Paying Off Unfunded Pension Liabilities Will Be A Low Priority After COVID-19 (#GotBitcoin)

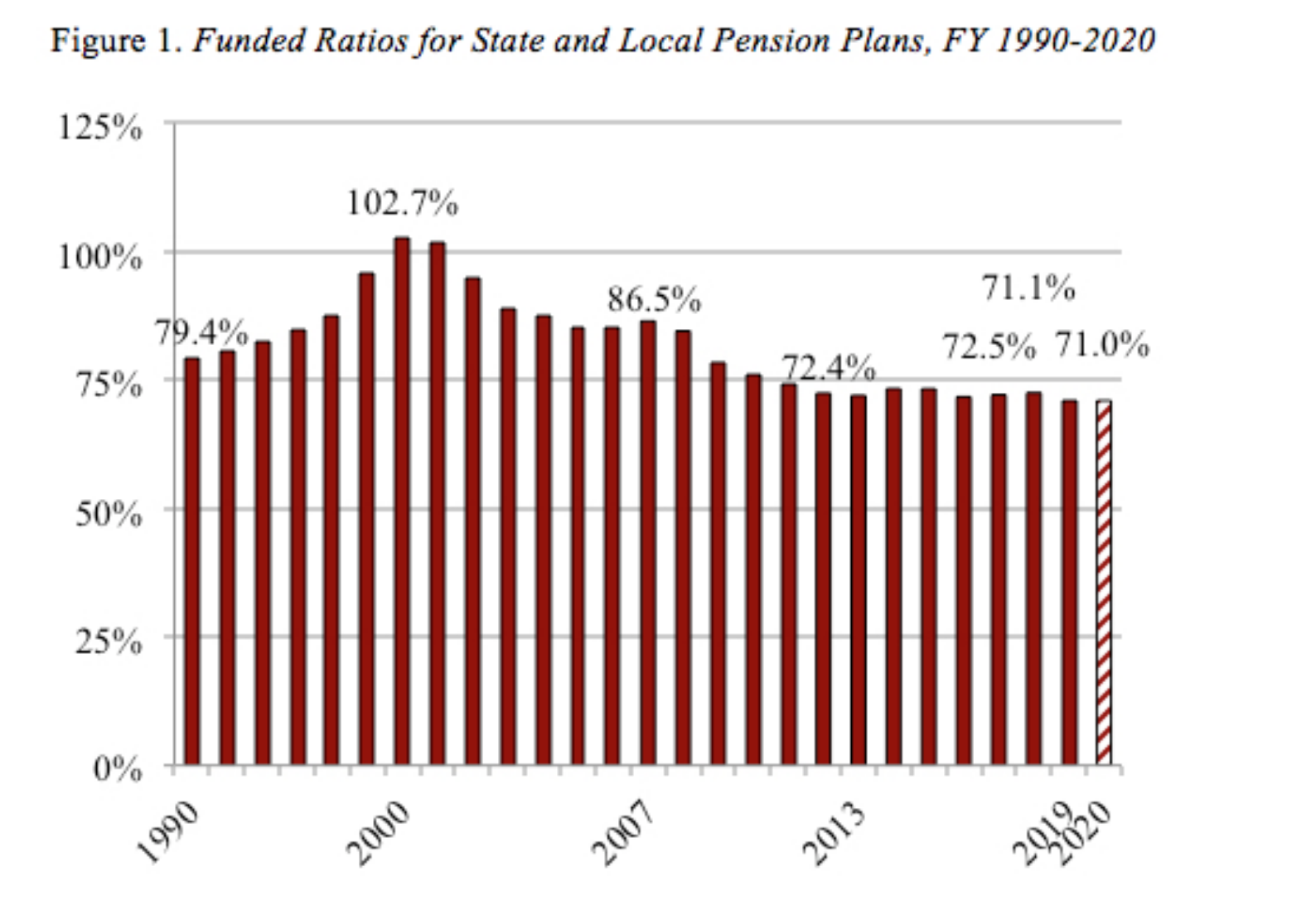

Our most recent update of state and local pension plans showed that — even after nearly a decade of stock market gains — plans were only about 70% funded in fiscal year 2020. Paying Off Unfunded Pension Liabilities Will Be A Low Priority After COVID-19 (#GotBitcoin)

That funded ratio discounts future benefits by the plan’s assumed rate of return (7.2%); the ratio would be lower with a lower discount rate (see figure 1).

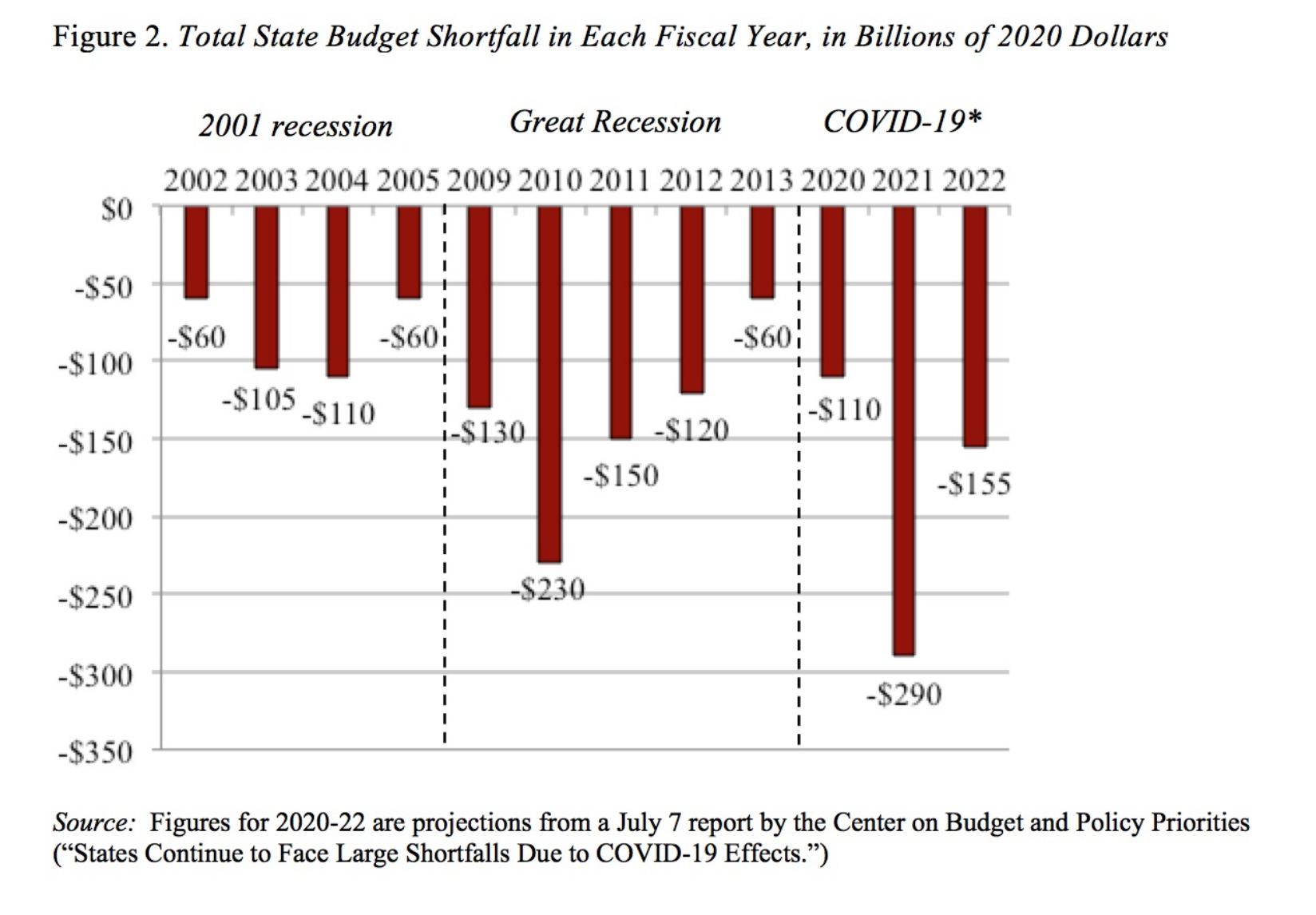

At the same time, experts from the Center on Budget and Policy Priorities (CBPP) predict that state budget shortfalls from the economic impact of COVID-19 will total a cumulative $555 billion over the period 2020-22. This figure is for states only and does not reflect revenue shortfalls at the local level.

