Big (4) Audit Firms Blasted By PCAOB And Gary Gensler, Head Of SEC (#GotBitcoin)

Fired KPMG Audit Head Fined Over Failure To Supervise Senior Auditors (Updated: 4-5-2022) Big (4) Audit Firms Blasted By PCAOB And Gary Gensler, Head Of SEC (#GotBitcoin)

The PCAOB said it is the first time the U.S. audit watchdog has brought such a charge against an individual.

Related:

The Miracle Of Blockchain’s Triple Entry Accounting

Ernst & Young Introduces Tax Tool For Reporting Bitcoin

Big (4) Audit Firms Entwined In Conflicts Of Interest In Push For ESG Compliance

Ultimate Resource For Money Laundering, Spoofing, Market-Rigging, Etc. In Banking Industry

Ultimate Resource On Insider Trading

The Financial Action Task Force (FATF) Is A Scam

Blockchain And Government-As-A-Platform AKA Algorithmic Regulation

The Public Company Accounting Oversight Board said it fined the fired former head of KPMG LLP’s U.S. audit business $100,000, the largest monetary penalty it’s ever imposed on an individual in a settled case.

Scott Marcello in 2017 was fired as the professional-services firm’s vice chair of audit over a leak of confidential information. KPMG at the time said it terminated Mr. Marcello and four other partners for mishandling a tip that gave the firm improper advance word about which of its audits the PCAOB planned to scrutinize in its annual inspections.

The so-called “steal the exam” scandal led to KPMG paying a $50 million settlement with the Securities and Exchange Commission in 2019 and a one-year prison sentence for Mr. Marcello’s deputy, David Middendorf, who later appealed his conviction.

The U.S. audit watchdog on Tuesday said Mr. Marcello failed to reasonably supervise senior auditors who engaged in the scheme to improve KPMG’s inspection results. The PCAOB said the case marks the first time it has imposed sanctions for a failure to supervise employees. The SEC, which oversees the PCAOB, rarely charges firms or people with failure to supervise in its enforcement actions.

Previously, the largest fine on an individual in a PCAOB settlement was $75,000, which it imposed in 2009 against former Deloitte & Touche partner Thomas J. Linden for allegedly helping a client avoid restating financial results.

The biggest penalty on an individual subject to litigated disciplinary proceedings was $100,000, which was imposed in 2015 against Hamid Kabani, president of accounting firm Kabani & Co.

“The PCAOB is committed to sanctioning top-level personnel at the largest firms when they fail to take sufficient supervisory steps aimed at preventing violations by their subordinates,” PCAOB Chair Erica Williams said in a statement. “The board believes it is important to hold Mr. Marcello accountable as their supervisor for contributing to a culture that led to this serious misconduct.”

KPMG, in response to the sanctions Tuesday, said it is a stronger firm as a result of the actions taken since 2017 to bolster its culture, governance and compliance program. “Integrity and quality are paramount for KPMG, including operating with the utmost regard for the critical importance of the regulatory process to our profession,” a KPMG spokesman said.

Mr. Marcello didn’t immediately respond to a request for comment.

The sanctions come months after Ms. Williams took the helm of the PCAOB and three others joined the five-member board. The SEC last November appointed new PCAOB board members after firing the former chair, William Duhnke, in June.

The PCAOB disciplines audit firms and individual auditors for violations in addition to setting audit standards and inspecting audits.

The PCAOB disclosed 18 enforcement actions in 2021, up from 13 the prior year but down from the previous five-year average of nearly 29, according to a calendar-year analysis of regulatory data by Cornerstone Research, a financial-consulting firm.

The PCAOB under new leadership is expected to increase its scrutiny of audit firms, further incorporate investor concerns into its work and potentially strengthen its approach to enforcement, accountants and former regulators have said.

Updated: 7-25-2022

KPMG Is Fined $17.3 Million In U.K. For Audit Shortfalls

The fine came in relation to two audits, one involving the now-defunct Carillion. Four former KPMG employees were also fined and temporarily banned from the profession, and a fifth was reprimanded.

The U.K.’s audit and accounting regulator fined KPMG LLP and sanctioned five former employees for providing false and misleading information in relation to two audits, one of them of the now-defunct Carillion PLC.

On Monday, the Financial Reporting Council said KPMG was fined £14.4 million—equivalent to $17.3 million—for failings related to the audits of construction and outsourcing giant Carillion and Regenersis PLC, a data-security company that has been renamed Blancco Technology Group PLC. The fine was reduced from £20 million to acknowledge KPMG’s own reporting of misconduct as well as its cooperation with the regulator.

An audit and accounting industry tribunal imposed the fine, saying KPMG provided false and misleading information and documents to the FRC. The tribunal also ordered KPMG to appoint an independent reviewer to consider the effectiveness of the firm’s policies and its engagement with audit inspectors. KPMG agreed to pay £3.95 million in costs related to the investigation.

Four of the accounting firm’s former employees were fined and banned from the auditing profession for varying numbers of years. A fifth was “severely reprimanded,” the FRC said.

“I accept the findings and sanctions of the tribunal in full,” Jon Holt, chief executive of KPMG UK, said in a statement. “The behavior underlying this case was wrong and should never have happened.”

Of the five former employees, Peter Meehan, a former partner, received the most severe penalty, with a ban of 10 years from auditing and a £250,000 fine.

Mr. Meehan, who led the fiscal 2016 Carillion audit, acted alongside Adam Bennett, Alistair Wright and Richard Kitchen to mislead audit inspectors with respect to year-end clearance meeting minutes and an audit working paper, according to the FRC. Pratik Paw followed instructions from Mr. Wright to create the false meeting minutes, the FRC said.

Mr. Meehan’s representatives didn’t respond to a request for comment.

The tribunal found Messrs. Bennett and Wright either had a role in or made false or misleading representations to audit inspectors related to Regenersis’s fiscal 2014 audit. Both men were banned from auditing for eight years and fined: Mr. Wright £45,000, and Mr. Bennett £40,000.

Representatives for Mr. Bennett and Mr. Wright didn’t respond to requests for comment.

Mr. Kitchen, whose representatives declined to comment, was banned from accounting for seven years and fined £30,000.

Representatives for Mr. Paw—a 25-year-old junior auditor when he worked on the Carillion account—noted that the tribunal found that he had failed to question the instructions given him, but not that he had acted dishonestly.

“Pratik deeply regrets not questioning these instructions from his superior and has learned a great deal from his conduct at the time, especially so early in his career,” the representatives said.

Separately, Stuart Smith, who had led the Regenersis audit for KPMG, in January reached a settlement with the FRC in which he agreed to a £150,000 fine and a three-year ban from the profession.

The £14.4 million fine was the second largest ever issued by the FRC, after a £15 million penalty against Deloitte in 2020 in relation to its audits of software company Autonomy Corp. Deloitte is a sponsor of CFO Journal.

Spurred by the collapse of Carillion in early 2018, the U.K.’s audit and accounting sector is set to be overhauled.

The revamp, which includes creation of a new regulator to replace the FRC—called the Audit, Reporting and Governance Authority—has been criticized by industry observers for being slow to take form.

Misconduct that thwarts the FRC’s ability to monitor and inspect audit quality is “extremely serious,” Elizabeth Barrett, the FRC’s executive counsel, said in a statement.

The tribunal’s full report is expected out in “due course,” an FRC spokesman said. A separate investigation into the quality of KPMG’s audits of Carillion’s financial statements remains ongoing, he added.

Updated: 7-27-2022

SEC’s Gensler Says PCAOB Has Been Sluggish In Rulemaking

The chair of the U.S. securities regulator also urged audit firms to review and enhance their independence protocols with respect to their auditing and consulting practices.

Securities and Exchange Commission Chair Gary Gensler said the U.S. audit regulator has been slow to update its rules, in a speech marking the 20th anniversary of the law that created it.

The Public Company Accounting Oversight Board, created as part of the Sarbanes-Oxley Act, continues to work with interim standards that it was allowed to use from the American Institute of Certified Public Accountants, a professional association whose guidelines and rules are often used as fallbacks for the industry.

“The expectation was that the board would produce a more appropriate set of standards going forward,” Mr. Gensler said on Wednesday at an event hosted by the Center for Audit Quality, a U.S. accounting-industry group. “Historically, though, the PCAOB has been too slow to update auditing standards.”

