDesk.

Then, on Monday, bZx released a post-mortem that admitted to a fault in its code, where a fail-safe failed. Once this was out, two claims were submitted – both second attempts from the prior round that had been rejected. These were both approved by token holders, as there was evidence of a failure of the contract itself.

Even without the bug, Ma said, the oracles remain a point of potential manipulation. As long as a smart contract can be tricked into thinking an asset is worth more than it actually is, an attacker could potentially borrow more than their collateral is worth.