Ultimate Resource Covering Bitcoin’s Impact In Africa And The African-American Community

The issue of race when it comes to cryptocurrency is a sensitive one, and not without reason. Ultimate Resource Covering Bitcoin’s Impact In Africa And The African-American Community

The African-American community is largely born at an economic disadvantage, with a legacy financial system fueled by unethical practices like redlining, among many others. However, cryptocurrencies may give them the opportunity to eventually level the playing field.

Jack Dorsey, CEO of Twitter, is no stranger to controversy himself. His platform currently hosts 330 million people around the world, and his individual followers currently number just over 4.3 million. On Sunday, he used that influence to promote a new book discussing Bitcoin’s potential benefits to the African-American community.

Bitcoin & Black America, written by Isaiah Jackson, offers an analysis of the role cryptocurrency can play with African-Americans, a group historically underserved by major financial institutions. Yet, the author notes, black people in the U.S. have largely not utilized cryptocurrency to try and achieve financial autonomy.

The Perception Of Cryptocurrency Among African Americans Needs To Change

One of the problems, according to Jackson, is the perception of cryptocurrency among the African-American community. They are not the only ones to see Bitcoin as a scam, with new schemes continuing to exploit lack of regulatory oversight popping up in the news. Misinformation coupled with a lack of banking access has made investing in cryptocurrency a challenge among black people in the United States. Jackson says this must change going forward.

Originally published in July 2019, Bitcoin & Black America received a boost from the recent resurgence of the crypto market. Dorsey’s endorsement this week may do likewise.

Updated: 8-6-2019

Six Of The World’s 10 Fastest-Growing Economies Are In Africa

At a time when the United States, once a standard bearer of multilateralism, is embracing protectionism, Africa has taken a bold step in the opposite direction, creating the world’s largest free-trade area since the establishment of the World Trade Organization in 1995.

The African Continental Free Trade Area (AfCFTA), which came into force on May 30, includes nearly every country on the continent. And it proves, yet again, that Africa is on the move.

In recent years, Africans have been working to reclaim the narrative, highlighting their countries’ remarkable progress and the continent’s vast potential, in order to attract investment and deepen regional and global engagement. They have much to boast about.

In recent years, Africa’s average annual GDP growth has consistently outpaced the global average, and is expected to remain at least 6% until 2023.

Six of the world’s 10 fastest-growing economies are in Africa; for the period 2014-2050, PwC projects that Nigeria, South Africa, and Egypt will remain in the top 10.

Africa will owe much of this growth to its large working-age population and growing consumer markets. Throughout the twenty-first century, Africa – the youngest region in the world – will be the source of the vast majority of global labor-force growth.

This implies massive potential for increased production and savings, which could sustain an economic boom that supports rapid poverty reduction. In 2050, the richest 10% of Africans – some 250 million people – will drive as much as a five-fold increase in demand for consumer goods and services.

Of course, such outcomes are not guaranteed. If the continent is to reap the productivity and growth benefits of its growing workforce, its governments will need to ensure that people have the right knowledge, skills, and opportunities.

Fortunately, Africa’s governments are working to develop the required infrastructure and institutions. Across the continent, efforts are underway to improve education and foster a culture of innovation. Moreover, political leaders are implementing reforms aimed at improving business conditions.

In the World Bank’s 2019 Doing Business Index, five of the ten most-improved countries are in Africa, and one-third of all recorded reforms occurred in Sub-Saharan Africa.

Already, returns on investment and entrepreneurship are rising fast. Over 400 African companies now boast annual revenues of $1 billion or more, and 700 more report revenues of over $500 million.

An assessment of 360 companies from 32 African countries reveals an impressive average compound annual growth rate of 46% in 2019, up from 16% last year.

Lucrative investment opportunities are available in sectors like energy, agriculture, water, and mineral processing. Agriculture (including agribusiness), projected to be a $1 trillion industry in Sub-Saharan Africa by 2030, is attracting a growing amount of private-sector investment. Africa is also expected to receive almost $2 trillion in investment in natural resources by 2036.

But Africa’s economies are not seeking to cling to past growth strategies. Instead, the growth and revenues brought by investments in resources like oil will enable them to diversify – including by developing technology-enabled non-manufacturing industries, like information and communications technology-based services – and deepen regional integration.

Such integration was advanced last November at the African Development Bank’s inaugural Africa Investment Forum, where business and government leaders closed 49 deals worth over $38 billion.

It has now been accelerated by the AfCFTA, which promises to deliver major gains to all countries involved.

The AfCFTA could increase the value of intra-African trade by 15-25% by 2040, and boost economic output by $29 trillion by 2050. This would enable companies to take advantage of economies of scale, while supporting the diversification of industrial sectors and driving growth in manufacturing value added.

If governments create the right conditions, this could spur job creation and lead to significant poverty reduction.

African countries’ cross-border trade and investment ties are hardly confined to the continent. Trade with the advanced economies (particularly the European Union and the US) remains high, though it is declining.

Among the emerging economies, China has been particularly proactive in deepening its links with Africa, including by investing in the continent’s industrialization, agricultural modernization, and infrastructure.

With China projected to shift 100 million labor-intensive manufacturing jobs offshore by 2030 – jobs that Africa’s large and young workforce could easily fill – this relationship could be a game changer.

Africa has also pursued partnerships with emerging economies like India, Indonesia, Russia, and Turkey. This is broadly good news, though African governments must be aware of both the benefits and drawbacks of new trade deals and loan agreements with emerging economies, including China.

At the same time, policymakers must continue to foster a vibrant innovation culture, including by strengthening intellectual-property protections.

Innovations in mobile finance, such as Kenya’s M-Pesa, have already improved financial inclusion on the continent. Similar innovations can help countries to expand access to quality education, develop their human capital, and much more.

Africa’s political leaders, businesses, and citizens increasingly recognize that integrated economies, powered by innovative and high-growth companies and strong private investment, are the key to a prosperous future. Now, they must each do their part to drive progress on all of these fronts, including by continuing to embrace initiatives like the AfCFTA.

Updated: 3-23-2020

The Blockchain Africa Participants Optimistic About Continent Becoming Center of Progress

The Blockchain Africa conference produced a swathe of optimism for Africa to become a driving force behind the development and use of new blockchain-powered technologies.

Over the past few years, blockchain has replaced cryptocurrency as the “it” word in the fintech space. It is a fact that was mirrored by the Blockchain Africa conference itself, with speakers focusing more on the possibilities of blockchain answering a number of industry inefficiencies, and far less on cryptocurrency trading and tokenized solutions.

Africa has its own unique challenges in the global space given that many of its countries are trailing behind the rest of the world in infrastructure development.

While the asymmetric digital subscriber lines and fiber internet connectivity is still being rolled out in many countries, mobile tower services have driven the proliferation of mobile payments systems.

To say that Africans have taken to these services would be an understatement. The M-Pesa mobile payment service is a prime example that shows Africans can quickly adopt technologies that improve their day-to-day lives.

Mobile network provider Vodafone estimates that over 37 million people across seven African countries currently use M-Pesa, which was launched in 2007.

This is just one example of how people in Africa have benefitted from a future-forward solution to build a bridge to the people that are unbanked on the continent. In general, fintech solutions are being readily adopted and driven by African countries and companies.

As Cointelegraph reported in an event recap of the Blockchain Africa conference, blockchain technology is already being explored by trade finance, supply chain and self-sovereign identity sectors. Here are the main use cases that can be observed right now:

A Solution For Africa’s ID problems

The issue of Self-Sovereign Identity is a particularly interesting one in an African context, given the difficulty many people on the continent face when trying to obtain ID documentation. By way of definition, SSI refers to a situation where individuals hold and control their own identification credentials.

Victor Mapunda, CEO and founder of startup FlexFinTx, made a compelling case for a move to digital-based identities at the Blockchain Africa conference.

In his presentation, data quoted by Mapunda estimates that nearly 400 million Africans do not have proper identification credentials. This then leads to a multitude of difficulties, as these people are unable to open bank accounts, apply for insurance or other financial products.

Being banked and having insurance is a luxury when considering the deeper problems that are plaguing the continent. Referring to information supplied by the Mo Ibrahim Foundation, only eight African countries have birth registration systems that cover 90% of the population.

Countries like Chad and Tanzania are only able to cover 12% of births in the country. Conversely, Egypt, Mauritius and Seychelles are the only three African countries that register deaths covering more than 90% of their population.

The key takeaway is that there is a sizable gap in providing Africans with vital identification documentation, which is primarily due to institutional inefficiencies. Data capturing and information sharing is therefore impacted, leaving various institutions lacking in information, unable to serve the public needs efficiently.

Mapunda hails from Zimbabwe and began exploring the issue of SSI when he faced his own difficulties in trying to register a bank account after studying abroad. FlexFinTx seeks to provide people with a digital ID through WhatsApp, which facilitates the issuance of a FlexID that is cryptographically secured by the Algorand blockchain.