Mr. Gensler, during the speech, also said the Chinese government needs to decide whether to comply with U.S. law in order for Chinese companies to remain listed on U.S. stock exchanges.

The issue arose after the U.S. passed a law that bans foreign businesses from its exchanges if their auditors haven’t been inspected by the PCAOB for three years in a row.

Erica Williams, who became the PCAOB’s chairwoman in January, in recent months has been working with other board members and staff to advance the body’s strategy.

The PCAOB in May said it would craft proposals this year on audit quality controls and auditors’ consideration of potentially illegal acts in the audit by their clients.

The watchdog last month adopted a rule strengthening the requirements for lead auditors in supervising other auditors outside their firms, the first standard to pass under Ms. Williams.

The SEC in November appointed four new board members to the PCAOB, including Ms. Williams, after firing the former chairman, William Duhnke, and moving to replace the board in June 2021.

“While they have their work cut out for them, I believe that Chair Erica Williams and the Board can live up to Congress’s original vision with respect to standard-setting,” Mr. Gensler said.

Mr. Gensler has previously said the PCAOB wasn’t living up to its role as a setter and enforcer of auditing standards.

Ms. Williams and the board have laid out an aggressive standard-setting agenda and she welcomes Mr. Gensler’s support as they work to modernize and strengthen its standards, a PCAOB spokesperson said.

Mr. Gensler said in Wednesday’s speech that U.S. audit quality has improved since 2002 but noted that certain areas, such as auditor independence, are still lacking.

Mr. Gensler said he has asked the PCAOB to look into updating audit independence standards and said the SEC might need to take a fresh look at its own auditor independence rules.

The U.S. securities regulator in 2020 gave auditors more discretion in assessing conflicts of interest in their relationships with businesses they audit. The PCAOB’s rules are currently aligned with those of the SEC.

Mr. Gensler also urged audit firms to review and enhance their independence protocols with respect to their auditing and consulting practices. “Given the growth in the size and complexity of nonaudit services, it is important that audit firms maintain a culture of ethics and integrity—placing the highest priority on auditor independence throughout the firm, not just in the audit practice,” he said.

Ernst & Young is considering a breakup of its business into separate audit and consulting businesses that will provide audit and advisory services to clients.

Updated: 2-17-2023

Lack of Crypto Audit Regulation Raises Questions About PCAOB Authority

Watchdog says it lacks jurisdiction on audits of private companies, but some accountants and academics say there are ways to strengthen its crypto oversight.

The Public Company Accounting Oversight Board is facing calls to be the regulator that brings supervision to bear on auditors of cryptocurrency companies, even as the majority of crypto businesses fall outside its jurisdiction.

Cryptocurrencies in the U.S. are largely unregulated, leaving investors at risk of market manipulation and fraud, and most crypto exchanges are privately held, so they aren’t required to produce audited financial statements or file the reports with the Securities and Exchange Commission.

Additionally, there isn’t a regulatory framework for audits for many crypto companies.

The SEC, which oversees the PCAOB, is reviewing how crypto companies portray reports from audit firms in the aftermath of the FTX collapse. The regulator is especially concerned about so-called proof-of-reserves reports, which aim to show sufficient assets to cover customer funds.

“It is the Wild West in the sense that nobody is requiring audits of financial statements and no one is specifying the standards that ought to apply to proof-of-reserves reports,” said Douglas Carmichael, a Baruch College accounting professor and former PCAOB chief auditor.

“It’s a big concern when investors get a report from an audit firm that seems to provide assurance when it doesn’t.”

Privately held crypto exchanges such as Binance Holdings Ltd., Kraken and Crypto.com, have moved to bolster efforts around these reports, which fall short of full audits.

Additionally, different FTX units secured full audits from auditors Armanino LLP and Prager Metis CPAs LLC before the crypto exchange’s implosion, in contrast with other privately held exchanges.

The PCAOB lists inspection reports on registered audit firms, including Prager Metis and Armanino, on its website.

The PCAOB—which sets audit standards, inspects audits and disciplines audit firms—has said it can only oversee audits of public companies and SEC-registered broker-dealers. The watchdog in 2019, however, set up a team of inspectors who focus on emerging audit risks, including in the cryptocurrency field.

“The PCAOB prioritizes cryptocurrency-related inspections and is committed to vigorously enforcing our standards wherever they apply, including registered broker-dealers,” spokesman Kent Bonham said.

Those efforts aren’t enough for Sens. Ron Wyden (D., Ore.) and Elizabeth Warren (D., Mass.). In a letter last month to PCAOB Chair Erica Williams, they said the watchdog ignored what they called questionable practices by auditors of crypto companies.

The lawmakers cited PCAOB rules requiring registered accounting firms to meet the regulator’s standards when preparing any audit, even if an audited firm falls outside the watchdog’s jurisdiction.

Their view ignores the PCAOB’s statutory authority and hasn’t been applied by the regulator, said Coy Garrison, a former counsel to SEC Commissioner Hester Peirce who now is a partner at law firm Steptoe & Johnson LLP focusing on crypto regulation.

A Senate aide countered that the PCAOB “has a responsibility to ensure PCAOB-registered auditors treat crypto companies with the same scrutiny other companies face, or they’ll lose their credibility.”

Accountants and academics say there might be ways to strengthen the PCAOB’s crypto oversight.

Some accountants say it is accurate to classify centralized crypto exchanges as broker-dealers and the SEC could designate them as such so their audits would fall under the PCAOB’s oversight.

That would require the SEC to classify crypto assets as securities through a rule-making process, Mr. Garrison said.

SEC Chair Gary Gensler has said most crypto tokens are securities falling under his agency’s jurisdiction and should comply with investor-protection laws. But many crypto firms are broker-dealers that haven’t registered with the SEC, he has said.

Mr. Gensler has also said it is possible some crypto intermediaries would need to register with the SEC and the Commodity Futures Trading Commission, similar to some mutual funds and brokers. The SEC declined to comment.

The PCAOB’s Mr. Bonham said authority to register broker-dealers lies with the SEC.

“The PCAOB welcomes Chair Gensler’s comments and stands ready to inspect any newly registered broker-dealers as part of our overall efforts to prioritize cryptocurrency oversight,” he said.

The PCAOB in 2011 launched an interim program to inspect audits of broker-dealers after the Dodd-Frank Act expanded its mandate. Mr. Bonham said the program, while still interim, is working well and is an important part of PCAOB inspections.

The deficiencies of broker-dealer audits remained “unacceptably high,” according to an annual PCAOB report released last August.

The audit regulator’s powers could be expanded if Congress moves to amend the Sarbanes-Oxley Act of 2002 that created the watchdog, potentially allowing PCAOB-registered audit firms to apply PCAOB standards to audits of nonpublic companies, accounting professors said.

That is a good idea in principle, but Congress might not further expand the PCAOB’s authority, and the regulator likely doesn’t have the resources to tackle a related surge in workload, said Vivian Fang, professor of accounting at the University of Minnesota and chief adviser of tax, accounting and policy at crypto software firm Ledgible Inc.

The PCAOB is funded by public companies and broker-dealers, and it would gain fees from private companies under an expansion, but “I’m not sure that is a challenge the PCAOB is ready to take on right now,” she said.

Even potential improvements to crypto audit regulation might not prevent fraud in the crypto industry, said Andrew Kitto, an assistant professor of accounting at the University of Massachusetts Amherst and a former PCAOB economic research fellow.

“If you have auditors that are subject to more stringent auditing oversight, you still have a lot of incentives for individuals to try and evade their auditors,” he said.

Updated: 2-21-2023

China Urges State Firms To Drop Big Four Auditors On Data Risk

* SOEs Encouraged To Use Local Auditors When Contracts Expire

* Guidance Reiterated Even After China Reached Us Audit Deal

Chinese authorities have urged state-owned firms to phase out using the four biggest international accounting firms, signaling continued concerns about data security even after Beijing reached a landmark deal to allow US audit inspections on hundreds of Chinese firms listed in New York.

China’s Ministry of Finance is among government entities that gave the so-called window guidance to some state-owned enterprises as recently as last month, urging them to let contracts with the Big Four auditing firms expire, according to people familiar with the matter.