Related:

Pension Funds And Insurance Firms Alive To Bitcoin Investment Proposal

Public Pensions Miss Fantastic Bitcoin Gains

The Pension Hole for U.S. Cities and States Is the Size of Japan’s Economy

Big Gains Did Little To Boost Corporate Pension Plans

The Long Bull Market Has Failed To Fix Public Pensions

World’s Top Pension Fund Books ‘Historic’ $339 Billion Gain

Ultimate Resource For Retirees And Retirement Planning

The CBPP reports that the projected gap for fiscal year 2021 alone (which started July 1 for most jurisdictions) is much larger than for any year during the Great Recession (see figure 2). The impact on governments has already been dramatic. In the last four months, states and localities have furloughed or laid off 1.5 million workers — double the number during the entire Great Recession.

In the next couple of years, states — which must balance their budgets every year — will face the tradeoff of deep cuts in education and health care and further layoffs, on the one hand, and funding their pensions on the other. Most observers would probably agree that pension funding could be postponed.

Related:

Ultimate Resource On Long COVID or (PASC)

Harvard Chemical Biology Department Chair Accused Of Selling Covid19 To Wuhan University

US Says China Backed Hackers Who Targeted COVID-19 Vaccine Research

Ultimate Resource For Covid-19 Vaccine Passports

Companies Plan Firings For Anti-Vaxers And Giveaways For Covid-19 Vaccine Recipients

Four Stories Of How People Traveled During Covid

How To Travel Luxuriously Post- Covid-19, From Private Jets To Hotel Buyouts

‘I Cry Every Day’: Olympic Athletes Slam Food, COVID Tests And Conditions In Beijing

Lessons Of The Great Depression: Preserving Wealth Amid The Covid-19 Crisis

Cyber Attack Hits Health And Human Services Department Amid Covid-19 Outbreak

More fundamentally, the standard recommendation that sponsors need to eliminate all their unfunded liability over 30 years is increasingly being called into question.

For years, we have argued that liabilities created before plans started to pre-fund their pension benefits should be taken off the backs of today’s workers and financed by outside sources as they come due (and coupled with more conservative funding methods — such as a lower discount rate and shorter amortization period — for liabilities created afterward). More recently, other researchers have made the case for stabilizing the ratio of unfunded liability to state GDP. Such a goal would also stabilize the ratio of debt service to output, requiring no further increases in taxes or cuts in outlays to maintain pensions.

These more moderate funding approaches seem sensible in the best of times. But they seem particularly helpful given the history of the 21st century, where the plans have been swamped with the retirement of baby boomers (a phenomenon that should end by 2030), two major market corrections in 2000-01 and 2007-09, and three recessions that depleted the revenues of state and local governments. In this context, blindly accumulating assets equal to 100% of the present value of promised benefits really doesn’t seem like a sensible goal.

Updated: 12-28-2020

Pensions Swamped In A Sea Of Negative Real Rates

It was hard enough for defined-benefit retirement plans to tread water before Covid-19. A slow recovery could put them in a near-impossible position.

Defined-benefit pension plans were already barely treading water heading into 2020. In the years ahead, the risk is as great as ever that a large swath of them will drown.

As the name implies, defined-benefit pensions promise to pay a set amount to retirees. While corporate America has largely moved away from this structure in favor of 401(k) options (or “defined contribution” plans), virtually all state and local governments still offer these reliable retirement payouts.

And they’ve been falling behind in a big way: In the 2019 fiscal year, states had $1.48 trillion in unfunded pension liabilities, while the 50 largest local governments faced $478 billion in adjusted net pension liabilities, according to calculations from Moody’s Investors Service. The 100 largest corporate defined-benefit plans had a deficit of $285 billion in November, according to Milliman data.

That $2 trillion hole is only going to get deeper as the Federal Reserve pledges to keep interest rates near record-low levels for years to come as the U.S. emerges from the Covid-19 pandemic. Moody’s, unlike many states and cities, uses a market-based discount rate to determine the present value of a pension’s future liabilities.

The lower the rate, the larger the current value. Analysts expect to apply a 2.7% rate to local governments’ fiscal 2021 reporting, down from 4.14% in fiscal 2018 and about the same as Milliman’s current discount rate for corporate pensions. It will likely cause pension shortfalls “to increase by double-digit percentages” in the next two years, Moody’s says.

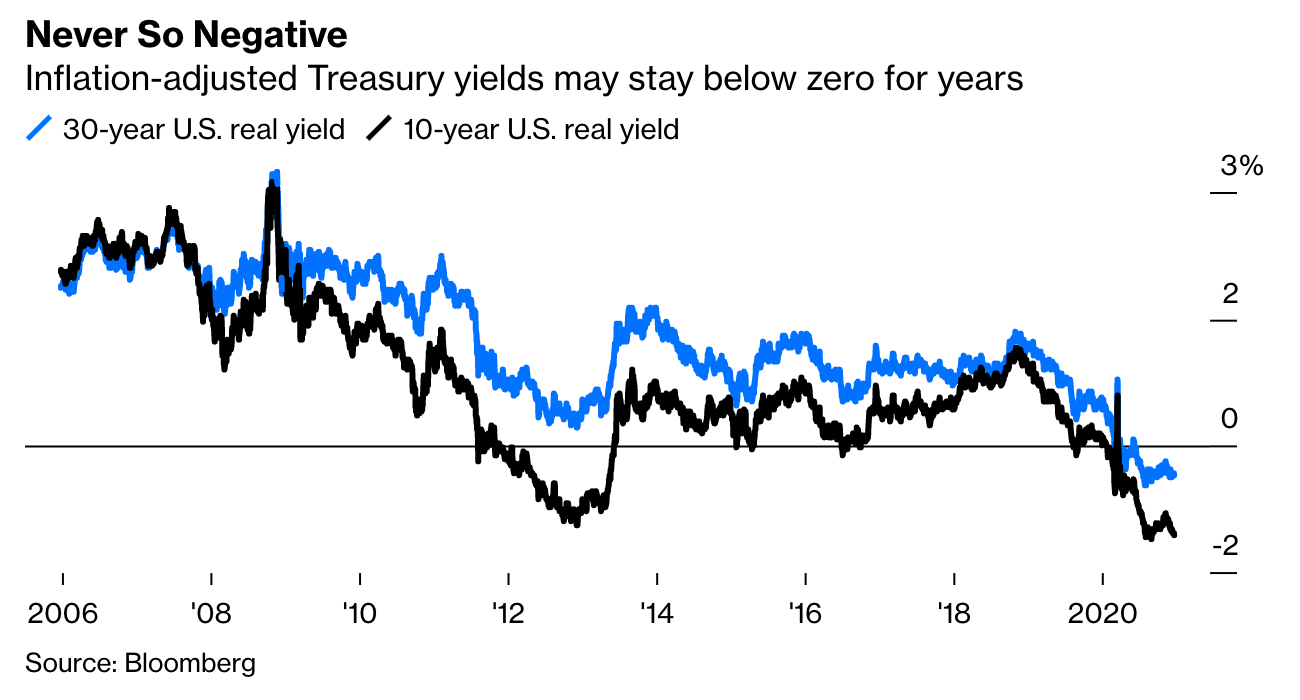

As harrowing as that seems, the 2.7% rate is likely to prove higher than anything pension-fund managers can hope to get from low-risk fixed-income assets, especially when adjusted for inflation. The 30-year U.S. real yield has been negative since mid-June after never falling below zero at any point since at least 2004.

That means even if pensions buy huge amounts of the longest-dated Treasuries, it’s nearly impossible for them to fully “immunize” by aligning principal and interest payments with payouts to retirees such that the value of its assets and liabilities rise and fall in tandem.

The only options, then, are to either shovel more money into the plans, take ever-greater risks with the cash promised to public workers or both. Because of Covid-19, many municipalities are strapped and don’t have much in the way of extra funds.

And pensions were already big players in alternative strategies like hedge funds and private equity, yet still fell behind in the decade after the global financial crisis as they assumed annual returns in the ballpark of 7%.

Ultralow interest rates can clearly help jump-start economic activity. Less-onerous mortgage rates open up homeownership to a larger share of Americans. Creditworthy companies can borrow cheaply for research, for new capital projects or, in the case of 2020, to avoid widespread layoffs.

The Fed, meanwhile, hopes that by keeping its short-term rate near zero until inflation overshoots its 2% target for an extended period of time, it will one day be able to conduct monetary policy further away from zero than it has in the past 12 years.