Users then have self-sovereign control over how their data is shared. Speaking to Cointelegraph after his presentation, Mapunda said that African people can quickly take to solutions that solve wide-ranging problems:

“I think Africans, when it comes to adoption of technology, are some of the most dynamic people in the world, this is because, for the most part, we don’t have a lot of legacy infrastructure and institutions. Most of the things we’ve grown up with didn’t work.”

Mapunda pointed to innovations such as mobile money and internet-based communication applications drastically improving Africans’ quality of life, saying, “Mobile money is a great example. We jumped on it,” and adding that no one even had to market it to the population. He went on to expand further:

“WhatsApp is a very good example of an application that didn’t have a single billboard, yet it managed to spread like wildfire across Africa. It solved a major problem — the cost of communication was too expensive and it’s a natural solution that people gravitate to.”

An Answer To Supply Chain Challenges

Blockchain technology has long been touted as a key tool in improving current supply chain systems across the world. In the past three years, major strides have been conducted in this regard, providing real use cases to back up the theory.

The subject was covered extensively at the Blockchain Africa conference and was particularly important considering the implementation of the African Continental Free Trade Area in May last year.

The move created a free-trade area that now includes 28 African countries, which requires member states to remove tariffs to provide the free trade of goods and services. While it improves the ease of trade, there are still some hurdles to clear in the trade finance and supply chain.

Thavash Govender, a data and AI specialist at Microsoft South Africa, spoke to Cointelegraph during the summit and said that blockchain technology could hold a number of benefits for trade across the continent:

“The one challenge that we have at the moment is trust between different countries. If I’m going to drop my trade barriers and say you can bring all your products into my country, I need to know that we aren’t allowing counterfeit goods in.”

Perhaps more importantly, Govender suggested that systems that are improved through the use of blockchain technology could drastically reduce the amount of time it takes for trade to take place due to inefficiencies in various processes, elaborating:

“If I’m an SME, I’m going to open up to a whole bunch of institutions that I just don’t know. If we’re all part of the same blockchain consortium, then I know I can trust what is written on the chain.

Because I can trust the information, I can move a lot quicker. It’s not going to take me weeks of investigation, so I can grant loans quicker or get the trade finance process going a lot faster.”

Public Procurement And Corruption

Another interesting implementation of blockchain technology is in the space of public procurement by government organizations. Corruption is not a uniquely African problem, but it is one that affects many countries on the continent.

Sope Williams-Elegbe, a professor and deputy director of the African Procurement Law Unit at Stellenbosch University, gave a presentation on the possibilities of blockchain addressing corruption in public procurement.

Williams-Elegbe said that 15%–22% of South Africa’s gross domestic product goes to public procurement. The problem is that the country loses 50% of this to corruption and fraud.

The professor believes that blockchain could be used to address procurement corruption but admitted that there are few to no use cases as of now. There is a lack of technical applications for public procurement, and it presents an opportunity for new solutions.

Forget The Hype, Build On Working Tech

Michelle Nsanzumuco, who acts as a senior advisor to the government of Bermuda and the Africa lead for Fintech4Good, spoke about a number of the sectors described above as being potential drivers of blockchain technology.

In an interview with Cointelegraph, Nsanzumuco highlighted supply chain and logistics as the key industry that can leverage blockchain due to the complexities of trade created by the sheer number of players in a value chain.

Nsanzumuco said that a number of entrepreneurs and SMEs that she has interacted with often complained about the difficulties they face when conducting trade inside their own country:

“They’re finding barriers just within their own countries because they’re dealing with so many different players, fill in so much documentation before they can even get their products from A to B. Now we haven’t even talked about cross-border transactions and trade. I can see it being a very strong use case for Africa specifically around supply chain and health care.”

Nsanzumuco added that blockchain solutions could improve the way health care systems track vaccinations and medications. Another factor is improving government services by digitizing a variety of manual data-capturing processes.

Additionally, while strongly agreeing that the continent could be a leader in the blockchain space, Nsanzumuco cautioned against touting “blockchain” tech because of its marketability:

“A big warning for me having traveled around the world is not getting caught up in the hype. Let’s leverage real solutions in particular sectors where it can have an impact in Africa.”

Updated: 5-6-2020

Why Binance And Akon Are Betting On Africa For Bitcoin Adoption

The future of money will be defined by African markets, where cryptocurrency awareness and usage surged dramatically over the past year.

Aspiring entrepreneurs like Ghanan high school student Emmanuella see bitcoin as a tool for international trade, not just speculation. He plans to buy some as soon as he turns 18 and can apply for a local mobile money account.

“I will use it to open up a business,” he said.

Ghanian exchange founder Nawaf Abd of eBitcoinics said local demand for bitcoin increased since the coronavirus crisis began, even though his physical stores in Accra and Kumasi are both closed. Through trading online, he continues to supply local buyers with bitcoin.

He said his sales were up 70% in March, so much that some days he sells out of bitcoin, but declined to say how many users that entailed. His servers briefly went down in April due to overwhelming traffic on the site.

According to researcher Matt Ahlborg, Ghanian volume at peer-to-peer exchanges LocalBitcoins and Paxful increased to roughly $6.2 million over 90 days of the lockdown, up from roughly $4.2 million the previous 90-day period.

Yet another Ghanan student, 18-year-old Derrick Bannerman, bought his first bitcoin during the last dip.

“I already had interest but the period seemed like the perfect moment to do something about my interest in bitcoins since we’re at home doing nothing,” Bannerman said from Accra. “The thing that interests me the most is its increasing value, popularity and security.”

And Nigerian bitcoin market activity is nearly 10 times Ghana’s. Ahlborg’s metrics showed roughly $63.9 million worth of Nigerian bitcoin trades during the lockdown.

CEO Yele Bademosi And CTO Taiwo Orilogbon Discuss Business At The Bundle Offices.

Sengelese-American hip-hop artist Akon is the latest celebrity to join the cryptocurrency industry, setting his sights on Africa.

He created a startup and corresponding foundation, both called Akoin, advised by Bancor co-founder Galia Benartzi, to issue a pan-African currency.

He’ll start in Senegal, where President Macky Sall gave the performer 2,000 acres of land to establish Akon City, and an industrial tech park in Kenya, Mwale Medical and Technology City (MMTC). The latter jurisdiction is expected to start using Akon’s cryptocurrency in the next few months.

“[Akoin] will be the primary digital payment solution and currency within the city … for all kinds of things that are city-related, like paying utility bills. They will ultimately pay employees in the hospital and the supermarket in Akoin,” said Akoin co-founder and Hollywood producer Jon Karas. “The government has asked people to go digital and not be using physical currency, overall, throughout the country.”

This Stellar-based token will launch within the next few months through a token sale aimed at raising $6.75 million. According to the project’s white paper, the sale represents 10% of the total token supply. Another 10% of the tokens will go to the founding team, plus an additional 5% will go to advisors.

“When it comes to growing vendor relationships in each country, we look at Dash in Venezuela as an example,” said Akoin co-founder Lynn Liss, an active promoter of token sales since 2016. She added government-endorsed Akoin systems will also offer civilians a stablecoin for “something relatable to savings.”

In Latin America, the Dash team has been criticized for overstating adoption metrics and marketing to vulnerable populations. There appears to be organic demand for cryptocurrency in Kenya, at least, with Ahlborg’s research indicating Paxful and LocalBitcoins traction in the country doubled over the past year to roughly $44 million worth of annual volume.

It remains to be seen which assets will gain traction across the continent, which includes a variety of jurisdictions with unique circumstances.

“We look for ways that we can help the people in Senegal, provide more tools, services to help the population, all the way to COVID-19 relief efforts we are currently looking at with the Senegalese government,” Karas said.

Regardless of their stance on any specific asset, all the above-mentioned entrepreneurs, across borders, agreed there’s an immeasurable opportunity to be found in Africa’s young and underserved populations.

“I got involved [with bitcoin] because I think it’s a currency of the future,” said Ghanaian student Albert Kwame Grant, who purchased his first cryptocurrency stash in April.

For example, Yele Bademosi, co-founder of the Binance-backed social payments startup Bundle, said thousands of Nigerians downloaded the Bundle app since it launched in late April.

There’s been some traction in Ghana as well, where Bademosi said the startup is looking to expand. But so far Nigerian demand is overwhelming enough. Roughly a 1,000 people signed up for an introductory Zoom webinar about bitcoin, he said, although there was only room for 100 to attend.

“It’s about making it easy to move value, regardless of whether it’s cash or crypto,” Bademosi said. “You can send [money] to any [smartphone] number in your contacts, even if they’re not on the app yet.”

For now, the app offers a fiat on-ramp to users with Nigerian bank accounts and supports bitcoin, ether, BNB, plus will soon support Binance’s dollar-denominated stablecoin BUSD.