While offshore subsidiaries can still use US auditors, the parent firms were urged to hire local Chinese or Hong Kong accountants when contracts come up, one of the people said, asking not to be identified discussing private information.

China is seeking to rein in the influence of the US-linked global audit firms and ensure the nation’s data security, as well as to bolster the local accounting industry, the people said.

Beijing has been giving the same suggestion to state-backed firms for years, but recently re-emphasized that companies should use other auditors than the Big Four, the people added. No deadline has been set for the changes and replacements may happen gradually as contracts expire.

While the China-US audit deal last year was hailed as a sign that the competitive superpowers can still work together on some issues, Beijing’s audit guidance is a reminder that decoupling is still proceeding in sensitive areas like SOEs and advanced technology.

One risk for China is that shifting to lesser-known auditors will make it harder for SOEs to attract capital from international investors.

“It builds in a further hurdle for Chinese SOEs in terms of appealing to international capital,” said Richard Harris, chief executive officer of Hong Kong-based investment business consultancy and fund manager Port Shelter Investment Management.

“I’m not sure if the data held secret as a result is likely to be important enough to justify inhibiting that access to international capital as accountants have a legal obligation to be confidential.”

China’s finance ministry and representatives of the Chinese offices of PricewaterhouseCoopers LLP, Ernst & Young, KPMG and Deloitte & Touche LLP — collectively known as the Big Four auditing firms — didn’t respond to requests seeking comment.

As for the global arms, PwC, KPMG and Ernst & Young declined to comment, and Deloitte didn’t immediately respond to a request for comment.

The frosty relationship between China and the US shows no signs of abating, with the episode over an alleged Chinese spy balloon adding further tension.

But the audit breakthrough last year was seen as a positive sign, ending decades-long spat that threatened to kick more than 200 Chinese firms off the American exchanges.

The US Securities and Exchange Commission on Wednesday declined to comment on Chinese authorities’ move on accounting firms. Generally, SEC rules don’t require companies to work with one of the Big Four accounting firms.

But companies must use accounting firms registered with the US Public Company Accounting Oversight Board, an auditor watchdog agency overseen by the SEC.

Companies traded on US exchanges risk being delisted if the PCAOB isn’t able to fully inspect and investigate the work papers of their auditors after three years in a row.

“The PCAOB continues to demand complete access to inspect and investigate all registered firms in China, and there will be no loopholes and no exceptions whether those firms are part of a global network or not,” Erica Williams, the board’s chair, said in a statement Wednesday.

“Should PRC authorities obstruct or otherwise fail to facilitate the PCAOB’s complete access at any point, in any way, the board will act immediately.”

The PCAOB in December completed its first-ever on-site work paper inspection of some of the largest Chinese companies and said it was able to sufficiently review audit documents during the trip to Hong Kong, which was hosted by PwC and KPMG. The PCAOB is planning further reviews this year.

Several big state firms including China Eastern Airlines Corp., China Life Insurance Co. and Petrochina Co. have voluntarily applied to delist from the American exchanges.

Voluntary delisting, however, doesn’t protect issuers’ “audit engagements from being selected for PCAOB inspections or investigations,” a PCAOB spokesperson said.

“PCAOB inspections of firms are retrospective. So if a company delists in a given year, PCAOB may still inspect audits from previous years while it was listed or investigate the audit work.”

Winners And Losers

Getting shut out of Chinese state-owned business would be a blow to the accounting firms. The Big Four earned combined revenue of 20.6 billion yuan ($3 billion) from all Chinese clients in 2021, according to the finance ministry.

Some 60 Hong Kong-listed companies with Chinese headquarters — state-owned and private — have changed auditors since September last year, when the PCAOB started its historic review.

Smaller Chinese and Hong Kong firms gained almost 20 jobs from the Big Four, according to Hong Kong exchange filings.

Those changing to smaller audit firms in recent months include property developer Sino-Ocean Group Holding Ltd. and its subsidiary Sino-Ocean Service Holding Ltd., which dropped PwC, citing good governance practices to rotate auditors after long years of service.

Furniture maker Red Star Macalline Group Corp. proposed to end a contract with EY because they “failed to reach consensus on the work schedule and expenses.”

While the Big Four dominate China at the moment, smaller rivals are edging up. Potential winners of new business could include close rivals such as Pan-China Certified Public Accountants, BDO China Shu Lun Pan CPAs, Moore Global, and RSM China.

More than 80 listed companies in Shanghai and Shenzhen also changed auditors since December, Chinese news outlet Jiemian reported. Chinese regulators have expressed concerns over some smaller firms’ quality of work and ability to handle troubled listed clients.

“The Big Four have grown because of their perceived independence and size, and being global and subject to different regulators reinforces this perception of trust, on which the Western financial system depends,” Harris said.

“While smaller firms should adopt the same internal controls and external regulation, they have to try much harder to justify that trust that it has taken the big names decades to build.”

Updated: 3-13-2023

KPMG Faces Scrutiny For Audits of SVB and Signature Bank

Accounting firm blessed books of two banks weeks before failure.

Silicon Valley Bank failed just 14 days after KPMG LLP gave the lender a clean bill of health. Signature Bank went down 11 days after the accounting firm signed off on its audit.

What KPMG knew about the two banks’ financial situation and what it missed will likely be the subject of regulatory scrutiny and lawsuits.

KPMG signed the audit report for Silicon Valley Bank’s parent, SVB Financial Group, on Feb. 24. Regulators seized the bank on March 10 after a surge of withdrawals threatened to leave it short of cash.

“Common sense tells you that an auditor issuing a clean report, a clean bill of health, on the 16th-largest bank in the United States that within two weeks fails without any warning, is trouble for the auditor,” said Lynn Turner, who was chief accountant of the Securities and Exchange Commission from 1998 to 2001.

Two crucial facts for determining whether KPMG missed the banks’ problems are when the bank runs began in earnest and when the bank’s management and KPMG’s auditors became aware of the crisis.

What is known about Silicon Valley Bank is that deposit outflows accelerated last month. In its March 8 statement, Silicon Valley Bank said “client cash burn has remained elevated and increased further in February.”

The bank said its deposits at the end of February were lower than it had predicted in January.

Both bank audits were for 2022, so auditors weren’t scrubbing the banks’ books when they ran into trouble. But auditors are supposed to highlight risks faced by the companies they audit.

They are also supposed to raise important issues that occur after companies close their books and before the audit is completed.

A spokesman for KPMG declined to comment on the specific audits, due to client confidentiality. In a statement, the firm said it isn’t responsible for things that happen after an audit is completed.

Silicon Valley Bank’s deposits peaked at the end of the first quarter of 2022 and fell $25 billion, or 13%, during the final nine months of the year. That means deposits were declining during the period of KPMG’s audit.

If the decline was affecting the bank’s liquidity when KPMG signed off on the audit report, that information likely should have been included. Since it wasn’t, the question becomes, did KPMG know or should have known what was going on?

Auditors are supposed to warn investors if companies are in trouble. They are required to evaluate “whether there is substantial doubt about the entity’s ability to continue as a going concern” for the next 12 months after the financial statements are issued.

Auditors also use their reports to highlight “critical audit matters” that involve challenging, subjective or complex judgments. KPMG in that section of its report focused on the accounting for credit losses at Silicon Valley Bank.

But it didn’t address Silicon Valley Bank’s ability to continue holding debt securities to maturity—which, in the end, the bank lacked.

Even if the bank wasn’t struggling last year, KPMG was required to evaluate developments that occurred after the balance-sheet date so the company’s financials were presented fairly.

Signature Bank, which was seized by regulators on Sunday, also faced a run last week but it didn’t have the same balance-sheet issues as Silicon Valley Bank. KPMG signed off on its audit on March 1.

Signature’s bet on crypto assets led to a surge in deposits, which went into reverse as that market struggled. A large amount of its deposits were uninsured, making it more likely the customers would flee at any sign of trouble.

But it hadn’t suffered the same losses on its investments as Silicon Valley Bank, giving it a greater ability to pay depositors.

The auditing firm could face additional scrutiny. KPMG also audited First Republic Bank, whose shares were down 76% Monday morning, even after the bank got a liquidity boost from JPMorgan Chase and the Federal Reserve.