Until that day arrives, however, the plight of pension funds — and particularly public pensions — is only going to worsen. It’s one thing for the central bank to strong-arm wealthy individuals or multibillion-dollar endowments out of Treasuries and into riskier assets to earn a positive return. It’s quite another to jeopardize the system that has for decades ensured that teachers, police officers and firefighters are positioned for retirement.

“The prospect of an extended period of negative real rates makes it’s very difficult for the defined-benefit pension plans and insurance companies that depend on some level of relatively low risk return,” John Hollyer, global head of fixed income at Vanguard Group Inc., said in an interview.

He expects negative real rates to last for a few years. “One of the unintended consequences could be that sponsors of defined-benefit pension plans wind up having to make larger contributions to those plans to meet their obligations, and also restructure the plans over time.”

At BlackRock Inc., they’re calling this period the “new nominal.” It’s an era defined by stronger near-term growth and eventually higher inflation but without the usual increase in bond yields. “Central banks appear committed to limit any rises in nominal yields even as inflation picks up,” according to the BlackRock Investment Institute’s 2021 global outlook.

“Investors will need a new playbook to navigate this. We underweight government bonds and maintain a higher strategic allocation to equities than in typical periods of rising inflation.”

To Hollyer at Vanguard, this raises the risk of asset bubbles that the Fed might struggle to contain. By describing the set of conditions it would take to begin paring back asset purchases, and then to raise interest rates, the central bank is left mostly powerless to push back on some of the easiest financial conditions on record.

In a somewhat unusual move, Fed Chair Jerome Powell at his Dec. 16 press conference seemed to try to justify all-time high stock prices by noting that the 10-year Treasury yield was historically low and is expected to stay that way.

“I get that you have to be patient, but at some point the central banks do realize they have to restore government bond yields to a rational, positive level of real yield,” said Bob Michele, global head of fixed income at J.P. Morgan Asset Management.

“Insurance companies and pension funds, you’ve removed the ability for them to de-risk, and you’ve also inflated their liabilities.

At this level of bond yields, they’ll never be able to generate the 7% return on an ongoing basis that they need. They can absorb it over the short term, but longer term, it’s a reason to raise rates.”

In July, when 30-year Treasury yields were around 1.3%, Bank of America Corp. strategists warned that pension managers would revolt and stay away from the world’s biggest bond market until yields increased by “at least” 50 basis points. Otherwise, adding Treasuries would only “lock in such large funding gaps and also lock in low rates of return on the bonds.”

Five months later, the long bond hasn’t yet reached 1.8%, while the benchmark 10-year yield remains stubbornly below 1%.

While investors refuse to sell Treasuries, they’re also not keen on shedding stocks, either. The S&P 500 Index has moved in an almost linear fashion higher since the worst of the coronavirus pandemic in March and April.

It got to the point where I wrote that Chicago should be cheering on September’s decline in U.S. technology stocks so its underfunded pensions could buy the dip, potentially by issuing bonds to raise the funds. That drop didn’t last long.

“A drawdown in the market is a good thing,” said Nick Maroutsos, head of global bonds at Janus Henderson Investors. Without that, “it can be a problem because it’s going to hurt earnings, it’s going to hurt return expectations and just overall returns for future generations. And the lessons it teaches — any sort of selloff, you just buy it, knowing full well that defaults will be limited, money will be provided, liquidity will be there.”

Now, pensions are left with little choice but to risk it all and buy stocks near their all-time highs or give even more money to hedge funds or distressed credit managers. The alternative of adding investment-grade corporate bonds that yield less than 2% is a non-starter, to say nothing of Treasuries.

This is by design. Even if the Fed can’t as easily fire up its credit facilities in 2021, investors know they’re an option during periods of crisis. It’s enough to have potentially changed markets forever. Unfortunately, the central bank’s commitment to ultralow interest rates for years has also put defined-benefit plans on track for significant struggles ahead.

Related Articles:

Bitcoin Information & Resources (#GotBitcoin)

Pension Funds And Insurance Firms Alive To Bitcoin Investment Proposal

Ley Lines: The Earth’s Energy Highways

Ultimate Resource On Biden Administration’s Student-Loan Forgiveness Program

Biden’s Student Loan Freeze Shows Path To Erase Billions Of Debt

The Number Of Americans Who Say They Were Rejected For A Loan Reaches Highest Rate In 5 Years

Mass Immigration Experiment Gives Canada An Edge In Global Race For Labor

Silver Lining of Coronavirus, Return of Animals, Clear Skies, Quiet Streets And Tranquil Shores

Meet The Women Who Track Down And Kill Poachers

Ultimate Resource On President Joe Biden’s $1.3 Trillion Infrastructure Program

Electric Vehicle Infrastructure Push Brings Cyber Concerns

Ultimate Resource For Biden’s Infrastructure Plans And It’s Impact On The Crypto-Currency Industry

The Future of Water Is (And Toilets) Recycled Sewage, You’ll Drink It And You’ll Like It😹😂🤣

The Key To Tracking Diseases And Other Ailments Should Start With Sewers

Kia Motors America Victim of Ransomware Attack Demanding $20M In Bitcoin, Report Claims

This Massive Phishing Campaign Delivers Password-Stealing Malware Disguised As Ransomware

A New Ransomware Enters The Fray: Epsilon Red

UK Cyber Chief Cameron Says Ransomware Key Online Threat

It Was Not Until Anonymous Payment Systems That Ransomware Became A Problem

REvil Ransomware Hits 200 Companies In MSP Supply-Chain Attack

Russia ‘Cozy Bear’ Breached GOP As Ransomware Attack Hit

US Fights Ransomware With Crypto Tracing, $10 Million Bounties

US Taps Amazon, Google, Microsoft, Others To Help Fight Ransomware, Cyber Threats

Google’s Chrome Browser Is Under Active Attack, Patch Now!!!!

Leaked Chainalysis Documents Reveal Company Is Advertising An IP-Scraping System To Law Enforcement

Hackers Breach Thousands of Security Cameras, Exposing Tesla, Jails, Hospitals

Major Hospital System Hit With Cyberattack, Potentially Largest In U.S. History

A Hospital Hit By Hackers, A Baby In Distress: The Case Of The First Alleged Ransomware Death

Major League Cricket Takes Off In US

America Is Wrapped In Miles of Toxic Lead Cables

What Is Dollar Cost Averaging Bitcoin?

The NASA Engineer Who Made The James Webb Space Telescope Work

The Webb Telescope Turns Big Bang Theory Upside-Down

Wagner Group: A State-Backed Russian Paramilitary Cartel

Debt Collectors’ Awkward Moment: Their Own Debt Is Now Sinking

Ultimate Resource On Brittney Griner Being Held In Russian Jail

Mocked As ‘Rubble’ By Biden, Russia’s Ruble Roars Back

Ultimate Resource On Russia’s Involvement With Bitcoin

What Is Structured Water: The Best Water For Muscular, Skin & Mood Disorders?

“Would Someone Please Buy US Treasury Bonds?” Janet Yellen #GotBitcoin

‘It Will Send BTC’ — On-Chain Analyst Says Bitcoin Hodlers Are Only Getting Stronger

HODLing Early Leads To Relationship Troubles? Redditors Share Their Stories

Governments Will Start To Hodl Bitcoin In 2021

Bitcoin’s Value Is All In The Eye Of The ‘Bithodler’

Ultimate Resource On Blue And Green Hydrogen As Alternative Energy

Ultimate Resource On Small And Mega-Battery Innovations And Facilities

Governments Turn Against Deep-Sea Mining In The Face Of Increase In Demand For Metals

How To Bulk: A Complete Workout And Nutrition Plan For Muscle Growth

What You Should Know About ‘529’ Education-Savings Accounts

Kia And Hyundai To Pay $200 Million To Settle Viral Car-Theft Suit

Stock Clearinghouse Leaked Sensitive Data, Trading Firm Says #GotBitcoin

Scarlette Bourne Joins Our List of 2023’s Most Influential Women

Surge In Celebrities And Others Contributing To Nonprofits Focusing On Blacks

Israel-Gaza Conflict Spurs Bitcoin Donations To Hamas

Signal Encrypted Messenger Now Accepts Donations In Bitcoin

Melinda Gates Welcomes The Philanthropists Of The Future

Who Gets How Much: Big Questions About Reparations For Slavery

California Lawmakers Vote To Create Reparations Task Force

US City To Pay Reparations To African-American Community With Tax On Marijuana Sales