“We have users who were interested in bitcoin but felt it was a little too difficult to get,” he said. “People use cryptocurrency as a remittance gateway as well as a hedge against any devaluations of local currency, plus speculative trading.”

And local entrepreneurs aren’t the only ones to notice the opportunity on the continent.

Updated: 5-15-2020

Cz Calls Africa An ‘Untapped Market’ With Unique Challenges For Crypto

Binance founder and CEO Changpeng Zhao, otherwise known as CZ, believes that the African continent holds some unique opportunities for cryptocurrency adoption and development.

The Binance leader provided a number of interesting insights during an exclusive “ask me anything” session hosted on Zoom for key members of the African cryptocurrency community, which Cointelegraph participated in.

Binance, which has established itself as the world’s largest cryptocurrency exchange by trade volume, has slowly been opening up satellite trading platforms in a number of African countries. Uganda was the first country to welcome Binance to the continent in 2018.

Binance has since launched trading support in countries such as Nigeria and most recently South Africa, which included the provision of trading pairs and fiat deposits for users using South African rands. The company’s foray into the African continent began in earnest in 2018, as CZ explained during the AMA.

“Even from the first day when Binance launched, we had users from Africa, and they were actually relatively active. So, we’ve always known that Africa is an important market. And so, I think it was early 2018 that I visited Uganda, Togo, Nigeria at the same time — and also Ethiopia. So, I had a little tour around Africa just to learn a little bit more about the market, and soon after that we opened Binance Uganda.”

The past two years have seen Binance branch out into a number of African countries, while its charity arms and incubation services have supported start-ups and made donations to the needy. CZ believes that the continent will become another vital cog in the company’s ever-growing base.

“We view the entire African market as a really key market, and this year we were very lucky to be able to find a good banking partner in South Africa, and we are able to now accept banking deposits directly through bank accounts. […] We will soon be able to launch credit card buying as well. South Africa, and Africa as a whole, is a really important market for us.”

Africa Is Untapped, But Not Without Challenges

As previously covered during the 2020 Blockchain Africa conference hosted in Johannesburg earlier this year, the continent is ripe for technological innovations that could provide solutions to the huge number of unbanked people.

Cointelegraph posed its own question to CZ during the Zoom session, asking if the Binance CEO sees Africa as a relatively untapped market for cryptocurrency exchanges.

Despite the fact that South Africa has a number of local cryptocurrency exchanges that are operating successfully, CZ believes that the rest of the continent could benefit from cryptocurrency exchanges:

“Yes, absolutely. I think that in South Africa there’s a few crypto exchanges — they’re doing quite well. But I believe they are still relatively small. I’m not sure how profitable they are or how sustainable they are. In other parts of Africa, I think the coverage is very weak, is very poor. I don’t think it’s very easy to buy cryptocurrencies in Africa right now overall, so we want to help improve that situation.”

Despite the fact that Binance is rolling out peer-to-peer platforms and its own centralized exchange platforms in certain countries, there is still a lot of room for growth.

CZ pointed to the fact that the provision of trading pairs in native fiat currencies is gaining traction in countries such as Nigeria where daily trading volumes have surpassed $1 million per day on Binance.com.

Nevertheless, the sheer number of Africans that are unbanked remains a major barrier to entry, as does basic Know Your Customer processes being carried out due to varying socioeconomic difficulties facing many Africans:

“It is a very much untapped market. There’s a different set of challenges there. I think basically, that’s the reason for it being untapped. Working with banks there is a little bit more difficult. The banking API interfaces are slightly older or nonexistent, and the number of people having bank accounts are quite low. So, even if you have a bank account support, the overall population you can tap into [is] still in the low double digits.”

CZ went on to add that even the most basic things like verifying users have proven to be challenging in some cases: “Many people in Africa does not have Western-style addresses. […] For exchanges that tap into this market, they have to address all of those issues. So, we’re trying to overcome all of those issues.”

Fiat On-Ramping Is A Key Driver Of Adoption

Another key takeaway from the AMA with CZ was the importance of fiat deposits bringing new cryptocurrency users into the ecosystem. This could become even more important as the world tries to grapple with the effects of the ongoing coronavirus pandemic.

As the founder of Binance explained, the world will have to adapt to new ways of working post- COVID-19, and that could have a profoundly positive effect on the adoption and use of cryptocurrencies:

“I think in the post-COVID-19 world, things will be more digital. They will be more online, more virtual. […] Right now, everyone’s staying home. People are buying things online. You can buy them using fiat currencies, or you can buy them across the world using cryptocurrencies. So, I think the future world, post-COVID-19, is a world that — I think it’s gonna be really great for cryptocurrencies.”

CZ pointed to a number of secondary and tertiary effects of the ongoing pandemic. A major consideration has been the need for fiscal stimulus from a number of central banks, in the form of newly minted fiat currency.

At the same time, Bitcoin has just carried out its third-ever halving event, which saw the block reward from mining halved from 12.5 BTC to 6.25 BTC. CZ believes that both situations will have a positive effect on the cryptocurrency ecosystem as a whole:

“There is a lot of fiat money being printed, while we’ve just gone through the Bitcoin halving. So, the new supply of Bitcoin is actually very limited, and the fiat money is being printed in record quantities now. So, I think the cost of everything will increase very soon. We will see hyperinflation. All of those things are actually really good for cryptocurrencies and for the overall blockchain business.”

That is where providing a proverbial on-ramp for non-crypto users will become a crucial cog in driving the adoption and proliferation of cryptocurrency use in Africa and around the world. The Binance founder wants to create the pathway for that to happen:

“I believe that creating, providing liquidity is […] gonna be a key role, a key feature that people require. […] Imagine a world with thousands or tens of thousands of cryptocurrencies you will have to exchange when you cross from one currency to another. So, I think crypto exchanges will play an increasingly important role in that new world. […] Payments, other things could come later, but right now […] our focus is really just building the bridges so people can enter the crypto space. So, those are the fiat gateways that we’re working really hard to build.”

Updated: 5-20-2020

Africa Is Bullish on Crypto Despite Infrastructure and Regulatory Hurdles

According to a new report, African nations have the highest rates of cryptocurrency adoption throughout the world.

A new report published by Arcane Research shows that African countries have some of the highest cryptocurrency ownership rates worldwide.

South Africa ranked third throughout the world with 13% of its internet users owning or using cryptocurrencies. Nigeria took the fifth spot with 11% of internet users owning cryptocurrencies. The worldwide average for the same stands at 7%.

Indeed, as Cointelegraph recently reported, Bitcoin (BTC) trading volume in Sub-Saharan Africa broke past records posted at the heights of 2017’s rally.