KPMG’s audit work likely will be scrutinized by regulators, including the Public Company Accounting Oversight Board and the SEC, as well private litigants that lost money when Silicon Valley Bank collapsed, said Erik Gordon, a professor at the University of Michigan’s Ross School of Business.

A shareholder lawsuit against the firm concerning its Silicon Valley Bank audit “won’t be an easy one for people to win, even though the timing is spectacularly embarrassing for KPMG,” Mr. Gordon said.

A PCAOB spokeswoman said the regulator “cannot comment on ongoing inspection or enforcement matters.” An SEC spokesman declined to comment on the Silicon Valley Bank audit.

One argument KPMG could try in court is that the run on the bank started after the firm signed its audit report. A state banking regulator, the California Department of Financial Protection and Innovation, in a filing Friday said the bank was “in sound financial condition prior to March 9,” when depositors withdrew $42 billion.

Douglas Carmichael, the PCAOB’s chief auditor from 2003 to 2006, said it was unclear how the California regulator could have determined the bank’s financial condition. “It seems like a premature analysis. How could they know without examining?” he said.

“Auditors are always under the microscope when the company fails shortly after the issuance of a clean opinion,” Mr. Carmichael said. “The shorter the period the greater the concern would have to be.”

Silicon Valley Bank almost doubled its assets and deposits during 2021. It got in trouble because it bought long-term, low-yielding bonds with short-term funding from depositors that was repayable upon demand.

Accounting rules said it didn’t have to recognize losses on the assets as long as it didn’t sell them.

When rising interest rates caused the bonds’ value to drop, it got stuck in them, and they kept falling. Silicon Valley Bank still had to maintain enough liquidity to pay withdrawals, which became increasingly difficult.

The $1.8 billion investment loss Silicon Valley Bank disclosed last week stemmed from Silicon Valley Bank’s decision to sell all its “available for sale” securities during the first quarter.

Silicon Valley Bank didn’t say when it started or when it completed the sales. It isn’t clear if Silicon Valley Bank used the proceeds of those sales to help cover withdrawals.

In the March 8 disclosure, Silicon Valley Bank said it expected to reinvest proceeds from the sales. But money is fungible, and it is unclear if selling the available-for-sale securities may have freed up other sources of cash to help pay departing customers.

Most of the capital hole in Silicon Valley Bank’s balance sheet was in government-sponsored mortgage bonds that Silicon Valley Bank classified as “held to maturity.”

That label allowed Silicon Valley Bank to exclude unrealized losses on those holdings from its earnings, equity and regulatory capital.

In a footnote, Silicon Valley Bank said the fair-market value of its held-to-maturity securities was $76.2 billion as of Dec. 31, or $15.1 billion below their balance-sheet value.

The fair-value gap was almost as large as Silicon Valley Bank’s $16.3 billion of total equity—which, KPMG could point out, is something anyone reading the financial statements could have seen.

Silicon Valley Bank stuck to its position that it intended—and had the ability—to hold those bonds to maturity. KPMG allowed the accounting treatment. Now it will be up to the Federal Deposit Insurance Corp. to sell the securities.

The bank’s troubles put KPMG in a no-win situation. If it had called attention to Silicon Valley Bank’s falling deposits, or issued a warning about Silicon Valley Bank’s ability to continue as a going concern, it could have set off a run on the bank.

By not raising these issues, it will face questions about how it missed the signs that the bank was headed for trouble.

One of the agencies likely to ask pointed questions of KPMG is the FDIC. After a bank fails, the FDIC’s Office of Inspector General regularly conducts investigations and publishes detailed reports called failed-bank reviews that identify the causes of the collapse and the parties most responsible.

Such reports are studied carefully by private litigants eyeing defendants to sue for damages. On that front KPMG caught a break over the weekend: The government said it would backstop all of both banks’ uninsured depositors, in effect helping to bail out KPMG as well. The backstop won’t affect losses suffered by the banks’ investors.

Updated: 3-20-2023

Banks, Investors Revive Push For Changes To Securities Accounting After SVB Collapse

The Financial Accounting Standards Board after the financial crisis weighed fair-value requirements for financial institutions that planned to never sell their debt securities, but reversed course amid widespread industry objections.

Some bank executives and investors are reviving calls for changes to U.S. accounting rules around held-to-maturity securities in the wake of the collapse of Silicon Valley Bank, a move that was considered after the financial crisis but largely abandoned after hundreds of banking-industry objections.

If banks designate bonds as held-to-maturity securities, the firms are allowed to exclude unrealized losses on them from equity as long as they don’t sell. Banks have to carry HTM instruments at amortized cost, or an adjusted version of the original price they paid.

Bonds the banks plan to sell need to be classified as available-for-sale securities and accounted for at fair market value. If banks sell any HTM securities, they must reclassify all of their HTM securities as available for sale and potentially take a big loss on the securities they didn’t sell.

SVB had designated 43% of its total assets as HTM securities, which fell in value and led to a buildup in unrealized losses as interest rates rose last year at one of the fastest paces in U.S. history.

Selling those HTM-branded assets—mostly government-backed mortgage bonds—before maturity would have reduced capital to virtually nothing.

But as the bank struggled to maintain its liquidity to fund withdrawals, SVB was able to avoid recognizing the losses by not switching the classification, a position permitted by its auditor, KPMG.

The collapse of SVB, the largest bank to fail since the 2008 financial crisis, recalls accounting issues that plagued that period.

The Financial Accounting Standards Board, which sets accounting rules for U.S. companies, in 2010 proposed requiring banks to record all financial instruments at fair value, or marked to market, a move to provide investors with more information in the fallout of the financial crisis.

Much of the crisis stemmed from illiquid, toxic subprime assets that had to be marked to market. The issue previously came under debate in the early 1990s, in the aftermath of the savings-and-loan crisis.

“Every time there’s stress, the issue comes up,” said Robert Herz, who served as the FASB’s chair when it issued the 2010 proposal.

“If the FASB were to decide to address the issue, it will likely be very controversial and the same arguments on either side will likely be raised again,” said Mr. Herz, who is chairman of Morgan Stanley and Fannie Mae’s audit committees.

Mr. Herz declined to comment on whether the FASB should change accounting rules now.

The FASB doesn’t have a project on its standard-setting agenda related to held-to-maturity accounting. But a FASB spokeswoman said, “as part of our continuing efforts to improve accounting and financial reporting, we’re always open to engaging with our stakeholders on accounting issues.”

Banks vehemently opposed the 2010 plan, saying it would have hurt lending and inaccurately portrayed their business strategies. Opponents of the proposal far outweighed its supporters, who said it would have improved transparency and revealed potential bank weaknesses.

The CFA Institute, which represents investment professionals designated as chartered financial analysts, public pension fund California Public Employees’ Retirement System and the World Bank were among those that backed fair value as the best measure for financial instruments.

The FASB in 2011 scrapped its plan and decided to largely stick with its existing so-called mixed-measurement model, which allows for financial instruments to be treated in a mix of ways.

Financial institutions are permitted to classify debt securities based on management’s intent, business model and their ability to hold them until maturity if the assets’ value were to drop.

More than a decade later, the banking industry’s views are largely unchanged, with industry experts saying that the use of fair-value accounting for all financial instruments with a requirement to reflect the changes each period through the income statement doesn’t reflect the banking business.

The existing rules are sufficient, said Charles Levingston, chief financial officer at Bethesda, Md.-based Eagle Bancorp Inc.

“I’m OK with the designations as they sit today, but I would not be surprised to see additional conversation about this particularly given the nature with which SVB managed its balance sheet,” Mr. Levingston said.

Some bank executives, however, want the FASB to revisit the issue.

Brent Beardall, chief executive of Seattle-based bank Washington Federal Inc., criticized the current mixed-measurement model, saying it allows investors to receive only partial information.

He said the FASB should consider requiring financial institutions to present two balance sheets, one at amortized cost and one at fair value, so that the information is comparable across all classes of assets and liabilities.

“Fair value is a useful piece of information, but it’s only useful if you get all of the information. Picking and choosing is a disaster,” Mr. Beardall said. “I think it’s time that the FASB look at it and provide information to investors the way they want it.”