Ultimate Resource On Australia’s Involvement With Bitcoin

Famous Former Bitcoin Critics Who Conceded In 2020-23

The Latest On FBI Warrantless Searches of Americans’ Communications #GotBitcoin

America’s Spies Are Losing Their Edge

Powell Got Punk’d By Putin’s Puppets

‘What Housewife Isn’t On Ozempic?’ How A Weight-Loss Craze Is Sweeping Across America

Snoop Dogg’s Net Worth Is Almost As High As He (Usually) Is

Is It Just Me Or Is America Having A Mental Breakdown? Joker

CFPB (Idiots) Says Staffer Sent 250,000 Consumers’ Data To Personal Account #GotBitcoin

Global Bitcoin Game Theory Is Now Playing Out

Operation Choke Point 2.0 Could Be Bitcoin’s Biggest Banking Crackdown And Regulatory Battle

The US Cracked A $3.4 Billion Crypto Heist—And Bitcoin’s Pseudo-Anonymity😹🤣😂

Twitter To Launch Bitcoin And Stock Trading In Partnership With eToro

Rich Chinese Splashing Out On Luxury In Singapore

Apple Sues NSO Group To Curb The Abuse Of State-Sponsored Spyware

Harvard Quietly Amasses California Vineyards—And The Water Underneath (#GotBitcoin)

US Says China Backed Hackers Who Targeted COVID-19 Vaccine Research

Ultimate Resource For Covid-19 Vaccine Passports

Companies Plan Firings For Anti-Vaxers And Giveaways For Covid-19 Vaccine Recipients

US Bank Lending Slumps By Most On Record In Final Weeks Of March And It’s Impact On Home Buyers

California Defies Doom With No. 1 U.S. Economy

California Wants Its Salton Sea Located In The Imperial Valley To Be ‘Lithium Valley’

Ultimate Resource For Nationwide Firsts Taking Place In California (#GotBitcoin)

Flight To Money Funds Is Adding To The Strains On Banks #GotBitcoin

The Fed Loses Money For The First Time In 107 Years – Why It Matters #GotBitcoin

African Safari Vacation Itinerary (2024 Proposal)

The Next Fountain-of-Youth Craze? Peptide Injections

This Ocean Monster Offers A Potential Climate Solution

What Are Credit Default Swaps, How Do They Work, And How They Go Wrong

Cyberattack Sends Quadrillion Dollars Derivative’s Trading Markets Back To The 1980s #GotBitcoin

What Is Dopamine Fasting? Meet The Dangerous Fad Among Silicon Valley’s Tech Geniuses

Bitcoin Community Leaders Join Longevity Movement

Sean Harribance Shares His Psychic Gifts With The Public

Scientists Achieve Real-Time Communication With Lucid Dreamers In Breakthrough

Does Getting Stoned Help You Get Toned? Gym Rats Embrace Marijuana

Marijuana In Africa Is Like The Gold Rush For America In The 1800s

The Perfect Wine And Weed To Get You Through The Coronavirus Pandemic Lockdown

Mike Tyson’s 420-Acre Weed Ranch Rakes In $500K A Month

What Sex Workers Want To Do With Bitcoin

“Is Bitcoin Reacting To The Chaos Or Is Bitcoin Causing The Chaos?” Max Keiser

How To Safely Store Deposits If You Have More Than $250,000

How To Host A Decentralized Website

Banks Lose Billions (Approx. $52 Billion) As Depositors Seek Higher Deposit Yields #GotBitcoin

Crypto User Recovers Long-Lost Private Keys To Access $4M In Bitcoin

Stripe Stops Processing Payments For Trump Campaign Website

Bitcoin Whales Are Profiting As ‘Weak Hands’ Sell BTC After Price Correction

Pentagon Sees Giant Cargo Cranes As Possible Chinese Spying Tools

Bitcoin’s Volatility Should Burn Investors. It Hasn’t

Bitcoin’s Latest Record Run Is Less Volatile Than The 2017 Boom

“Lettuce Hands” Refers To Investors Who Can’t Deal With The Volatility Of The Cryptocurrency Markets

The Bitcoiners Who Live Off The Grid

US Company Now Lets Travelers Pay For Passports With Bitcoin

After A Year Without Rowdy Tourists, European Cities Want To Keep It That Way

Director Barry Jenkins Is The Travel Nerd’s Travel Nerd

Four Stories Of How People Traveled During Covid

Who Is A Perpetual Traveler (AKA Digital Nomad) Under The US Tax Code

Tricks For Making A Vacation Feel Longer—And More Fulfilling

Travel Has Bounced Back From Coronavirus, But Tourists Stick Close To Home

Nurses Travel From Coronavirus Hot Spot To Hot Spot, From New York To Texas

How To Travel Luxuriously Post- Covid-19, From Private Jets To Hotel Buyouts

Ultimate Travel Resource Covering Business, Personal, Cruise, Flying, Etc.)

Does Bitcoin Boom Mean ‘Better Gold’ Or Bigger Bubble?

Bitcoin’s Slide Dents Price Momentum That Dwarfed Everything

Retail Has Arrived As Paypal Clears $242M In Crypto Sales Nearly Double The Previous Record

Jarlsberg Cheese Offers Significant Bone & Heart-Health Benefits Thanks To Vitamin K2, Says Study

Chrono-Pharmacology Reveals That “When” You Take Your Medication Can Make A Life-Saving Difference

Ultimate Resource For News, Breakthroughs And Innovations In Healthcare

Ultimate Resource For Cooks, Chefs And The Latest Food Trends

Ethereum Use Cases You Might Not Know

Will 1% Yield Force The Fed Into Curve Control?

Ultimate Resource On Hong Kong Vying For World’s Crypto Hub #GotBitcoin

France Moves To Ban Anonymous Crypto Accounts To Prevent Money Laundering

Numerous Times That US (And Other) Regulators Stepped Into Crypto

Where Does This 28% Bitcoin Price Drop Rank In History? Not Even In The Top 5

Traditional Investors View Bitcoin As If It Were A Technology Stock

3 Reasons Why Bitcoin Price Abruptly Dropped 6% After Reaching $15,800

As Bitcoin Approaches $25,000 It Breaks Correlation With Equities

UK Treasury Calls For Feedback On Approach To Cryptocurrency And Stablecoin Regulation

Bitcoin Rebounds While Leaving Everyone In Dark On True Worth

Slow-Twitch vs. Fast-Twitch Muscle Fibers

Biden, Obama Release Campaign Video Applauding Their Achievements

Joe Biden Tops Donald Trump In Polls And Leads In Fundraising (#GotBitcoin)

Trump Gets KPOP’d And Tic Toc’d As Teens Mobilized To Derail Trump’s Tulsa Rally

Schwab’s $200 Million Charge Puts Scrutiny On Robo-Advising

TikTok Is The Place To Go For Financial Advice If You’re A Young Adult

TikTok Is The Place To Go For Financial Advice If You’re A Young Adult

American Shoppers Just Can’t Pass Up A Bargain And Department Stores Pay The Price #GotBitcoin

Motley Fool Adding $5M In Bitcoin To Its ‘10X Portfolio’ — Has A $500K Price Target

Mad Money’s Jim Cramer Invests 1% Of Net Worth In Bitcoin Says, “Gold Is Dangerous”

Ultimate Resource For Financial Advisers By Financial Advisers On Crypto

Anti-ESG Movement Reveals How Blackrock Pulls-off World’s Largest Ponzi Scheme

The Bitcoin Ordinals Protocol Has Caused A Resurgence In Bitcoin Development And Interest

Bitcoin Takes ‘Lion’s Share’ As Institutional Inflows Hit 7-Month High

Bitcoin’s Future Depends On A Handful of Mysterious Coders

Billionaire Hedge Fund Investor Stanley Druckenmiller Says He Owns Bitcoin In CNBC Interview

Bitcoin Billionaire Chamath Palihapitiya Opts Out Of Run For California Governor

Billionaire Took Psychedelics, Got Bitcoin And Is Now Into SPACs

Billionaire’s Bitcoin Dream Shapes His Business Empire In Norway

Trading Firm Of Richest Crypto Billionaire Reveals Buying ‘A Lot More’ Bitcoin Below $30K

Simple Tips To Ensure Your Digital Surveillance Works As It Should

Big (4) Audit Firms Blasted By PCAOB And Gary Gensler, Head Of SEC (#GotBitcoin)

What Crypto Users Need Know About Changes At The SEC

The Ultimate Resource For The Bitcoin Miner And The Mining Industry (Page#2) #GotBitcoin

How Cryptocurrency Can Help In Paying Universal Basic Income (#GotBitcoin)

Gautam Adani Was Briefly World’s Richest Man Only To Be Brought Down By An American Short-Seller

Global Crypto Industry Pledges Aid To Turkey Following Deadly Earthquakes

Money Supply Growth Went Negative Again In December Another Sign Of Recession #GotBitcoin

Here Is How To Tell The Difference Between Bitcoin And Ethereum

Crypto Investors Can Purchase Bankruptcy ‘Put Options’ To Protect Funds On Binance, Coinbase, Kraken

Bitcoin Developers Must Face UK Trial Over Lost Cryptoassets

Google Issues Warning For 2 Billion Chrome Users

How A Lawsuit Against The IRS Is Trying To Expand Privacy For Crypto Users

IRS Uses Cellphone Location Data To Find Suspects

IRS Failed To Collect $2.4 Billion In Taxes From Millionaires

Treasury Calls For Crypto Transfers Over $10,000 To Be Reported To IRS

Can The IRS Be Trusted With Your Data?