Clear Interest In Bitcoin

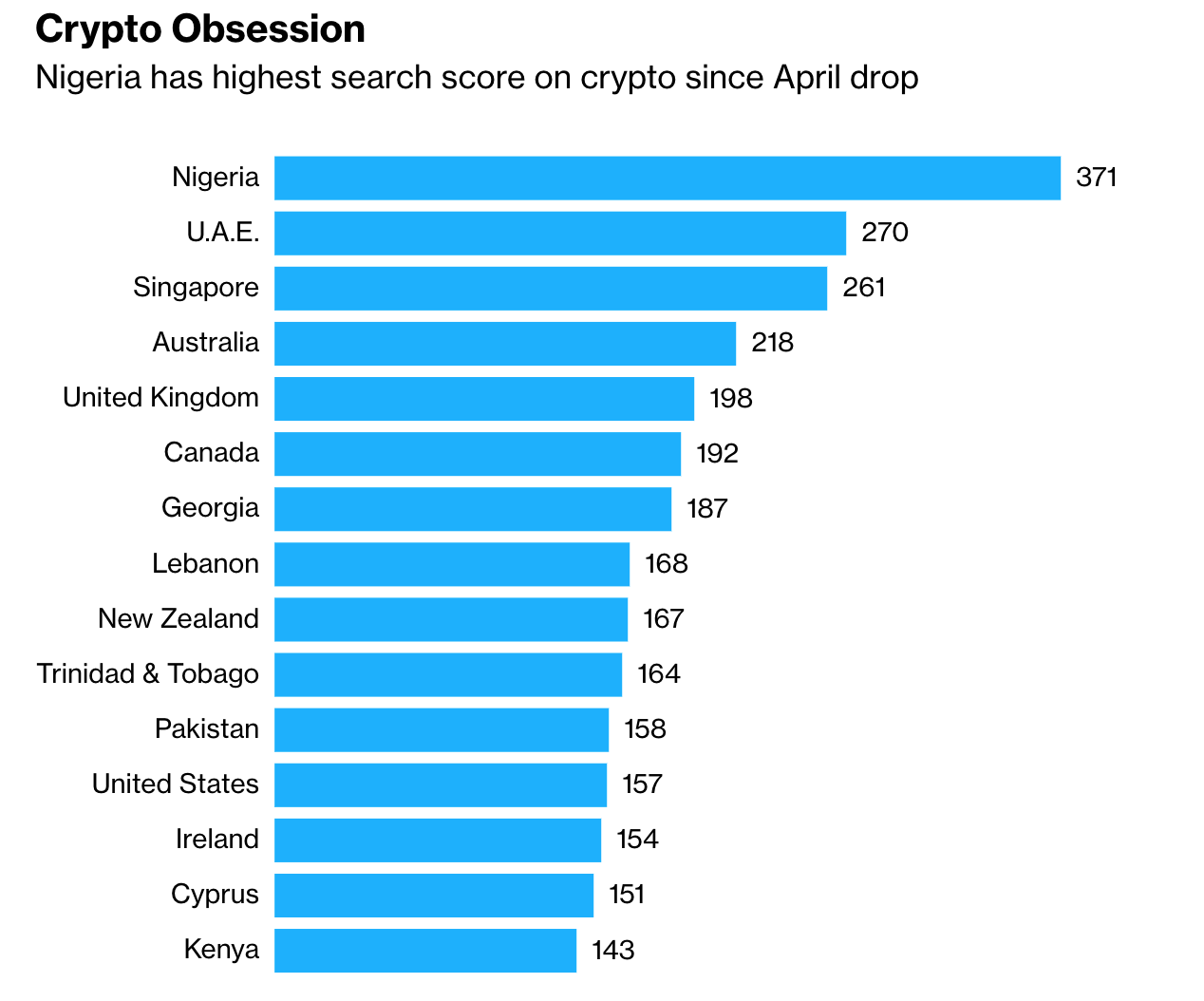

Arcane Research noted that Uganda, Nigeria, South Africa, Kenya and Ghana feature in the top-10 countries searching for the term “cryptocurrency” on Google.

Sub-Saharan Africa also has a huge remittance market that brings in about $48 billion annually. Expats today rely on slow and centralized remittance systems that charge transaction fees as high as 9%. Even mobile payment alternatives charge a fee of around 11%.

These factors along with high inflation rates in some African nations reflect the extreme need for cryptocurrency alternatives within the continent.

But There Are Obstacles

However, the report notes a significant lack of related infrastructures such as crypto mining operations, supporting merchants, smartphone penetration, and internet connectivity. These are obstructing wider reach and utility of cryptocurrencies among Africans.

Additionally, there’s little to no clarification from governments regarding cryptocurrency regulation in African countries. Almost 60% of African governments, the report states, are yet to clarify their stance on cryptocurrencies, which is causing a drag on the adoption of digital currencies.

The fact that African citizens are relying on crypto assets despite the lack of proper infrastructure and regulatory clarity is a testament to the wide room for cryptocurrency adoption across the continent.

Many major players in the cryptocurrency industry are already entering African markets. In a recent “ask me anything” session, the founder of world-leading cryptocurrency exchange Binance, Changpeng Zhao, said that Africa is an untapped market for cryptos, and the exchange was working on offering its services on the continent.

Updated: 5-22-2020

African P2P Volume Beats Out Latin America For First Time

African peer-to-peer Bitcoin trade has generated more than $14.6 million in weekly volume, comprising a new record for the continent.

African peer-to-peer, or P2P, Bitcoin (BTC) trading volumes have continued to increase, with the continent posting its third-consecutive all-time high for trade activity.

Africa’s surging volumes come amid a plateauing in global P2P trade, with Latin America, Asia Pacific, and Western Europe posting significant declines in post-halving volume.

As such, this past week saw African P2P trade overtake Latin America to rank as the second-strongest region by weekly volume for the first week on record.

Africa’s P2P Markets See Prolonged Volume Spike

More than $14.6 million worth of Bitcoins changed hands between African users of P2P crypto marketplaces Localbitcoins and Paxful this past week.

The week’s volume beat out the continent’s previous record of $11.6 million from last week, and the nearly $10 million traded at the start of the month.

Trade between the Nigerian naira and BTC represents two-thirds of the continent’s P2P trade, with $9.5 million worth of BTC changing hands in Nigeria in one week.

North American trade also increased in volume this week, extending the continent’s dominance with $25.4 million.

Only Africa And Asia See Annual Increase In P2P Trade

Comparing P2P volumes over 365-day intervals shows only Africa and Asia to have made gains in yearly trade activity.

Sub Saharan Africa ranks as the fifth-strongest region by volume, trailing behind North America, Eastern Europe, Latin America, and Asia Pacific.

North American generates over $1 billion in P2P Bitcoin trade each year.

Updated: 5-24-2020

Africa Is Experiencing A Crypto Renaissance

Crypto adoption appears to be growing across the continent of Africa.

Crypto adoption is making significant advances in Africa, with crypto ownership, trade volume, and regulation all moving toward greater adoption.

A recent report by Arcane Research and Luno found that Uganda, Nigeria, South Africa, Ghana, and Kenya are frequently among the top 10 countries by Google searches for the word “Bitcoin.”

The report describes the continent as “one of, if not the most promising region for the adoption of cryptocurrencies,” emphasizing Africa’s combination of low existing crypto adoption alongside an “enormous” domain possibility.

The firms emphasize that Africa exhibits a young population, frequent monetary crises and currency failures, large unbanked or underbanked populations, and expensive means of payment.

South Africa Emerges As Crypto Hub

While Nigeria has long dominated the continent’s trade volume, the report found that South Africa has the highest percent of cryptocurrency ownership or use among internet users in Africa with 13%, followed by Nigeria with 11%.

Worldwide, South Africa ranks fifth for crypto adoption among connected citizens.

This past week saw South Africa post its second-strongest weekly volume on peer-to-peer Bitcoin (BTC) marketplace Localbitcoins, with nearly $1.65 million worth of BTC changing hands.

The surge in trade activity saw total P2P volume for South African trade edge out Kenya last week with $1.95 million in trade across Localbitcoins and Paxful.

Last month, South Africa’s financial regulator issued a policy document asserting that crypto assets and activities relating to virtual currencies “can no longer remain outside of the regulatory perimeter.”

P2P Volumes Surge Across Africa

Nigerian P2P trade is rallying to record highs, producing $9.2 million in combined weekly trade.

Kenyan trade has also seen a recent spike, with Localbitcoins trade between BTC and the Kenyan shilling producing its second-strongest week on record for the third consecutive time.

Morocco and Egypt have also posted record trade activity in recent weeks.

The increase in volume across the continent has also seen P2P volume from Sub Saharan Africa beat out Latin America for the first time.

Updated: 5-25-2020

Africa Is Experiencing A Crypto Renaissance

Crypto adoption appears to be growing across the continent of Africa.

Crypto adoption is making significant advances in Africa, with crypto ownership, trade volume, and regulation all moving toward greater adoption.

A recent report by Arcane Research and Luno found that Uganda, Nigeria, South Africa, Ghana, and Kenya are frequently among the top 10 countries by Google searches for the word “Bitcoin.”

The report describes the continent as “one of, if not the most promising region for the adoption of cryptocurrencies,” emphasizing Africa’s combination of low existing crypto adoption alongside an “enormous” domain possibility.

The firms emphasize that Africa exhibits a young population, frequent monetary crises and currency failures, large unbanked or underbanked populations, and expensive means of payment.

South Africa Emerges As Bitcoin Hub

While Nigeria has long dominated the continent’s trade volume, the report found that South Africa has the highest percent of cryptocurrency ownership or use among internet users in Africa with 13%, followed by Nigeria with 11%.

Worldwide, South Africa ranks fifth for crypto adoption among connected citizens.

This past week saw South Africa post its second-strongest weekly volume on peer-to-peer Bitcoin (BTC) marketplace Localbitcoins, with nearly $1.65 million worth of BTC changing hands.

The surge in trade activity saw total P2P volume for South African trade edge out Kenya last week with $1.95 million in trade across Localbitcoins and Paxful.

Last month, South Africa’s financial regulator issued a policy document asserting that crypto assets and activities relating to virtual currencies “can no longer remain outside of the regulatory perimeter.”

P2P Volumes Surge Across Africa

Nigerian P2P trade is rallying to record highs, producing $9.2 million in combined weekly trade.

Kenyan trade has also seen a recent spike, with Localbitcoins trade between BTC and the Kenyan shilling producing its second-strongest week on record for the third consecutive time.

Morocco and Egypt have also posted record trade activity in recent weeks.

The increase in volume across the continent has also seen P2P volume from Sub Saharan Africa beat out Latin America for the first time.

Updated: 5-25-2020

Why Africa Is The New Crucible Of Crypto

Twitter’s Jack Dorsey calls Africa the future of Bitcoin. Local startup founders agree; is the continent set to play host to “Crypto Valley”?

Just like the explorers of a bygone age, Jack Dorsey came away entranced when he visited Africa for the first time last year. The Twitter and Square CEO is a big Bitcoin fan and investor—and during his visit, he declared that the continent was the future of Bitcoin.