Timothy Spence, chief executive of Cincinnati-based Fifth Third Bancorp, said in a recent television interview the accounting designations in the differences in the available-for-sale or held-to-maturity treatment need to be addressed.

“There’s no question that what triggered the outflows at Silicon Valley Bank last week was the surprise on the unrealized losses on their securities portfolio because such a significant share of it was embedded in held-to-maturity securities,” Mr. Spence said on CNBC March 13. Fifth Third declined to comment for this article.

Meanwhile, some investors continue to push for accounting requirements they say reflect economic reality. SVB’s billions of dollars in unrealized losses tied to HTM securities would have been clearer to investors if the bank had been obligated to record them at fair value, said Sandy Peters, head of financial reporting policy at the CFA Institute.

Carrying HTM securities at amortized cost can make a bank look good “while the market value of the assets on the balance sheet implodes,” she wrote in a recent report. “SVB would have had virtually no book value if they had marked them to market, but nobody was paying attention,” Ms. Peters said.

The Council of Institutional Investors, which represents pension funds and other large money managers, has long believed that fair-value accounting with robust disclosures provides investors with more useful information than amounts that would be reported under amortized cost or other existing alternative accounting approaches, said Jeff Mahoney, CII’s general counsel.

But it doesn’t oppose existing accounting standards providing for the categorization of held-to-maturity securities, he said.

Updated: 3-22-2023

US lawmakers Reiterate Concerns About ‘Sham’ Crypto Firm Audits To PCAOB

Two U.S. senators cited the collapse of FTX when writing to Public Company Accounting Oversight Board chair Erica Williams in January, but now suggest improper auditing could have affected three banks as well.

United States Senators Elizabeth Warren and Ron Wyden have cited the recent collapse of three major banks to call on the Public Company Accounting Oversight Board (PCAOB) to “rein in” audits of crypto firms.

In a March 21 letter to PCAOB chair Erica Williams, Warren and Wyden reiterated the concerns over “shady audits” of crypto companies that the pair raised in January, this time referencing the failures of Silvergate Bank, Silicon Valley Bank and Signature Bank.

The two senators requested Williams respond to questions on whether improper audits and proof-of-reserve reports “may have played a direct or indirect role” in the collapse of the banks.

“You have ample authority to establish standards for auditors that require any SEC-registered auditor to only conduct audits of crypto firms that comply with existing standards for audit quality,” said the letter.

“Based on the obvious threats to investors and the public interest posed by sham audits, any audits and reviews of crypto firms done by SEC-registered auditors must maintain a high level of scrutiny. Otherwise, these sham audits must be addressed by PCAOB.”

Congress and the Fed weakened stress tests and other rules to prevent big banks from taking on too much risk and crashing the economy — all so banks could make bigger profits. Banks can’t be trusted to regulate themselves. Congress and our regulators need to step up. https://t.co/AVcFr7g3GB

— Elizabeth Warren (@SenWarren) March 21, 2023

Warren and Wyden suggested that defunct crypto exchange FTX, currently in bankruptcy court for Chapter 11 proceedings, could have impacted the events around Silvergate and Signature, given the firm “received sham financial reviews” by auditors registered with the PCAOB, writing:

“In assessing the risks associated with the FTX’s deposits, as well as those of other crypto-related customers, the banks may have relied on the misleading and faulty financial information provided by proof-of-reserve examinations.”

The two senators requested Williams provide a staff-level briefing on March 31 and respond to the questions raised by April 4.

Warren, an outspoken critic of many aspects of the digital asset space, has been pointing to a lack of regulatory oversight as part of the reason behind the failure of the aforementioned banks.

On March 15, she requested that Federal Reserve Chair Jerome Powell recuse himself from any review of regulatory failures leading to the collapse of Silicon Valley Bank.

PwC Probes Security Incident Tied To Russian-Speaking Clop Cyber Gang

* Accounting Firm Says Event Had ‘Limited Impact’ On Business

* MOVEit Software Flaw Haunts Businesses, Us Government Agencies

A criminal hacking gang has added more names to its lists of alleged victims from a recent campaign that exploited a vulnerability in a popular file-transfer product.

The group, known as Clop, threatened to post internal data from professional services firms Pricewaterhousecoopers LLP and Ernst & Young LLP unless they pay a ransom fee. The scope of the incidents weren’t immediately clear.

The Russian-speaking gang has in recent weeks launched scores of attacks after discovering a vulnerability in MOVEit, a file-sharing software from Progress Software Corp.

Pricewaterhousecoopers in a statement confirmed it used MOVEit software, and that the hack had a “limited impact” on PwC. The firm stopped using the MOVEit platform upon learning of the incident, it said.

“We have reached out to the small number of clients whose files were impacted to discuss the incident,” a company spokesperson said. “Data security is a key priority for PwC and we continue to put the right resources and safeguards in place to protect our network.”

Ernst & Young has previously said it had launched an investigation into its use of the MOVEit tool and “took urgent steps to safeguard any data.”

“We have verified that the vast majority of systems which use this transfer service across our global organization are secure and were not compromised,” the spokesperson said in a statement from June 16.

“We are manually and thoroughly investigating systems where data may have been accessed. Our priority is to first communicate to those impacted, as well as the relevant authorities. Our investigation is ongoing.”

The largest US public pension fund, the California Public Employees’ Retirement System, or CalPERS, also said the personal data of about 769,000 members — including Social Security numbers, dates of birth and potentially the names of family members — have been exposed due to the same MOVEit issue.

CalPERS said a third-party vendor that CalPERS used to help make payments to retirees and other beneficiaries notified the company on June 6 that a MOVEit vulnerability allowed data to be downloaded by an unauthorized party.

“This external breach of information is inexcusable,” said CalPERS Chief Executive Officer Marcie Frost in a statement. “Our members deserve better.”

The US Cybersecurity and Infrastructure Security Agency on June 1 issued an advisory about a vulnerability in MOVEit software, warning that “a cyber threat actor could exploit this vulnerability to take over an affected system.”

Progress has since released a patch to fix the vulnerability, but about 90 companies are so far known to have been affected by the hack, according to cybersecurity researchers.

Last week, Shell Plc said it was investigating a possible data breach after it was targeted by Clop. The gang listed Shell among dozens of other victims including a US university, insurance and manufacturing firms, as well as banks, investment and financial services companies.

US government agencies have also been affected.

Clop has been among the most prolific cybercriminal gangs in recent years, causing hundreds of millions of dollars of damage internationally, according the cybersecurity firm Trend Micro Inc.

In a statement posted on its dark web page last week, Clop invited victims to reach out and negotiate. “We have information on hundreds of companies so our discussion will work very simple,” the gang said, claiming it had downloaded “a lot of your data as part of exceptional exploit.”

Updated: 3-23-2023

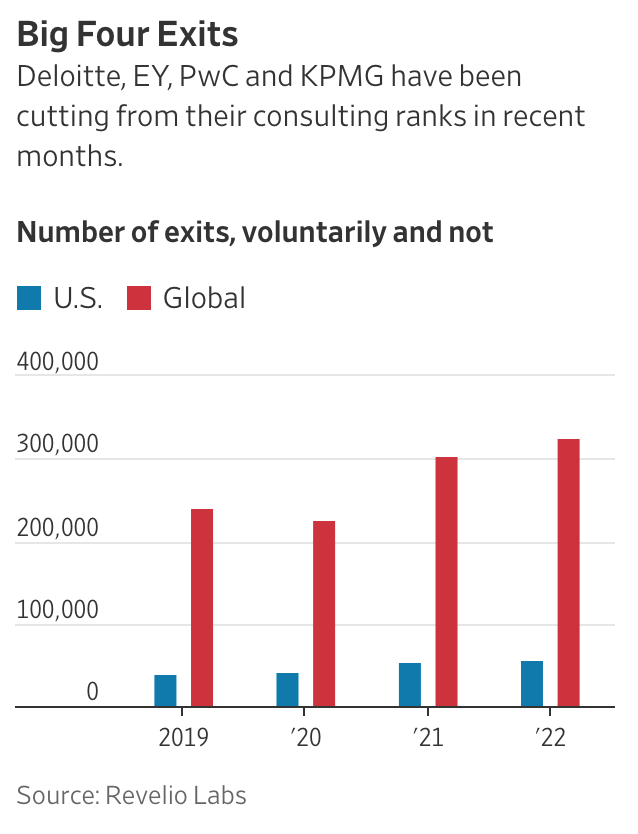

McKinsey Starts Cutting 1,400 Jobs This Week in Restructuring

* It’s One Of The Biggest Rounds Of Cuts At The Consulting Giant

* Firm Aims For Attrition Or Voluntary Exits For More Reductions

McKinsey & Co. is embarking on a rare round of major job cuts, with plans to eliminate about 1,400 roles.