US Ransomware Attack Suspect Hails From A Small Ukrainian Town

Alibaba Admits It Was Slow To Report Software Bug After Beijing Rebuke

Japan Defense Ministry Finds Security Threat In Hack

Raoul Pal Believes Institutions Have Finished Taking Profits As Year Winds Up

Yosemite Is Forcing Native American Homeowners To Leave Without Compensation. Here’s Why

What Is Dollar Cost Averaging Bitcoin?

Ultimate Resource On Bitcoin Unit Bias

Best Travel Credit Cards of 2022-2023

A Guarded Generation: How Millennials View Money And Investing (#GotBitcoin)

Bitcoin Enthusiast And CEO Brian Armstrong Buys Los Angeles Home For $133 Million

Nasdaq-Listed Blockchain Firm BTCS To Offer Dividend In Bitcoin; Shares Surge

Ultimate Resource On Kazakhstan As Second In Bitcoin Mining Hash Rate In The World After US

Ultimate Resource On Solana Outages And DDoS Attacks

How Jessica Simpson Almost Lost Her Name And Her Billion Dollar Empire

Sidney Poitier, Actor Who Made Oscars History, Dies At 94

Green Comet Will Be Visible As It Passes By Earth For First Time In 50,000 Years

FTX (SBF) Got Approval From F.D.I.C., State Regulators And Federal Reserve To Buy Tiny Bank!!!

Joe Rogan: I Have A Lot Of Hope For Bitcoin

Teen Cyber Prodigy Stumbled Onto Flaw Letting Him Hijack Teslas

Spyware Finally Got Scary Enough To Freak Lawmakers Out—After It Spied On Them

The First Nuclear-Powered Bitcoin Mine Is Here. Maybe It Can Clean Up Energy FUD

The World’s Best Crypto Policies: How They Do It In 37 Nations

Tonga To Copy El Salvador’s Bill Making Bitcoin Legal Tender, Says Former MP

Wordle Is The New “Lingo” Turning Fans Into Argumentative Strategy Nerds

Prospering In The Pandemic, Some Feel Financial Guilt And Gratitude

Is Art Therapy The Path To Mental Well-Being?

New York, California, New Jersey, And Alabama Move To Ban ‘Forever Chemicals’ In Firefighting Foam

The Mystery Of The Wasting House-Cats

What Pet Owners Should Know About Chronic Kidney Disease In Dogs And Cats

Pets Score Company Perks As The ‘New Dependents’

Why Is My Cat Rubbing His Face In Ants?

Natural Cure For Hyperthyroidism In Cats Including How To Switch Him/Her To A Raw Food Diet

Ultimate Resource For Cat Lovers

FDA Approves First-Ever Arthritis Pain Management Drug For Cats

Ultimate Resource On Duke of York’s Prince Andrew And His Sex Scandal

Walmart Filings Reveal Plans To Create Cryptocurrency, NFTs

Bitcoin’s Dominance of Crypto Payments Is Starting To Erode

T-Mobile Says Hackers Stole Data On About 37 Million Customers

Jack Dorsey Announces Bitcoin Legal Defense Fund

More Than 100 Millionaires Signed An Open Letter Asking To Be Taxed More Heavily

Federal Regulator Says Credit Unions Can Partner With Crypto Providers

What’s Behind The Fascination With Smash-And-Grab Shoplifting?

Train Robberies Are A Problem In Los Angeles, And No One Agrees On How To Stop Them

US Stocks Historically Deliver Strong Gains In Fed Hike Cycles (GotBitcoin)

Ian Alexander Jr., Only Child of Regina King, Dies At Age 26

Amazon Ends Its Charity Donation Program Amazonsmile After Other Cost-Cutting Efforts

Indexing Is Coming To Crypto Funds Via Decentralized Exchanges

Doctors Show Implicit Bias Towards Black Patients

Darkmail Pushes Privacy Into The Hands Of NSA-Weary Customers

3D Printing Make Anything From Candy Bars To Hand Guns

Stealing The Blood Of The Young May Make You More Youthful

Henrietta Lacks And Her Remarkable Cells Will Finally See Some Payback

AL_A Wins Approval For World’s First Magnetized Fusion Power Plant

Want To Be Rich? Bitcoin’s Limited Supply Cap Means You Only Need 0.01 BTC

Smart Money Is Buying Bitcoin Dip. Stocks, Not So Much

McDonald’s Jumps On Bitcoin Memewagon, Crypto Twitter Responds

America COMPETES Act Would Be Disastrous For Bitcoin Cryptocurrency And More

Lyn Alden On Bitcoin, Inflation And The Potential Coming Energy Shock

Inflation And A Tale of Cantillionaires

El Salvador Plans Bill To Adopt Bitcoin As Legal Tender

Miami Mayor Says City Employees Should Be Able To Take Their Salaries In Bitcoin

Vast Troves of Classified Info Undermine National Security, Spy Chief Says

BREAKING: Arizona State Senator Introduces Bill To Make Bitcoin Legal Tender

San Francisco’s Historic Surveillance Law May Get Watered Down

How Bitcoin Contributions Funded A $1.4M Solar Installation In Zimbabwe

California Lawmaker Says National Privacy Law Is a Priority

The Pandemic Turbocharged Online Privacy Concerns

How To Protect Your Online Privacy While Working From Home

Researchers Use GPU Fingerprinting To Track Users Online

Japan’s $1 Trillion Crypto Market May Ease Onerous Listing Rules

Ultimate Resource On A Weak / Strong Dollar’s Impact On Bitcoin

Fed Money Printer Goes Into Reverse (Quantitative Tightening): What Does It Mean For Crypto?

Crypto Market Is Closer To A Bottom Than Stocks (#GotBitcoin)

When World’s Central Banks Get It Wrong, Guess Who Pays The Price😂😹🤣 (#GotBitcoin)

“Better Days Ahead With Crypto Deleveraging Coming To An End” — Joker

Crypto Funds Have Seen Record Investment Inflow In Recent Weeks

Bitcoin’s Epic Run Is Winning More Attention On Wall Street

Ultimate Resource For Crypto Mergers And Acquisitions (M&A) (#GotBitcoin)

Why Wall Street Is Literally Salivating Over Bitcoin

Nasdaq-Listed MicroStrategy And Others Wary Of Looming Dollar Inflation, Turns To Bitcoin And Gold

Bitcoin For Corporations | Michael Saylor | Bitcoin Corporate Strategy

Ultimate Resource On Myanmar’s Involvement With Crypto-Currencies

‘I Cry Every Day’: Olympic Athletes Slam Food, COVID Tests And Conditions In Beijing

Does Your Baby’s Food Contain Toxic Metals? Here’s What Our Investigation Found

Ultimate Resource For Pro-Crypto Lobbying And Non-Profit Organizations

Ultimate Resource On BlockFi, Celsius And Nexo

Petition Calling For Resignation Of U.S. Securities/Exchange Commission Chair Gary Gensler

100 Million Americans Can Legally Bet on the Super Bowl. A Spot Bitcoin ETF? Forget About it!

Green Finance Isn’t Going Where It’s Needed

Shedding Some Light On The Murky World Of ESG Metrics

SEC Targets Greenwashers To Bring Law And Order To ESG

BlackRock (Assets Under Management $7.4 Trillion) CEO: Bitcoin Has Caught Our Attention

Canada’s Major Banks Go Offline In Mysterious (Bank Run?) Hours-Long Outage (#GotBitcoin)

On-Chain Data: A Framework To Evaluate Bitcoin

On Its 14th Birthday, Bitcoin’s 1,690,706,971% Gain Looks Kind of… Well Insane

The Most Important Health Metric Is Now At Your Fingertips

American Bargain Hunters Flock To A New Online Platform Forged In China

Why We Should Welcome Another Crypto Winter

Traders Prefer Gold, Fiat Safe Havens Over Bitcoin As Russia Goes To War

Music Distributor DistroKid Raises Money At $1.3 Billion Valuation

Nas Selling Rights To Two Songs Via Crypto Music Startup Royal

Ultimate Resource On Music Catalog Deals

Ultimate Resource On Music And NFTs And The Implications For The Entertainment Industry

Lead And Cadmium Could Be In Your Dark Chocolate

Catawba, Native-American Tribe Approves First Digital Economic Zone In The United States

The Miracle Of Blockchain’s Triple Entry Accounting

How And Why To Stimulate Your Vagus Nerve!