Atsu Davoh, founder of Ghana-based cross-border transaction app Bitsika, was one of those Dorsey sought out during his recent visit there. “He was humble and very curious,” Davoh said.

And Dorsey is coming back, with other investors in his wake, because Africa is compelling, see—and especially so for crypto. The continent’s very specific challenges and its enthusiastic workforce are the key ingredients cryptocurrencies like Bitcoin need to succeed.

Fragmented infrastructure means that Africans pay the highest remittance costs in the world, and are the second highest unbanked population, but these could prove to be opportunities in the right hands. Does Africa have the potential to lead the way on blockchain adoption?

How Is Crypto And Blockchain Adoption Progressing In Africa?

Ray Youssef certainly thinks so. The CEO of peer-to-peer Bitcoin marketplace Paxful, Youssef credits the continent with teaching him about Bitcoin’s true use cases. “Africans have had peer-to-peer financial systems in place for thousands of years,” he said.

Approximately 45% of Paxful’s three million subscriptions are from Africa. Sending money in traditional ways is so onerous for many that it’s easier to get on a plane and deliver it yourself, said Youssef.

Cryptocurrencies are used as a store of value, for speculation and, increasingly, as a medium for borderless trade across countries, said Philip Agyei Asare, CEO of remittance platform, BTCGhana, which was founded in 2015.

“African crypto is like the Wild West, there are no legal hurdles or regulations,” said Bitsaka’s Davoh. “Governments don’t know that much about crypto so they let people do whatever they want to do.”

He claims to know someone who processed $30 million in Bitcoin over-the-counter transactions in one year. Nigeria has a big population and the best programmers, but is also more politically unstable than Ghana, he added.

National Digital Currencies, Stablecoins And Schools

Africa’s major economies, South Africa, Nigeria and Kenya, are all keeping an eye on cryptocurrency. Ghana and South Africa are also among those exploring the potential of national digital currencies.

Among the continent’s more liberal crypto states is Senegal, where rapper Akon has started constructing the world’s first “crypto city.”

But the project has come under fire. Improving education is a more pressing need, many believe.

“The greatest national resources in Africa are above the ground, not below it,” said Paxful’s Youssef. “It’s the people—so driven, so ambitious, and just looking for a way to make a difference.”

In 2017, Paxful began a push to build 100 schools with Bitcoin.

African Projects To Meet African Needs

Africa’s unique qualities make it ideally suited as a giant sandbox for blockchain and crypto development—from blockchain commodity exchanges in Nigeria, to boosting agricultural yields and establishing land rights in Kenya. Cardano is prominent among blockchain platforms working with African governments to address local needs, and training developers.

“Africa missed the first, second and third industrial revolutions, but we have a real opportunity to be a part of the Fourth Industrial Revolution,” said Bitange Ndemo, who heads Kenya’s Blockchain and AI Taskforce.

The so-called “Leapfrogging” theory holds that it’s now irrelevant that Africa failed to develop current-generation IT infrastructure because next-generation services—5G, AI and the Internet of Things—can now be built without having to worry about the costs of overhauling legacy infrastructure.

In Kenya, birthplace of the M-Pesa, the digital revolution is transforming everyday life, paving the way for the application of emerging technologies like blockchain. Kenya’s startup scene is thriving, and the government is working on a trusted identity platform, and exploring biometrics for transaction verification.

Much of Africa’s digital revolution is due to the explosion in mobile phones, now commonplace even in the continent’s poorest countries. Close to 10 percent of GDP in transactions are made with mobile money—the highest proportion in the world.

UK blockchain platform Electroneum is tapping into this trend, and has also teamed up with an NGO to create “a crypto ETN village” in an as-yet-undisclosed location, a spokesperson told Decrypt.

Africa is also on the cutting edge of crypto innovation; Many believe 2020 could be the continent’s year of the stablecoin.

Bitsika is currently developing its own ABCD stablecoin, and Nigerian Bitcoin exchange NairaEx is also working on one backed by the national currency, the Naira.

Africa: A Big Place

In a continent comprised of 54 countries and and 1.2 billion people, there’s plenty of disparity in how technology is used, something that also applies to blockchain and crypto.

Take the M-Pesa. Touted as digital currency for the entire continent, its success in Kenya wasn’t replicated in South Africa, and there’s no definitive answer as to why.

There’s also a huge disparity between Cape Town, South Africa, where you can now buy a pad near the city’s university complex with bitcoin, and Zambia, where cryptocurrency is illegal.

But what Africa’s countries have in common is that across the continent, startup founders have grown up in an era of digital transformation—mobile, YouTube and the M-Pesa. That makes the continent a perfect crucible for the next wave of innovation, in crypto and blockchain.

“Jack said the future of crypto is in Africa, and I totally agree,” said Davoh. “If you just look at the freedom we have here, the talent and the attention we’re getting from outside—and the role and purpose these solutions serve—this is the perfect place. When I look at all the exciting companies being built here, I think that very, very soon, we’ll see a crypto valley happening in Africa.”

Updated: 6-7-2020

Opportunities For Blockchain-Based Technologies In African Healthcare

Emerging technologies such as blockchain can dramatically improve the situation with the healthcare industry in Africa by its implementation.

One of the linchpins of the internet is the ability to access and share data seamlessly. Whether it’s financial metrics for an institution or something as innocuous as a meme, the internet’s distinct pathways of protocols and standardization are the ideal medium for exchanging information.

That transmissibility of information has not translated well to specific industries, however.

Regulatory moats, cumbersome and outdated database architecture, and poorly designed user interfaces are a hindrance to major industries — particularly healthcare.

Even in the United States, where healthcare standards are high, onerous regulatory processes inhibit the ability of doctors to adequately share patient information across state lines or access sensitive medical data from past care providers.

If there’s a silver lining to COVID-19, it’s that it has induced a long-overdue examination of many archaic aspects of the healthcare system. When we apply these lessons to emerging markets, such as Africa, the horizon for change coming out of the crisis looks promising.

Africa’s Healthcare Problems Are Opportunities

The maxim that “every problem is an opportunity in disguise” applies aptly to the COVID-19 pandemic and the overall healthcare situation in Africa — COVID-19 aside. For context, Africa’s healthcare system is overburdened, lacks adequate resources and does not have a unified approach to its myriad endemic diseases ranging from Malaria to HIV/AIDS and Ebola.

World organizations such as the United Nations have taken an active role in bolstering the healthcare system in Africa for decades, but the progress is slow and lacks technological innovation.

For example, African countries are making meaningful strides in preventing childhood diseases, with 60% or more children now immunized for measles — largely the effort of nonprofits and the United Nations.

On the contrary, public-private healthcare partnerships remain sparse on the continent (especially with foreign companies), yet they represent the greatest opportunity for bringing cutting-edge technologies to African medical facilities. In many cases, these technologies can be as simple as mobile diagnosis tools and more developed IT infrastructure.

The problem isn’t a lack of third-party donations and assistance to the African healthcare system. The same problem that, in many cases, hinders innovative tinkering in the developed world — adequate data sharing.

For example, telehealth was disparaged by many medical professionals in the U.S. before COVID-19. Now, however, it appears that telehealth is here to stay. Some of the early concerns with telehealth (i.e., telemedicine) are well-founded, though.

The Health Insurance Portability and Accountability Act standards for privacy and security of patient medical data are embedded into hospital practices and procedures, severely limiting the amount of data that can be shared between medical institutions without cumbersome processes.

In addition, many major healthcare institutions in the U.S. rely on disparate IT systems, including non-congruent databases for storing and indexing patient data.

This has profound consequences on data sharing in the medical community.

Some medical providers may even be unwilling to share data for fear of not being able to control who else the data is doled out to from the initial party offered access.

In other cases, the incentive for big data modeling using artificial intelligence is reduced, since it requires unobstructed access to sensitive clinical data by a technology company — further restricting the internet’s capacity to mold medicine for the better.

As a consequence, some medical professionals and institutions are exploring blockchain technology and its concomitant class of developments to tackle the data sharing barrier. And it’s implications present an enormous opportunity for Africa.

Africa’s healthcare infrastructure is not as mature as in developed countries like the U.S., but that may be an advantage.

For example, an African medical initiative to build hospitals, research enterprises and other organizations imbued with blockchain tech like secure multi-party computation and reduced regulatory overhead could unleash the floodgates for medical innovation.

In theory, African medical facilities could leapfrog many of the bottlenecks facing Western medical institutions that stem from their entrenched policies and aversion to sharing medical data without myriad regulatory processes.

Blockchains are ideal for the secure sharing of sensitive data, and can even be imbued with advanced privacy-preserving primitives like zk-SNARKS to further obscure sensitive medical data.

While Africa’s limited medical infrastructure may have formerly proven an obstacle, when paired with dynamically growing technologies in the blockchain arena, it can catapult to a competitive landscape of innovation.