The consulting giant, which has seen rapid growth in its headcount over the past decade, is restructuring how it organizes its support teams starting this week, including workforce reductions or moving people into other roles.

The total cuts will amount to about 3% of headcount that has ballooned to almost 47,000 from 28,000 just five years ago and 17,000 in 2012.

Consulting giant McKinsey is embarking on a rare round of major job cuts with plans to eliminate about 1,400 roles.@EdLudlow has more https://t.co/am9iDnxtYF pic.twitter.com/cOztmByRrO

— Bloomberg TV (@BloombergTV) March 28, 2023

“The painful result of this shift is that we will have to say goodbye to some of our firm functions colleagues, while helping others move into new roles that better align to our firm’s strategy and priorities,” Bob Sternfels, global managing partner, wrote in a note to staff.

“Starting now, where local regulations allow, we will begin to notify colleagues who will depart our firm or be asked to change roles.”

The total number of cuts were described by a person with knowledge of the matter, who asked not to be identified because the information isn’t public. A spokesperson declined to comment.

Unlike some of the major financial firms it works with, McKinsey rarely carries out job cuts in its own ranks. Even underperforming employees in client-facing roles tend to depart after being “counseled to leave” — a phrase that indicates the company doesn’t want them on client projects and recommends they try to find a different employer.

The company, where it can, is “implementing reductions through attrition or voluntary departures,” Sternfels wrote.

The firm — known for devising workforce-reduction plans for its clients — had been looking at eliminating about 2,000 jobs, people familiar with the plans told Bloomberg News last month, adding that the number of people to be cut from the firm could still change. Most of the affected roles don’t have direct contact with clients.

McKinsey posted a record $15 billion in revenue in 2021, and surpassed that figure in 2022, a person familiar with the matter said last month.

Consulting firm Accenture Plc said last week it will cut 19,000 jobs — about 2.5% of its workforce — over the next 18 months, one of the largest rounds of dismissals in the sector.

Companies in industries from finance and technology to retailing are reducing staff amid a slowdown in demand and predictions of a looming recession.

Tech giants including Amazon.com Inc. and Microsoft Corp. are making deep cuts, and Goldman Sachs Group Inc., Morgan Stanley and other top banks have been eliminating thousands of positions. Facebook parent Meta Platforms Inc. has undertaken two rounds of mass layoffs.

McKinsey’s move comes two years after Sternfels took over as global managing partner following a vote by its roughly 650 senior partners to oust his predecessor, Kevin Sneader.

The management shift was the culmination of a tumultuous period for the firm, which took flak for its role in advising the makers of the painkiller OxyContin and faced scrutiny of various other business ties.

Updated: 3-28-2023

U.S. Audit Watchdog Proposes Move To Get Inspections Started Faster

The PCAOB proposed slashing the period auditors have to assemble final documents on audits to 14 days from 45. That might get material information into investors’ hands faster, the group said.

The Public Company Accounting Oversight Board proposed cutting by more than half the amount of time auditors have to assemble final audit documentation, which might allow the audit watchdog to start its inspection process up to a month earlier and provide key information to investors sooner.

The U.S. audit regulator has been working to update more than 30 standards that have gone largely unchanged since they were adopted on an interim basis roughly 20 years ago from the American Institute of Certified Public Accountants.

With the proposal released Tuesday, the PCAOB suggested consolidating and modernizing four interim standards into one standard on auditors’ core responsibilities, including areas such as professional skepticism, independence, competence and professional judgment.

As part of that update, auditors would have up to 14 days to assemble their final set of audit documentation, as opposed to the 45 days they are now granted. These documents usually help show whether the audit work complied with PCAOB standards.

Most of the documentation in this process, known as archiving, is now occurring electronically, the PCAOB said. Many firms documented at least a portion of their procedures using paper-based systems in 2004, when rules on archiving were set.

Some firms compile the documents in as little as two to four days, while others take the full 45 days.

The PCAOB can’t begin its inspection of any given registered accounting firm until its auditors have put together a final set of audit documentation, a task that has to be done as close as possible to the end of a particular audit.

The PCAOB’s inspection teams select certain completed audits conducted by a firm for review.

By shortening the window to 14 days, the PCAOB could begin its inspection process earlier than usual, putting possibly material information in the hands of investors more quickly.

“This would lead to a waterfall effect that ultimately would provide the opportunity for us to get our inspection reports to investors sooner, enhancing their protection,” PCAOB Chair Erica Williams said on Tuesday.

Ms. Williams, who took the helm of the PCAOB in January 2022, has led several other initiatives at the regulator including dialing up enforcement of rules against audit firms and individual auditors that violate them.

The proposal would also seek to clarify the role of the partner in charge of an audit, particularly when planning, supervising and documenting audit-engagement activities.

This partner needs to review sufficient documentation to make sure that the engagement was performed as planned, a requirement more explicitly laid out under the proposal.

Consolidating the standards is aimed at helping to ease auditors’ understanding and compliance, the PCAOB said.

The public will have until May 30 to weigh in on the proposal, the PCAOB said.

EY Breakup Plan’s Fate May Rest On Executive Showdown This Week

Retired U.S. partners are also fighting the deal, worried about payouts they are owed.

The fate of Ernst & Young’s proposed split may be determined in Silicon Valley this week when feuding executives meet to hash out a deal that is acceptable to all factions.

One of those powerful factions won’t be represented at the meeting and doesn’t even work for the global auditing firm. Yet some of EY’s retired partners are playing a key role in trying to block the deal.

EY this month paused its preparations for the multibillion-dollar breakup, after its U.S. arm demanded a blueprint for the deal be reworked to give auditors a bigger share of the lucrative tax practice.

The unexpected revolt, putting the deal in jeopardy, has provoked infighting and rifts within the 390,000-person firm, according to people familiar with the matter.

This week’s meeting in Palo Alto, Calif., sets the stage for a potential showdown between the breakup plan’s architect, EY’s global leader Carmine Di Sibio, and the person most likely to derail it, EY’s U.S. leader Julie Boland.

Tensions between the two senior executives have escalated sharply in recent weeks, the people familiar with the matter said.

Ms. Boland, EY’s U.S. chair and managing partner, last week said the firm still needed to resolve questions affecting the financial strength of both businesses that will be created by the split.

Mr. Di Sibio responded with a direct appeal to EY’s 13,000 partners, telling them in an email they had “the right to vote on whether to proceed with a transaction,” according to a copy of his message reviewed by The Wall Street Journal.

The power struggle between the duo reflects the unusual structure of EY and other big accounting firms. Mr. Di Sibio runs EY’s global network, but needs approval from dozens of independent firms for the breakup.

Ms. Boland, as the head of the most powerful of those member firms, effectively holds sway over some 40% of EY’s global revenues.

There is also no guarantee the warring factions of EY can agree to a compromise deal. The U.S. demands to strengthen the audit-focused firm, at the expense of the new consulting company, could affect the amount raised by the split.

That in turn could reduce the windfalls for partners, making the deal less attractive to the U.K. and other overseas EY firms that lined up behind the original blueprint.

U.S. opposition to the deal, and criticism of Mr. Di Sibio, has also come from scores of retired EY partners, including former leaders of the firm.

Retired EY partners don’t get to vote on the deal. But they are an influential contingent. Many retain connections to the firm via friends or family, such as retired partner Jim Boland, who is Ms. Boland’s father.

Some retired partners serve as executives or board members at major companies, making them valuable as clients or potential clients.

Their central concern involves money. EY has around $7 billion of promised payouts to its retired U.S. partners that aren’t backed by a specific pot of money.

Retired partners worry the audit-focused firm, weakened by the sale of the consulting arm, may not generate sufficient earnings to meet these pension-style commitments in future, according to memos reviewed by the Journal.