Housing Boom Brings A Shortage Of Land To Build New Homes

Biden Lays Out His Blueprint For Fair Housing

No Grave Dancing For Sam Zell Now. He’s Paying Up For Hot Properties

Cracks In The Housing Market Are Starting To Show

Ever-Growing Needs Strain U.S. Food Bank Operations

Food Pantry Helps Columbia Students Struggling To Pay Bills

Food Insecurity Driven By Climate Change Has Central Americans Fleeing To The U.S.

Housing Insecurity Is Now A Concern In Addition To Food Insecurity

Families Face Massive Food Insecurity Levels

US Troops Going Hungry (Food Insecurity) Is A National Disgrace

Everything You Should Know About Community Fridges, From Volunteering To Starting Your Own

Russia’s Independent Journalists Including Those Who Revealed The Pandora Papers Need Your Help

10 Women Who Used Crypto To Make A Difference In 2021

Happy International Women’s Day! Leaders Share Their Experiences In Crypto

Dollar On Course For Worst Performance In Over A Decade (#GotBitcoin)

Juice The Stock Market And Destroy The Dollar!! (#GotBitcoin)

Unusual Side Hustles You May Not Have Thought Of

Ultimate Resource On Global Inflation And Rising Interest Rates (#GotBitcoin)

The Fed Is Setting The Stage For Hyper-Inflation Of The Dollar (#GotBitcoin)

An Antidote To Inflation? ‘Buy Nothing’ Groups Gain Popularity

Why Is Bitcoin Dropping If It’s An ‘Inflation Hedge’?

Lyn Alden Talks Bitcoin, Inflation And The Potential Coming Energy Shock

Ultimate Resource On How Black Families Can Fight Against Rising Inflation (#GotBitcoin)

What The Fed’s Rate Hike Means For Inflation, Housing, Crypto And Stocks

Egyptians Buy Bitcoin Despite Prohibitive New Banking Laws

Archaeologists Uncover Five Tombs In Egypt’s Saqqara Necropolis

History of Alchemy From Ancient Egypt To Modern Times

Former World Bank Chief Didn’t Act On Warnings Of Sexual Harassment

Does Your Hospital or Doctor Have A Financial Relationship With Big Pharma?

Ultimate Resource Covering The Crisis Taking Place In The Nickel Market

Apple Along With Meta And Secret Service Agents Fooled By Law Enforcement Impersonators

Handy Tech That Can Support Your Fitness Goals

How To Naturally Increase Your White Blood Cell Count

Ultimate Source For Russians Oligarchs And The Impact Of Sanctions On Them

Ultimate Source For Bitcoin Price Manipulation By Wall Street

Russia, Sri Lanka And Lebanon’s Defaults Could Be The First Of Many (#GotBitcoin)

Will Community Group Buying Work In The US?

Building And Running Businesses In The ‘Spirit Of Bitcoin’

What Is The Mysterious Liver Disease Hurting (And Killing) Children?

Citigroup Trader Is Scapegoat For Flash Crash In European Stocks (#GotBitcoin)

Bird Flu Outbreak Approaches Worst Ever In U.S. With 37 Million Animals Dead

Financial Inequality Grouped By Race For Blacks, Whites And Hispanics

How Black Businesses Can Prosper From Targeting A Trillion-Dollar Black Culture Market (#GotBitcoin)

Ultimate Resource For Central Bank Digital Currencies (#GotBitcoin) Page#2

Meet The Crypto Angel Investor Running For Congress In Nevada (#GotBitcoin?)

Introducing BTCPay Vault – Use Any Hardware Wallet With BTCPay And Its Full Node (#GotBitcoin?)

How Not To Lose Your Coins In 2020: Alternative Recovery Methods (#GotBitcoin?)

H.R.5635 – Virtual Currency Tax Fairness Act of 2020 ($200.00 Limit) 116th Congress (2019-2020)

Adam Back On Satoshi Emails, Privacy Concerns And Bitcoin’s Early Days

The Prospect of Using Bitcoin To Build A New International Monetary System Is Getting Real

How To Raise Funds For Australia Wildfire Relief Efforts (Using Bitcoin And/Or Fiat )

Former Regulator Known As ‘Crypto Dad’ To Launch Digital-Dollar Think Tank (#GotBitcoin?)

Currency ‘Cold War’ Takes Center Stage At Pre-Davos Crypto Confab (#GotBitcoin?)

A Blockchain-Secured Home Security Camera Won Innovation Awards At CES 2020 Las Vegas

Bitcoin’s Had A Sensational 11 Years (#GotBitcoin?)

Sergey Nazarov And The Creation Of A Decentralized Network Of Oracles

Google Suspends MetaMask From Its Play App Store, Citing “Deceptive Services”

Christmas Shopping: Where To Buy With Crypto This Festive Season

At 8,990,000% Gains, Bitcoin Dwarfs All Other Investments This Decade

Coinbase CEO Armstrong Wins Patent For Tech Allowing Users To Email Bitcoin

Bitcoin Has Got Society To Think About The Nature Of Money

How DeFi Goes Mainstream In 2020: Focus On Usability (#GotBitcoin?)

Dissidents And Activists Have A Lot To Gain From Bitcoin, If Only They Knew It (#GotBitcoin?)

At A Refugee Camp In Iraq, A 16-Year-Old Syrian Is Teaching Crypto Basics

Bitclub Scheme Busted In The US, Promising High Returns From Mining

Bitcoin Advertised On French National TV

Germany: New Proposed Law Would Legalize Banks Holding Bitcoin

How To Earn And Spend Bitcoin On Black Friday 2019

The Ultimate List of Bitcoin Developments And Accomplishments

Charities Put A Bitcoin Twist On Giving Tuesday

Family Offices Finally Accept The Benefits of Investing In Bitcoin

An Army Of Bitcoin Devs Is Battle-Testing Upgrades To Privacy And Scaling

Bitcoin ‘Carry Trade’ Can Net Annual Gains With Little Risk, Says PlanB

Max Keiser: Bitcoin’s ‘Self-Settlement’ Is A Revolution Against Dollar

Blockchain Can And Will Replace The IRS

China Seizes The Blockchain Opportunity. How Should The US Respond? (#GotBitcoin?)

Jack Dorsey: You Can Buy A Fraction Of Berkshire Stock Or ‘Stack Sats’

Bitcoin Price Skyrockets $500 In Minutes As Bakkt BTC Contracts Hit Highs

Bitcoin’s Irreversibility Challenges International Private Law: Legal Scholar

Bitcoin Has Already Reached 40% Of Average Fiat Currency Lifespan

Yes, Even Bitcoin HODLers Can Lose Money In The Long-Term: Here’s How (#GotBitcoin?)

Unicef To Accept Donations In Bitcoin (#GotBitcoin?)

Former Prosecutor Asked To “Shut Down Bitcoin” And Is Now Face Of Crypto VC Investing (#GotBitcoin?)

Switzerland’s ‘Crypto Valley’ Is Bringing Blockchain To Zurich

Next Bitcoin Halving May Not Lead To Bull Market, Says Bitmain CEO

Bitcoin Developer Amir Taaki, “We Can Crash National Economies” (#GotBitcoin?)

Veteran Crypto And Stocks Trader Shares 6 Ways To Invest And Get Rich

Is Chainlink Blazing A Trail Independent Of Bitcoin?

Nearly $10 Billion In BTC Is Held In Wallets Of 8 Crypto Exchanges (#GotBitcoin?)

SEC Enters Settlement Talks With Alleged Fraudulent Firm Veritaseum (#GotBitcoin?)

Blockstream’s Samson Mow: Bitcoin’s Block Size Already ‘Too Big’

Attorneys Seek Bank Of Ireland Execs’ Testimony Against OneCoin Scammer (#GotBitcoin?)