The continent is even showing signs of early success in combating COVID-19, largely drawing from its experience with Ebola.

Surveillance has been scaled up rapidly, and face masks and other personal protective equipment are commonplace. A South African team even designed a mesh-network COVID-19 tracing app that preserves privacy — a notable departure from the combined efforts of Apple and Google in the U.S.

Injecting Africa’s experience with data-sharing technology like blockchains would only further bolster the continent’s ability to stifle pandemics in their infancy.

Imagine the scale of intrigue by foreign scientists, AI firms and medical professionals into Africa’s myriad novel diseases and pathogens should the real potential of the internet’s data-sharing capabilities be realized on the world’s fastest-growing and most geographically diverse continent.

Data on unique diseases plaguing Africans, such as river blindness, could be seamlessly and securely shared between hospitals, clinics and researchers — enabling real-time improvements in decision-making.

Mobile diagnoses could be uploaded to shared blockchain networks in real time, cryptographically secured, and passed on to third-parties with read-access restrictions baked into the patient data. No need to worry about a Facebook Cambridge Analytica scandal at the medical level in the African sub-Saharan region.

Capital investment would subsequently pour into a region where the regulatory shackles are removed, and technology can flourish independently of government mandates. Interestingly, reduced regulatory overhead may be a direct consequence of COVID-19 as we take measure of our failures to respond to the pandemic.

If Africa pursues the fusion of low regulatory burdens and blockchain-based healthcare IT systems, the consequence may have an endemic positive impact.

Africa, and the world, needs more nimble technology for disease monitoring, diagnosing and treatment in the field. The current systems have proven inadequate in the fight against COVID-19, and it’s clearly time for some deep introspection.

Africa is a fertile hotbed for exploring the potential of new technologies in the healthcare sector.

But Africans remain firmly skeptical of third-party interference in its healthcare system as well. A murky history of the World Health Organization using Africans for experimental vaccine treatments has eroded trust in foreign aid, and even led to novel strain outbreaks of diseases like Polio, which have been linked to a mutation in a strain of a vaccine.

That’s why a more self-sufficient African healthcare system is the ultimate goal, and one that blockchains can help realize.

That’s a promising vision for bypassing many of the bottlenecks facing the medical industry in the West, which has languished in red tape for decades. For a global medical landscape looking to reshape after a colossal disaster, the incentive for letting go of outmoded healthcare solutions and embracing more agile, connected yet less invasive models has never been greater.

Updated: 6-16-2020

One Man’s Mission to Deploy Solar-Powered Bitcoin Nodes Across Africa

Africa appears to have eight nodes total. From this map, entrepreneur and IT guru Chimezie Chuta inferred that he is the only person in Nigeria known to be running a Lightning node.

A crucial caveat is that many users might be running nodes without exposing them to the world. But, all told, Lightning activity looks sparse on the planet’s second-largest and second-most populous continent.

Chuta wants to change this. Like many Bitcoiners, he believes running a network node is one of the best ways to become truly financially independent. A Lightning node in particular, while experimental and maybe risky to use, allows Africans to earn a little cash by way of fees for relaying money across the network, he said.

To that end, BlockSpace Technologies Africa Inc., Chuta’s company, has released a kit for a Bitcoin and Lightning node, including all the hardware pieces for assembly, called SpaceBox, in the hopes of expanding the technology’s use across the continent.

“I think this will help many people living in low-income regions of the world to become part of the Bitcoin ecosystem. Beyond trading and speculation, Africa seems to have zero representation,” Chuta said.

Many Africans don’t have access to financial services like traditional bank accounts. In 2015, the World Bank estimated that 350 million people living in Sub-Saharan Africa were “unbanked.”

In theory, running the pair of nodes could connect Africans to a more modern financial system – and do so in a way that gives them greater visibility and control over their funds than relying on third parties.

The SpaceBox sells for 210,000 naira, the Nigerian currency, worth roughly $541. The main component of the kit is a tiny hobbyist computer called the Raspberry Pi running the open-source Raspblitz software for Lightning nodes. It also has a solar panel component, since many Africans lack electricity.

“Our goal is to raise an army of full Bitcoin Lightning node operators to dot every nook and cranny of the continent in the next one year,” Chuta said. “We plan to sell and deploy at least 250 of these nodes … in the next six months.”

So far, over the last month the company has received seven orders, one from British Columbia, five from Nigeria, and one from Ghana.

Financial Sovereignty

Some readers may feel deja vu. Half a decade ago, Africa was touted as fertile ground for cryptocurrency adoption. Back then, cheaper remittances were supposedly the killer app.

Compliance costs, along with bitcoin’s scaling challenges, complicated that narrative. While some people, including in Nigeria, indeed use bitcoin for remittances today, it hardly put a dent in Western Union.

Chuta’s pitch is different, emphasizing the autonomy that comes with running a full Bitcoin node, and the income from a Lightning one. It’s a way to earn and safeguard money, not just zap it to someone else.

Operating a Bitcoin full node basically means running the underlying infrastructure for the world’s largest cryptocurrency by market capitalization. Unlike mining, which requires significant investment in specialized chips, electricity and cooling, anyone can run a node on a laptop with enough space.

At least 10,000 people are running nodes today – a conservative estimate since not all nodes show the world they are running.

While there’s no direct financial reward for running a Bitcoin node, it has an advantage over both custodial services (where a third party holds the private keys) and simplified payment verification wallets (which verify only their own transactions).

A full node “self-validates” by retrieving every transaction recorded on the blockchain. With this information and the node rules downloaded, users can verify firsthand that transactions follow the network rules.

As the ultimate bullshit detector, it can tell if you’re getting false data.

“Being financially sovereign has become a necessity and Bitcoin offers the primary tool to attain that,” Chuta said.

SpaceBox’s Lightning node component is built on top of the Bitcoin node. Lightning attempts to solve one of Bitcoin’s biggest problems: increasing scalability so more people can use the network at once.

If successful, it might become the main method of making everyday payments in the cryptocurrency – and generate revenue for those running nodes.

“Although operating a full Bitcoin Lightning node is more like a hobbyist engagement, some people are already making some money by positioning their nodes as [a] Lightning payment routing channel,” Chuta said.

Solar-Powered

There are several options for building Lightning nodes, such as RaspiBlitz, or just purchasing them already put together from vendors like myNode.

Most node makers assume that users will have a stable electric source to plug into, which isn’t a safe assumption in Sub-Saharan Africa where, according to The World Bank, more than one half of the population lacks electricity.

“With regards to infrastructure, Nigeria (and a number of other African countries) have very poor electricity supply so keeping a full node running is very difficult,” Bitcoin Core contributor Tim Akinbo told CoinDesk.

Hence the solar panel that comes with the SpaceBox kit.

“This lack of regular electricity has denied most bitcoin enthusiasts in the continent the opportunity to participate in the global bitcoin multi-billion dollar industry as miners or routing node operators,” Chuta said. “By integrating [an] affordable solar power kit into bitcoin node operation, we expect that many more people across the world, especially Africans, can participate.”

Beyond electricity, Akinbo notes there are other costs to running a full node. They require a lot of storage space, for instance.

“It’s just untenable for most Africans at the moment,” Akinbo said, arguing that only wealthy bitcoins in Africa could afford a node.

But in Chuta’s vision, not everyone will necessarily run a node themselves. Perhaps there will be specialists that learn to run them, he said, who then pass the benefits on to their local community.

“The main point of this project … is to educate and train capable node operators across Africa, who then can help their small communities maintain ‘friends and family node’ in order to secure a healthy financial future for them,” Chuta said.

He hopes orders will snowball after the coronavirus fades, since the pandemic has hurt BlockSpace’s hardware suppliers.

“As soon as COVID-19 issues settle, we will launch a full campaign that will make a significant impact based on our vision,” Chuta said.