“We are the largest creditors of the company and want to make sure our rights are protected,” one retired U.S. partner said.

EY’s leadership has pledged to use some of the estimated $30 billion that would be raised by the deal to increase the funding for retired partners, according to people familiar with the matter.

The firm has set up a committee to represent the retired partners, and agreed to pay for lawyers and actuaries to advise them, the memos reviewed by the Journal show.

But that may not be enough to quell the retirees’s revolt, which has morphed from concerns about pension obligations to questioning the benefits of doing a deal at all.

Four former EY leaders this month said there remained “significant questions…around the necessary strength EY must have” after any spinoff, according to a copy of their joint statement seen by the Journal.

Even if EY’s leaders succeed in overcoming the current impasse, retired partners could prove a continuing roadblock to getting a deal done. One group, who are organizing opposition to the deal online via Facebook and emails, recently appointed a law firm to advise on their rights, according to a memo reviewed by the Journal.

The start of that legal work has been delayed, while work on the deal itself is paused, the memo said.

Updated: 3-31-2023

EY Fails To Reach Deal On Split

Opposition to breakup plan is being led by two longtime U.S. auditors.

The unexpected revolt that has upended the planned breakup of accounting firm Ernst & Young is being driven by two longtime U.S. auditors who believe their part of the firm could end up weakened by a deal.

John King and Frank Mahoney, senior U.S. EY executives, have emerged as key opponents to the firm’s plan for a worldwide split of its auditing and consulting arms, according to people familiar with the matter.

After a year of planning and tens of millions of dollars in costs, the split of the 390,000-person accounting firm was put on hold earlier this month. A meeting in Silicon Valley this week failed to reach a deal.

Carmine Di Sibio, EY’s global leader, and Julie Boland, head of the firm’s U.S. arm, said in a joint statement Friday they were “continuing to work toward a transaction.” The deal is “very complicated, and we agree it is critical that we get the key elements right,” the statement added.

The stalemate dates back to earlier this month. Mr. King, EY’s U.S. head of auditing, and his predecessor, Mr. Mahoney, used a meeting of EY’s U.S. leadership to push back on the planned breakup, the people familiar with the matter said.

The two executives convinced EY U.S. chief Ms. Boland that the auditors should get a greater share of EY’s multibillion-dollar tax practice, according to people familiar with the matter.

Ms. Boland would lead the global audit firm, should the split go ahead. Mr. Di Sibio is expected to lead the new consulting firm.

As U.S. leader, Ms. Boland could have forced through the blueprint with the support of two-thirds of the U.S. executive committee, the people familiar with the matter said. But she was reluctant to ignore the concerns of the two senior auditor representatives and their supporters, the people added.

A group of powerful retired U.S. EY partners, including former leaders of the firm, is also fighting the split, people familiar with the matter said. They are concerned about the future of the auditing firm, which is on the hook for the firm’s pension payments.

An official committee representing U.S. retired partners has had discussions with Ms. Boland, according to emails viewed by The Wall Street Journal.

Ms. Boland this month appeared to support the need to rethink the deal, telling the Journal that “people are asking the right questions, and we’re making sure we’re getting those questions answered.” She demanded changes to the template for the breakup.

The U.S. is the most powerful of the scores of member firms that make up EY’s global network. A deal would be extremely difficult without U.S. participation.

Mr. King and Mr. Mahoney, who now leads the firm’s U.S. West region, didn’t respond to requests for comment. A spokesman for EY’s U.S. firm said “it would be impossible for a handful of people to derail the process under the U.S. firm’s governance rules.”

The surprise upending of the carefully orchestrated deal preparations has caused disruption and infighting at the firm.

Mr. Di Sibio, EY’s global chairman and chief executive, said in a recent internal email the firm’s 13,000 partners are “overwhelmingly in favor” of doing a deal, according to a copy viewed by the Journal.

Even if that is the case, there appears little that he or any of EY’s overseas firm leaders can do to push through a global deal should the U.S. firm’s leadership remain opposed.

This week’s meeting of EY’s global executives included Mr. Di Sibio and U.S. leader Ms. Boland, but not the U.S. auditors who balked at the original proposal, according to one of the people familiar with the matter.

The mood was broadly positive, but progress was limited because the U.S. firm is still working on an alternative template for the split, the person added.

EY’s leaders are looking at getting an agreement done in the next few weeks, according to one of the people familiar with the matter. The longer the uncertainty drags on, the greater the damage to the firm, industry watchers said.

One central concern is the impact on clients. Mr. Di Sibio in his recent email to partners said media coverage of the troubled transaction had led to “a larger volume of client questions being received and discussions being held.”

Rohit Deshpande, a marketing professor at Harvard Business School, said the delays to carrying out the split risked causing confusion about what the EY brand now represents.

“Clients are getting mixed messages as to whether strategically this was a good idea or not,” Mr. Deshpande said. “Speed is absolutely of the essence.”

The uncertain fate of the deal is also affecting staff morale, according to people familiar with the matter and messages on employee websites.

“This is an unmitigated disaster,” one EY employee wrote recently on Fishbowl. Another said they have “never been more embarrassed of this firm.”

Responding to the tensions between global leader Mr. Di Sibio and U.S. chief Ms. Boland, another EY employee commented: “Will someone pull these two aside and say please stop! Neither of you are helping the situation right now.”

The turmoil at EY could make competing firms look more appealing for employees, who are not in line for the multimillion-dollar payouts promised to partners should the deal go ahead.

That risk is heightened by the current widespread shortage of accountants, according to Troy Janes, accounting professor at Purdue University and a former EY auditor.

“If your firm seems like it’s not a fun place to be anymore, there’s other firms out there who would be more than happy to hire you away because they need people,” Mr. Janes said.

Updated: 4-11-2023

Ernst & Young Halts Breakup Plan After Revolt By U.S. Leaders

EY spent more than $100 million on split between auditing, consulting business.

Ernst & Young has axed its plan for a split of its auditing and consulting arms, marking a dramatic and costly retreat from a proposal that was meant to reshape the accounting profession but ended amid bitter infighting at the firm.

Global leaders of the Big Four firm said Tuesday they were “stopping work on the project” because the heads of EY’s U.S. arm, the biggest member of the global network, had decided not to move forward, according to a note sent to EY’s 13,000 partners.

Rather than creating two dynamic firms, EY is now left with a potential leadership vacuum, thousands of angry partners, a split between its U.S. and overseas partnerships and confused clients.

EY spent more than a year and over $100 million on the effort only to see it upended by a small group of senior U.S. executives.

“This is the beginning of a real period of nastiness,” said an EY U.S. partner who favored the deal.

EY’s global leaders said in the note to partners that they remained committed to the principle of splitting the auditing and consulting businesses.

But it isn’t clear how a split could be redesigned in a way that achieves consensus, given the failure of intense negotiations over recent weeks to rescue the deal.

“We thought we had something everyone would sign up to,” one person close to the deal said. “This means going back to the drawing board.”

The failure of the project marks a humiliating rebuff for Carmine Di Sibio, EY’s global chairman and chief executive, who championed the planned split.

Mr. Di Sibio had originally been scheduled to retire in June but was granted a two-year extension to see the proposal through and was nominated to lead the newly created consulting firm.

His plans were undone by a revolt among U.S. audit leaders who complained that the consulting business was getting the bulk of the firm’s lucrative tax business.

The auditors, joined by an influential group of retired partners, were concerned that the split would leave the audit business too weak to compete.

EY now faces a potential leadership crisis at the top of the 390,000-person firm. Mr. Di Sibio and EY’s overseas leaders who supported the breakup have lost credibility for failing to deliver on it.

Staff members are angry about the uncertainty the plan created and cost cuts imposed on them to boost profitability.

Julie Boland, the chief of EY’s U.S. arm and a potential leader of the firm, may struggle to command global support. She was due to head the new audit-focused partnership, but was unable to unite her executives behind the breakup plan.

The split entailed getting approval from partners in dozens of countries and hinged on a complicated plan to raise cash to pay millions of dollars to the audit partners for giving up the consulting business.

That plan faced headwinds from rising interest rates and volatile markets. EY had planned for the consulting business to borrow billions of dollars and raise billions more from an IPO to pay auditing partners, as well as fund pensions for retired partners.