OpenLibra Plans To Launch Permissionless Fork Of Facebook’s Stablecoin (#GotBitcoin?)

Tiny $217 Options Trade On Bitcoin Blockchain Could Be Wall Street’s Death Knell (#GotBitcoin?)

Class Action Accuses Tether And Bitfinex Of Market Manipulation (#GotBitcoin?)

Sharia Goldbugs: How ISIS Created A Currency For World Domination (#GotBitcoin?)

Bitcoin Eyes Demand As Hong Kong Protestors Announce Bank Run (#GotBitcoin?)

How To Securely Transfer Crypto To Your Heirs

‘Gold-Backed’ Crypto Token Promoter Karatbars Investigated By Florida Regulators (#GotBitcoin?)

Crypto News From The Spanish-Speaking World (#GotBitcoin?)

Financial Services Giant Morningstar To Offer Ratings For Crypto Assets (#GotBitcoin?)

‘Gold-Backed’ Crypto Token Promoter Karatbars Investigated By Florida Regulators (#GotBitcoin?)

The Original Sins Of Cryptocurrencies (#GotBitcoin?)

Bitcoin Is The Fraud? JPMorgan Metals Desk Fixed Gold Prices For Years (#GotBitcoin?)

Israeli Startup That Allows Offline Crypto Transactions Secures $4M (#GotBitcoin?)

[PSA] Non-genuine Trezor One Devices Spotted (#GotBitcoin?)

Bitcoin Stronger Than Ever But No One Seems To Care: Google Trends (#GotBitcoin?)

First-Ever SEC-Qualified Token Offering In US Raises $23 Million (#GotBitcoin?)

You Can Now Prove A Whole Blockchain With One Math Problem – Really

Crypto Mining Supply Fails To Meet Market Demand In Q2: TokenInsight

$2 Billion Lost In Mt. Gox Bitcoin Hack Can Be Recovered, Lawyer Claims (#GotBitcoin?)

Fed Chair Says Agency Monitoring Crypto But Not Developing Its Own (#GotBitcoin?)

Wesley Snipes Is Launching A Tokenized $25 Million Movie Fund (#GotBitcoin?)

Mystery 94K BTC Transaction Becomes Richest Non-Exchange Address (#GotBitcoin?)

A Crypto Fix For A Broken International Monetary System (#GotBitcoin?)

Four Out Of Five Top Bitcoin QR Code Generators Are Scams: Report (#GotBitcoin?)

Waves Platform And The Abyss To Jointly Launch Blockchain-Based Games Marketplace (#GotBitcoin?)

Bitmain Ramps Up Power And Efficiency With New Bitcoin Mining Machine (#GotBitcoin?)

Ledger Live Now Supports Over 1,250 Ethereum-Based ERC-20 Tokens (#GotBitcoin?)

Miss Finland: Bitcoin’s Risk Keeps Most Women Away From Cryptocurrency (#GotBitcoin?)

Artist Akon Loves BTC And Says, “It’s Controlled By The People” (#GotBitcoin?)

Ledger Live Now Supports Over 1,250 Ethereum-Based ERC-20 Tokens (#GotBitcoin?)

Co-Founder Of LinkedIn Presents Crypto Rap Video: Hamilton Vs. Satoshi (#GotBitcoin?)

Crypto Insurance Market To Grow, Lloyd’s Of London And Aon To Lead (#GotBitcoin?)

No ‘AltSeason’ Until Bitcoin Breaks $20K, Says Hedge Fund Manager (#GotBitcoin?)

NSA Working To Develop Quantum-Resistant Cryptocurrency: Report (#GotBitcoin?)

Custody Provider Legacy Trust Launches Crypto Pension Plan (#GotBitcoin?)

Vaneck, SolidX To Offer Limited Bitcoin ETF For Institutions Via Exemption (#GotBitcoin?)

Russell Okung: From NFL Superstar To Bitcoin Educator In 2 Years (#GotBitcoin?)

Bitcoin Miners Made $14 Billion To Date Securing The Network (#GotBitcoin?)

Why Does Amazon Want To Hire Blockchain Experts For Its Ads Division?

Argentina’s Economy Is In A Technical Default (#GotBitcoin?)

Blockchain-Based Fractional Ownership Used To Sell High-End Art (#GotBitcoin?)

Portugal Tax Authority: Bitcoin Trading And Payments Are Tax-Free (#GotBitcoin?)

Bitcoin ‘Failed Safe Haven Test’ After 7% Drop, Peter Schiff Gloats (#GotBitcoin?)

Bitcoin Dev Reveals Multisig UI Teaser For Hardware Wallets, Full Nodes (#GotBitcoin?)

Bitcoin Price: $10K Holds For Now As 50% Of CME Futures Set To Expire (#GotBitcoin?)

Bitcoin Realized Market Cap Hits $100 Billion For The First Time (#GotBitcoin?)

Stablecoins Begin To Look Beyond The Dollar (#GotBitcoin?)

Bank Of England Governor: Libra-Like Currency Could Replace US Dollar (#GotBitcoin?)

Binance Reveals ‘Venus’ — Its Own Project To Rival Facebook’s Libra (#GotBitcoin?)

The Real Benefits Of Blockchain Are Here. They’re Being Ignored (#GotBitcoin?)

CommBank Develops Blockchain Market To Boost Biodiversity (#GotBitcoin?)

SEC Approves Blockchain Tech Startup Securitize To Record Stock Transfers (#GotBitcoin?)

SegWit Creator Introduces New Language For Bitcoin Smart Contracts (#GotBitcoin?)

You Can Now Earn Bitcoin Rewards For Postmates Purchases (#GotBitcoin?)

Bitcoin Price ‘Will Struggle’ In Big Financial Crisis, Says Investor (#GotBitcoin?)

Fidelity Charitable Received Over $100M In Crypto Donations Since 2015 (#GotBitcoin?)

Would Blockchain Better Protect User Data Than FaceApp? Experts Answer (#GotBitcoin?)

Just The Existence Of Bitcoin Impacts Monetary Policy (#GotBitcoin?)

What Are The Biggest Alleged Crypto Heists And How Much Was Stolen? (#GotBitcoin?)

IRS To Cryptocurrency Owners: Come Clean, Or Else!

Coinbase Accidentally Saves Unencrypted Passwords Of 3,420 Customers (#GotBitcoin?)

Bitcoin Is A ‘Chaos Hedge, Or Schmuck Insurance‘ (#GotBitcoin?)

Bakkt Announces September 23 Launch Of Futures And Custody

Coinbase CEO: Institutions Depositing $200-400M Into Crypto Per Week (#GotBitcoin?)

Researchers Find Monero Mining Malware That Hides From Task Manager (#GotBitcoin?)

Crypto Dusting Attack Affects Nearly 300,000 Addresses (#GotBitcoin?)

A Case For Bitcoin As Recession Hedge In A Diversified Investment Portfolio (#GotBitcoin?)

SEC Guidance Gives Ammo To Lawsuit Claiming XRP Is Unregistered Security (#GotBitcoin?)

15 Countries To Develop Crypto Transaction Tracking System: Report (#GotBitcoin?)

US Department Of Commerce Offering 6-Figure Salary To Crypto Expert (#GotBitcoin?)

Mastercard Is Building A Team To Develop Crypto, Wallet Projects (#GotBitcoin?)

Canadian Bitcoin Educator Scams The Scammer And Donates Proceeds (#GotBitcoin?)

Amazon Wants To Build A Blockchain For Ads, New Job Listing Shows (#GotBitcoin?)

Shield Bitcoin Wallets From Theft Via Time Delay (#GotBitcoin?)

Blockstream Launches Bitcoin Mining Farm With Fidelity As Early Customer (#GotBitcoin?)

Commerzbank Tests Blockchain Machine To Machine Payments With Daimler (#GotBitcoin?)

Man Takes Bitcoin Miner Seller To Tribunal Over Electricity Bill And Wins (#GotBitcoin?)

Bitcoin’s Computing Power Sets Record As Over 100K New Miners Go Online (#GotBitcoin?)

Walmart Coin And Libra Perform Major Public Relations For Bitcoin (#GotBitcoin?)

Judge Says Buying Bitcoin Via Credit Card Not Necessarily A Cash Advance (#GotBitcoin?)

Poll: If You’re A Stockowner Or Crypto-Currency Holder. What Will You Do When The Recession Comes?