Updated: 7-1-2020

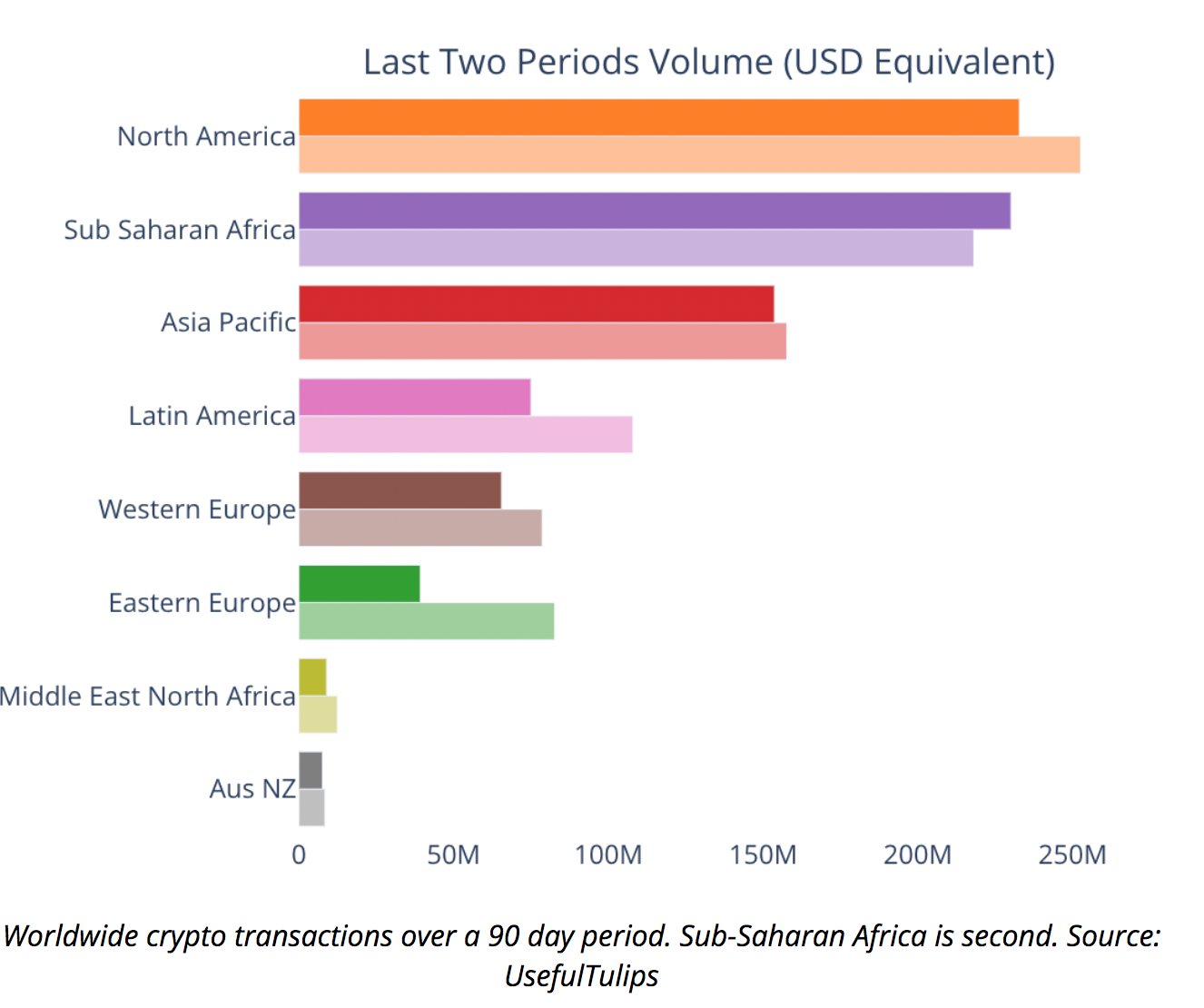

Africa Posts Triple-Digit P2P Volume Gains In Three Months

Sub-saharan Africa now represents more than $15 million in combined weekly peer-to-peer trade following triple-digit growth over just a few months.

Peer-to-peer Bitcoin (BTC) trading has seen rapid growth in recent months, with the African continent now the second-strongest region in the world for P2P volume behind the U.S.

Africa was the sole region to produce an increase in seven-day P2P trade this past week — with sub-saharan African trade posting its seventh all-time high for weekly trade in nine weeks.

Since early January, the sub-saharan African has overtaken the Asia-Pacific, Eastern European, and Latin American regions to emerge as the second-strongest P2P market by a volume margin of more than 50%.

African P2P Trade Surges

Data posted to Twitter by crypto analyst Kevin Rooke on June 30 indicated triple-digit P2P activity among Africa’s top P2P markets over just three months, with volume increases of 125% in Nigeria, 194% in South Africa, 199% in Kenya, and 257% in Ghana.

Speaking to Cointelegraph, a spokesperson for top P2P Bitcoin marketplace Paxful noted that in addition to Africa’s top markets, Cameroon has emerged as a “breakout country” with $5 million in volume during 2020 so far.

Paxful attributes the dramatic increase in trade activity to its ethos of staying “connected to the streets” and fostering grassroots communities in developing markets:

“There’s no one catalyst for the recent significant jump in volume, rather it’s a result of a collective effort on the part of our various teams who have enabled us to successfully enter new markets like India and Argentina, build local communities (in Kenya, Ghana, South Africa, etc.) and form new partnerships.”

“With every new market comes an opportunity to improve and we plan to continue to focus on our users’ needs as a roadmap for growth,” Paxful added.

US Dominates P2P Volume

Despite Africa’s meteoric rise, North America has further consolidated its lead in P2P volume with recent all-time highs for weekly trade exceeding $30 million.

The United States represented $30 million in trade by itself this past week, comprising nearly twice that of the entire continent of Africa. Paxful’s spokesperson noted that California is the strongest U.S. state for P2P trade year-to-date.

Nigeria is the second-strongest national P2P market, representing almost $10 million in weekly trade.

Updated: 8-3-2020

Where FATF Crypto Compliance Gets Interesting: Africa

Africa isn’t included on the virtual asset regulatory map just yet.

But crypto businesses seeing strong growth across the 54-country continent are working hard on know-your-customer (KYC) rules to meet the exacting standards set out by the Financial Action Task Force (FATF).

A broad range of entities operating in Africa, ranging from crypto exchanges to remittance providers to peer-to-peer marketplaces, are exploring KYC options, which could mean picking up licenses from other jurisdictions or even creating new regulatory frameworks in some cases.

The FATF makes reference to jurisdictions with “weak or non-existent” anti-money laundering (AML) and counter-terrorist financing (CTF) controls in its recently published summer plenary report.

If a so-called stablecoin provider were located in a jurisdiction with poor AML/CTF controls, other jurisdictions could apply their stronger AML/CTF laws to these providers, says the FATF report.

But enforcement of any rules might be difficult if the home supervisor of the virtual asset services provider (VASP) had not implemented the revised FATF standards strongly enough to respond to international co-operation requests, the report continues.

Nonetheless, innovative crypto players in Africa and other parts of the unregulated world are doing their best to be AML-compliant with a view toward meeting the requirements of the Travel Rule. The Travel Rule mandates that the senders and receivers of crypto transactions over $1,000 on regulated exchanges must be identified.

Shopping For Regs

“In places where there aren’t really e-regulatory rules yet, firms are doing KYC and using blockchain analytics for AML,” said former Kenya resident Pelle Braendgaard, CEO of crypto identity startup Notabene. “People are shopping around for regulation, looking at remittance licenses to deal with foreign partners so they can have at least some level of clarity.”

This was the approach taken by BitPesa, launched in Kenya in 2013. The cryptocurrency payments and liquidity platform, which rebranded as AZA last year, snagged a license from the U.K.’s Financial Conduct Authority (FCA) in 2015, then acquired money transfer company TransferZero in 2018, gaining a license from the Spanish central bank.

When AZA expanded into Nigeria, it helped the Nigerian central bank address the dearth of crypto regulation, taking part in a government DLT task force, said Stephany Zoo, AZA’s head of marketing.

“Our AML and KYC are of U.K. and European standards, which means we are asking for things that nobody else on the African continent is asking for,” said Zoo, adding:

“We have a number of automated AML and KYC platforms that are integrated into ours, but when you don’t have the same kind of access to government databases, it becomes much harder to run these checks. So, unfortunately, we do have to use a combination of automated and manual systems.”

AZA also recently became the first company to get a digital remittances license in Uganda, which involved some hands-on effort.

“We basically lobbied the central bank for three years and finally they created a license for us,” Zoo said. “In Africa, that’s what you kind of have to do, you have to work with the government very closely because these regulations don’t exist, so you have to create them.”

Collecting remittance licenses is one approach; formulating an entire regulatory framework is another. That’s what Cryptobaraza CEO Michael Kimani is attempting to do with the Blockchain Association of Kenya.

Kimani counts South African crypto exchange Luno among the association’s backers, and says members would like to move the regulatory process forward on their own steam, rather than wait for state-led supervision to emerge.

He also expects guidance on this project from the likes of FATF and the International Monetary Fund (IMF).

“We are creating our own virtual currency guidelines and we are hoping to submit about 15 regulations,” said Kimani. “One of the reasons I’m trying to push this, as the chairman of the association, is because I feel it’s important we cater to local peculiarities and don’t just end up adopting some laws that may have been customized for a completely different market.”

Africa is a complex and varied market. Its many local nuances mean Western companies can experience epic failures, such as BebaPay, Google’s bank-backed attempt at travel cards.

Even M-pesa, the Vodafone-backed mobile-phone money with a monopoly in Kenya, failed miserably in South Africa, where some 75% of the population have bank accounts.