Ms. Boland and other U.S. leaders said Tuesday that they would support a breakup at the right time, but also laid out their demands for change, according to a copy of an internal note viewed by The Wall Street Journal.

The firm needs to simplify its structure, invest in its most strategic businesses and modernize its governance, the note said. “These actions will also better prepare us to execute on transaction options in the future,” it said.

EY’s effort was closely watched in the accounting industry, which has moved aggressively into consulting operations despite potential conflicts of interest. EY hoped to create a template that other leading firms would be forced to follow.

Mr. Di Sibio said in December that the firm’s “competitors are jealous in terms of what we’re doing,” according to a copy of a webcast viewed by the Journal.

Instead of creating a model for the future of the profession, EY appears instead to have proved its doubters right. Joe Ucuzoglu, the global chief executive of rival Big Four firm Deloitte, last month said history was littered with examples of proposed transactions that “sounded great [with] pretty slide decks [and] lots of big promises” that never played out as intended.

Rival firms will likely try to poach disaffected EY partners, now that multimillion-dollar bonuses promised under the split appear to have evaporated, according to people familiar with the matter.

Cost-cutting to boost profit margins in the U.S. firm, including a suspension of the midyear bonus employees hoped to receive earlier this year, has added to staff frustration, the people said.

Differences over the planned split have riven EY’s U.S. firm, which contributes some 40% of the firm’s $45 billion in annual global revenue, according to people familiar with the matter.

Most of the executive committee backed the proposed deal, the people said, but U.S. managing partner Ms. Boland refused to override the objections of a handful of senior audit leaders.

The apparent ability of a few U.S. executives to wreck a deal affecting thousands of partners, in scores of countries, frustrated the global leadership.

Mr. Di Sibio told partners this month that the “overwhelming majority” backed the deal and that they had the right to vote on whether to go ahead.

The U.S. leaders in their note also focused on the growing financial challenges to the deal. Tougher economic and market conditions mean the “transaction economics have become challenged,” the leaders added, according to their note.

Mr. Di Sibio launched the plan, known as Project Everest, to address a longstanding limitation on the growth of the firm’s consulting business. Many countries prevent firms from doing consulting work for companies they audit.

That limited the pool of prospective consulting clients and companies the consulting firm could work with. This was a big issue for EY, which audits most of the large tech companies, meaning they couldn’t join with them on tech consulting contracts.

“The fact that this deal, as constructed, now seems unlikely to go ahead, doesn’t mean that the thinking that underpinned it was wrong,” said Fiona Czerniawska, chief executive of research firm Source.

“Clients are still looking for different delivery models, and EY’s specific constraint—the extent to which the firm can partner with big technology firms—remains just as urgent an issue to resolve.”

The breakup plan created uncertainty among the thousands of new graduates that EY needs to recruit every year. Jeffrey Johanns, accounting professor at the University of Texas at Austin, said some of his students graduating with master’s degrees in accounting and job offers from EY have been concerned about the implications of the split and its related turmoil.

The students hadn’t received start dates at EY, unlike their peers at the other Big Four firms, he said.

Updated: 5-7-2023

Deloitte Integrates Blockchain For Digital Credentials

The credentials will “have multiple use cases,” including regulatory compliance for banking and decentralized finance, age verification for e-commerce, private logins and fundraising.

Big Four accounting firm Deloitte has integrated blockchain technology to allow customers to store verification credentials in a single digital wallet to streamline the “typically inefficient” verification processes.

In a May 4 statement, Deloitte announced it has integrated KILT Protocol technology — a Polkadot parachain — to enable the issuance of reusable digital credentials to its customers.

The integration aims to improve the efficiency of Deloitte’s Know Your Customer (KYC) and Know Your Business (KYB) verification processes.

In the statement, Deloitte said the standard and “typically inefficient” processes, including KYC and KYB certificates being issued on paper, and identity verification requests requiring multiple data points when only one is needed, often create “extra work in the process.“

Additionally, these traditional verification procedures store data and personal information across multiple platforms and databases, placing consumer data privacy at risk.

Establish a digital identity with Deloitte and keep control of your data, sharing only the data you want to share. We are launching a credential verifier, in partnership with @Kiltprotocol and @Polkadot. Applications opening soon. #KYC #Blockchain #Web3

https://t.co/NDkUf9XMqk— Deloitte Switzerland (@DeloitteCH) May 4, 2023

The credentials will serve various use cases, including regulatory compliance for banking and decentralized finance (DeFi), age verification for e-commerce, private logins and fundraising.

While the wallet will be stored on the customer’s device and remain under their control at all times, Deloitte retains the ability to modify if circumstances change, as noted in the statement:

“Credentials are digitally signed by Deloitte. Deloitte can revoke credentials using blockchain technology if conditions of the customer have changed after the credential was issued.”

The company added that no prior knowledge of blockchain is required from customers to set up the credential wallet.

KILT Protocol founder Ingo Rübe said that the streamlined identity solutions built on KILT allow customers to use verifiable digital credentials across multiple services while maintaining control “over when and where to share personal information.”

As a Polkadot parachain, it also provides the “scale and security needed by enterprise partners,” he added.

Polkadot tweeted shortly after the announcement on May 4, saying that Deloitte leveraging KILT’s solutions to support its KYC and KYB processes is vital for safeguarding itself against illegal activity.

2/ Deloitte will leverage KILT’s reusable digital identity credentials to support its Know Your Customer / Know Your Business processes (KYC/KYB) – vital for protecting financial institutions against fraud, corruption, money laundering and terrorist financing.

— Polkadot (@Polkadot) May 4, 2023

This comes after reports on April 26 that there were over 300 crypto-related job opportunities available at Deloitte, with almost all of them being posted in the same week.

Meanwhile, searching for crypto-related job openings at the other Big Four accounting firms, Ernst & Young, KPMG and PricewaterhouseCoopers, showed no results.

Updated: 5-10-2023

Auditors Didn’t Flag Risks Building Up In Banks

Bond losses such as those at Silicon Valley Bank could have been raised as ‘critical audit matters’.

When KPMG LLP gave Silicon Valley Bank a clean bill of health just 14 days before the lender collapsed, the Big Four audit firm flagged potential losses on loans as a so-called critical audit matter.

But the audit opinion was silent on what actually brought down the bank—its unrealized bond losses and ability to hold them given a reliance on potentially flighty deposits.

“The auditors failed to mention the fire in the basement or the box of dynamite on the first floor, but they did point out the peeling paint on the flower box,” said Erik Gordon, a University of Michigan business professor. “How could they miss the interest-rate risk?”

The current banking crisis is the first big test of critical audit matters, a measure designed to help investors decode risks and uncertainties buried in financial statements.

Audit regulator Public Company Accounting Oversight Board introduced critical audit matters in 2017 to “breathe life into the audit report.” Described as the biggest shake-up in audits in 70 years, the new standard was meant to make audit opinions more useful to investors.

So far, though, critical audit matters have failed to shed light on issues that have caused a collapse of confidence among depositors and investors in many small and midsize banks.

Auditors are required to record any critical audit matters when they sign off on a public company’s books. Regulators define these as matters that have a significant impact on the financial statements and involve “especially challenging, subjective or complex” judgments by the auditors.

Silicon Valley Bank’s unrealized losses in its bond portfolio appear to “meet every definition of a possible critical audit matter,” said Martin Baumann, a former chief auditor at the PCAOB who had a leading role in designing the new measure.

The latest banking crisis has exposed the gamble some banks took in betting heavily on long-term government bonds, which last year plunged in value as the Federal Reserve raised interest rates.

Banks can keep these losses off their books by classifying their bondholdings as “held to maturity,” or intended never to be sold, allowing them to be held at cost rather than fair value.

The banking industry last year relied more heavily on this accounting maneuver, as rising rates pummeled balance sheets.

Accounting rules say banks can classify bonds as held to maturity only if they have both the intent and ability to hold on to them, rather than having to sell them to meet demands for withdrawals. For well-capitalized banks, that likely isn’t a tough judgment call to make.

But it is a much more nuanced issue for many of the lenders at the center of the latest banking crisis. Unlike the biggest banks, smaller banks are largely reliant on deposits for funding, which can prove flighty in stressed times, calling into question a bank’s ability to indefinitely hold long-term assets.