1 In 5 Crypto Holders Are Women, New Report Reveals (#GotBitcoin?)

Beating Bakkt, Ledgerx Is First To Launch ‘Physical’ Bitcoin Futures In Us (#GotBitcoin?)

Facebook Warns Investors That Libra Stablecoin May Never Launch (#GotBitcoin?)

Government Money Printing Is ‘Rocket Fuel’ For Bitcoin (#GotBitcoin?)

Bitcoin-Friendly Square Cash App Stock Price Up 56% In 2019 (#GotBitcoin?)

Safeway Shoppers Can Now Get Bitcoin Back As Change At 894 US Stores (#GotBitcoin?)

TD Ameritrade CEO: There’s ‘Heightened Interest Again’ With Bitcoin (#GotBitcoin?)

Venezuela Sets New Bitcoin Volume Record Thanks To 10,000,000% Inflation (#GotBitcoin?)

Newegg Adds Bitcoin Payment Option To 73 More Countries (#GotBitcoin?)

China’s Schizophrenic Relationship With Bitcoin (#GotBitcoin?)

More Companies Build Products Around Crypto Hardware Wallets (#GotBitcoin?)

Bakkt Is Scheduled To Start Testing Its Bitcoin Futures Contracts Today (#GotBitcoin?)

Bitcoin Network Now 8 Times More Powerful Than It Was At $20K Price (#GotBitcoin?)

Crypto Exchange BitMEX Under Investigation By CFTC: Bloomberg (#GotBitcoin?)

“Bitcoin An ‘Unstoppable Force,” Says US Congressman At Crypto Hearing (#GotBitcoin?)

Bitcoin Network Is Moving $3 Billion Daily, Up 210% Since April (#GotBitcoin?)

Cryptocurrency Startups Get Partial Green Light From Washington

Fundstrat’s Tom Lee: Bitcoin Pullback Is Healthy, Fewer Searches Аre Good (#GotBitcoin?)

Bitcoin Lightning Nodes Are Snatching Funds From Bad Actors (#GotBitcoin?)

The Provident Bank Now Offers Deposit Services For Crypto-Related Entities (#GotBitcoin?)

Bitcoin Could Help Stop News Censorship From Space (#GotBitcoin?)

US Sanctions On Iran Crypto Mining — Inevitable Or Impossible? (#GotBitcoin?)

US Lawmaker Reintroduces ‘Safe Harbor’ Crypto Tax Bill In Congress (#GotBitcoin?)

EU Central Bank Won’t Add Bitcoin To Reserves — Says It’s Not A Currency (#GotBitcoin?)

The Miami Dolphins Now Accept Bitcoin And Litecoin Crypt-Currency Payments (#GotBitcoin?)

Trump Bashes Bitcoin And Alt-Right Is Mad As Hell (#GotBitcoin?)

Goldman Sachs Ramps Up Development Of New Secret Crypto Project (#GotBitcoin?)

Blockchain And AI Bond, Explained (#GotBitcoin?)

Grayscale Bitcoin Trust Outperformed Indexes In First Half Of 2019 (#GotBitcoin?)

XRP Is The Worst Performing Major Crypto Of 2019 (GotBitcoin?)

Bitcoin Back Near $12K As BTC Shorters Lose $44 Million In One Morning (#GotBitcoin?)

As Deutsche Bank Axes 18K Jobs, Bitcoin Offers A ‘Plan ฿”: VanEck Exec (#GotBitcoin?)

Argentina Drives Global LocalBitcoins Volume To Highest Since November (#GotBitcoin?)

‘I Would Buy’ Bitcoin If Growth Continues — Investment Legend Mobius (#GotBitcoin?)

Lawmakers Push For New Bitcoin Rules (#GotBitcoin?)

Facebook’s Libra Is Bad For African Americans (#GotBitcoin?)

Crypto Firm Charity Announces Alliance To Support Feminine Health (#GotBitcoin?)

Canadian Startup Wants To Upgrade Millions Of ATMs To Sell Bitcoin (#GotBitcoin?)

Trump Says US ‘Should Match’ China’s Money Printing Game (#GotBitcoin?)

Casa Launches Lightning Node Mobile App For Bitcoin Newbies (#GotBitcoin?)

Bitcoin Rally Fuels Market In Crypto Derivatives (#GotBitcoin?)

World’s First Zero-Fiat ‘Bitcoin Bond’ Now Available On Bloomberg Terminal (#GotBitcoin?)

Buying Bitcoin Has Been Profitable 98.2% Of The Days Since Creation (#GotBitcoin?)

Another Crypto Exchange Receives License For Crypto Futures

From ‘Ponzi’ To ‘We’re Working On It’ — BIS Chief Reverses Stance On Crypto (#GotBitcoin?)

These Are The Cities Googling ‘Bitcoin’ As Interest Hits 17-Month High (#GotBitcoin?)

Venezuelan Explains How Bitcoin Saves His Family (#GotBitcoin?)

Quantum Computing Vs. Blockchain: Impact On Cryptography

This Fund Is Riding Bitcoin To Top (#GotBitcoin?)

Bitcoin’s Surge Leaves Smaller Digital Currencies In The Dust (#GotBitcoin?)

Bitcoin Exchange Hits $1 Trillion In Trading Volume (#GotBitcoin?)

Bitcoin Breaks $200 Billion Market Cap For The First Time In 17 Months (#GotBitcoin?)

You Can Now Make State Tax Payments In Bitcoin (#GotBitcoin?)

Religious Organizations Make Ideal Places To Mine Bitcoin (#GotBitcoin?)

Goldman Sacs And JP Morgan Chase Finally Concede To Crypto-Currencies (#GotBitcoin?)

Bitcoin Heading For Fifth Month Of Gains Despite Price Correction (#GotBitcoin?)

Breez Reveals Lightning-Powered Bitcoin Payments App For IPhone (#GotBitcoin?)

Big Four Auditing Firm PwC Releases Cryptocurrency Auditing Software (#GotBitcoin?)

Amazon-Owned Twitch Quietly Brings Back Bitcoin Payments (#GotBitcoin?)

JPMorgan Will Pilot ‘JPM Coin’ Stablecoin By End Of 2019: Report (#GotBitcoin?)

Is There A Big Short In Bitcoin? (#GotBitcoin?)

Coinbase Hit With Outage As Bitcoin Price Drops $1.8K In 15 Minutes

Samourai Wallet Releases Privacy-Enhancing CoinJoin Feature (#GotBitcoin?)

There Are Now More Than 5,000 Bitcoin ATMs Around The World (#GotBitcoin?)

You Can Now Get Bitcoin Rewards When Booking At Hotels.Com (#GotBitcoin?)

North America’s Largest Solar Bitcoin Mining Farm Coming To California (#GotBitcoin?)

Bitcoin On Track For Best Second Quarter Price Gain On Record (#GotBitcoin?)

Bitcoin Hash Rate Climbs To New Record High Boosting Network Security (#GotBitcoin?)

Bitcoin Exceeds 1Million Active Addresses While Coinbase Custodies $1.3B In Assets

Why Bitcoin’s Price Suddenly Surged Back $5K (#GotBitcoin?)

Zebpay Becomes First Exchange To Add Lightning Payments For All Users (#GotBitcoin?)

Coinbase’s New Customer Incentive: Interest Payments, With A Crypto Twist (#GotBitcoin?)

The Best Bitcoin Debit (Cashback) Cards Of 2019 (#GotBitcoin?)

Real Estate Brokerages Now Accepting Bitcoin (#GotBitcoin?)

Ernst & Young Introduces Tax Tool For Reporting Cryptocurrencies (#GotBitcoin?)

Recession Is Looming, or Not. Here’s How To Know (#GotBitcoin?)

How Will Bitcoin Behave During A Recession? (#GotBitcoin?)

Many U.S. Financial Officers Think a Recession Will Hit Next Year (#GotBitcoin?)

Definite Signs of An Imminent Recession (#GotBitcoin?)

What A Recession Could Mean for Women’s Unemployment (#GotBitcoin?)

Investors Run Out of Options As Bitcoin, Stocks, Bonds, Oil Cave To Recession Fears (#GotBitcoin?)

Goldman Is Looking To Reduce “Marcus” Lending Goal On Credit (Recession) Caution (#GotBitcoin?)

Your Questions And Comments Are Greatly Appreciated.

Paying Off Unfunded Pension,Paying Off Unfunded Pension,Paying Off Unfunded Pension,Paying Off Unfunded Pension,Paying Off Unfunded Pension,Paying Off Unfunded Pension,

Go back

Leave a Reply

You must be logged in to post a comment.