There’s also a lesson here for Facebook and the proposed cryptocurrency libra, says Kimani: “I think the challenge is, no one wants to see a foreign company come in here and just dominate the payments scene.”

P2P Pump

African countries with more advanced banking and financial infrastructure such as Nigeria are beginning to see impressive growth in crypto, not only in remittances but around investing and trading, said Ruth Iselema, CEO and co-founder of crypto exchange Bitmama.

“There’s not much in the way of government rules,” said Iselema, “but we can KYC users with Nigeria’s BVN [bank verification number]. It’s like a social security number, but not everyone has one. Or you can use an international passport when you have higher transaction limits.”

But exchange-based trading in Africa is only part of the picture, as Cryptobaraza’s Kimani points out. Peer-to-peer (P2P) marketplaces are growing fast across the continent. This type of crypto adoption between so-called “unhosted wallets” occupies the other end of the regulatory spectrum from the FATF’s VASP regime.

“The best way to mitigate the ML/TF [money laundering/terrorist financing] risks posed by such disintermediated transactions remains an area of focus and will be considered in further detail by the FATF as part of its ongoing work on virtual assets,” states the FATF plenary report.

There are, in fact, two types of P2P markets in Africa, said Kimani. The first includes the likes of LocalBitcoins and Paxful. But there’s another whole system of informal networks based on trust and reputation. Pockets of trading using Telegram and WhatsApp are also very popular, said Kimani, who has acted as an escrow agent to such trust networks.

“This happened before crypto with PayPal, Skrill and Neteller,” said Kimani. “People feel comfortable knowing they are dealing with someone they trust. A lot of crypto conversations are fixated on AML, but I think crypto could learn a lot from how these trust networks operate.”

The Paxful Challenge

Meanwhile, P2P marketplace Paxful, which is now experiencing explosive growth in Africa, has taken on an inordinate KYC challenge across the region.

Paxful CEO Ray Youssef explained his company is building a localized KYC “switchboard,” in rather the same way Paxful itself has evolved into a universal switchboard for money.

“It’s a big job, believe me; it’s like a whole other startup,” said Youssef. “For example, Nigeria has five different types of national ID, most of them don’t have an expiry date. In Kenya, there’s no such thing as proof of address. If someone has an ID from a little country like Malawi, for example, we are routing KYC requests to one of the very few appropriate KYC providers. Sadly, most KYC providers have left Africa behind.”

A large slice of Paxful’s business in places like Nigeria involves the trading of gift cards (Amazon, Apple, etc.) for bitcoin. These gift cards are sold for bitcoin at between 60 cents and 80 cents on the dollar, which critics flag up as inherently scammy.

Some of the business is fraudulent, as Paxful will admit.

“We have made 99.5% of gift card transactions safe, which is a monumental achievement,” said Youssef. “LocalBitcoins dropped gift cards because they don’t have the capability to support this. But we haven’t abandoned gift cards, and they are most challenging. Why? Because they are a key route to onboarding the emerging world.”

There appears to be a vibrant system of gift card remittance (many gift cards are purchased by expat Nigerians in the U.S., who immediately send pictures of the cards, plus receipts back to relatives who then trade for bitcoin).

Indeed, gift cards are even described as a kind of “stablecoin” to the Paxful ecosystem; this is not so different from the hack where Kenyans started selling mobile-phone minutes, which ultimately led to M-pesa.

Youssef said gift card trading, plus the creation of a bitcoin trade route between Nigeria and China, have paved the way for a crypto gold rush in Africa. He also thinks P2P is going to be front and center.

“P2P is how the world works,” said Youssef. “Dare I say it – and I do – in two years time, P2P volume will flippen exchange volume, which is vastly inflated. They’ve got some surprises coming from the people of Africa.”

Updated: 8-12-2020

Championing Blockchain Education In Africa: Women Leading The Bitcoin Cause

“Women need to be financially independent. This is the biggest weapon they can use to liberate themselves. When they no longer depend on anyone, they can then reach their full potential.”

It’s no secret that women are underrepresented in the technology and financial industries. In the U.S, women only hold a quarter of computing-related jobs. Some sectors, like software engineering, fare even worse, with female representation as low as 15%.

And now along comes blockchain, a technology that promises a global revolution through decentralization. Blockchain has already begun to transform many industries, from finance and supply chain management to healthcare and governance.

However, it has yet to significantly change the demographics of the tech industry.

According to a study conducted by Long Hash, a cryptocurrency research firm, women only represent 14.5% of blockchain startup team members. At the management level, the number is even lower, with women only accounting for 7% of executives and 8% of advisors.

Africa Paints A Different Picture

In Africa, the story has been quite different. The continent has greatly taken to blockchain technology and cryptocurrencies, and women have been playing a key role. Despite the tech industry traditionally being a ‘boys’ club,’ a rapidly growing number of fearless, dedicated and determined women have taken the industry by storm, rising to various positions of power and influence.

In Africa, women have faced marginalization for centuries. Economic exclusion, lack of access to education, gender-based violence, limited participation in political decisions – these are just a few of the many challenges that the continent’s women face.

This has been one of the reasons Bitcoin, and the underlying blockchain technology, have appealed to many women. For them, blockchain promises freedom. The technology gives them hope that they can break free from the shackles of financial captivity by the legacy systems, decades of corruption, lack of opportunities and more.

For example, in Botswana Alakanani Itireleng has been on the frontline in preaching the blockchain gospel. Known as ‘The Bitcoin Lady,’ she is the founder of Satoshicentre, a blockchain hub which works with several developers to use blockchain to solve Africa’s biggest challenges.

In South Africa, Sonya Kuhnel has continued to be one of the most renowned leaders in the blockchain space. Kuhnel is the founder of Xago, an XRP cryptocurrency exchange and payment gateway that allows retailers to accept XRP payments.

She is also the founder of The Blockchain Academy, an institution committed to up-skilling 10,000 software engineers on blockchain technology by 2022.

In Kenya, Roselyn Gicira leads blockchain innovation and adoption, serving as the chairperson of the Blockchain Association of Kenya. Gicira also leads the Kenya Women in Blockchain Chapter which seeks to ensure that more women get into the blockchain industry.

And in Nigeria, Doris Ojuedeire’s efforts to promote blockchain have gone beyond her home country, reaching out to women across the continent and bringing them into blockchain and cryptocurrencies. She shared her journey with me, one that has seen her rise to become one of Africa’s most influential blockchain voices.

Of Scams And Triumphs

Doris got into cryptocurrencies when she was studying accounting in university, eight years ago. At the time, crypto was a niche field that few in Africa were involved with — most of them men. This didn’t faze Doris, and she sought all the materials she could find to learn more about Bitcoin and other upcoming cryptocurrencies.

She started off by investing in crypto trading. As a novice, Doris lost a lot of money initially through online scams. However, she battled on, and in time she started making profits from crypto trading. The venture proved to be quite fruitful for her, giving her financial independence while still at the university.

It was when she graduated that she discovered there was much more to Bitcoin than just making profits. As she learned about blockchain technology, she realized that it had the potential to transform lives for millions of Africans, especially the continent’s women. It was then that she decided to embark on educating the masses about blockchain, a passion that still drives her today.

Blockchain Africa Ladies

In Africa, Bitcoin had become synonymous with scams after several investors lost millions of dollars to Ponzi schemes. This was the first thing Doris set out to change, educating thousands of Nigerians about Bitcoin and the world of opportunities it opens up.

She realized that women were vastly underrepresented in Bitcoin and blockchain. She set out to change this, eventually leading to the birth of Blockchain African Ladies (BAL).

BAL is a non-profit organization that educates African women on blockchain technology. The organization has grown rapidly and now has members in Kenya, Cameroon, Nigeria, South Africa, Ghana, Egypt, Cote d’Ivoire and many other countries.

BAL organizes meet-ups, workshops, mentorship programs and conferences for the women, geared towards sparking an interest in blockchain.

Its biggest event is the Blocktech Women Conference, an event that attracts some of the foremost leaders in blockchain to inspire, educate and interact with the women. Unlike most blockchain events that have only a few female speakers, 80% of the speakers at Blocktech are women.

Doris Has Gone Beyond Education, Though. She Told Me:

“While blockchain can help eradicate, or at least reduce, many of the challenges that African women go through, teaching them about it isn’t enough. The women need to be financially independent. This is the biggest weapon they can use to liberate themselves. When they no longer depend on anyone, they can then reach their full potential.”

Her desire to make African women financially stable led to the founding of Crypto Lioness, a platform she uses to educate women about crypto trading.

Crypto Lioness allows the women to connect via WhatsApp, Telegram and other social media platforms to learn the do’s and don’ts of crypto trading, share tips, learn from experts and support each other.

Women In Blockchain

Through Doris’ efforts, thousands of women in Africa have joined the blockchain industry. This is her greatest accomplishment, she tells me. She believes that this will be a catalyst for widespread adoption of the technology and cryptocurrencies across the continent.