Ultimate Resource On Central Bank Digital Currencies (#GotBitcoin)

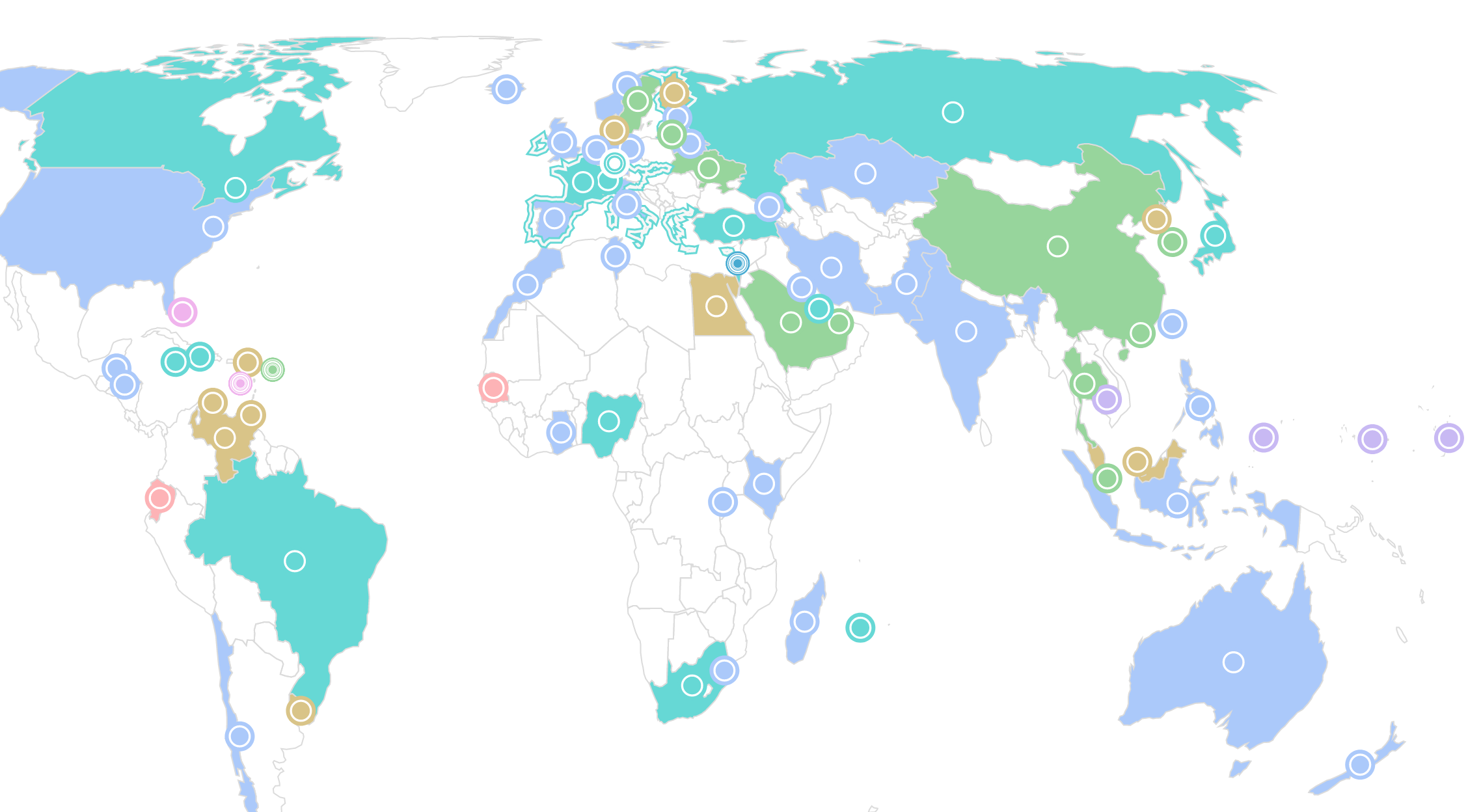

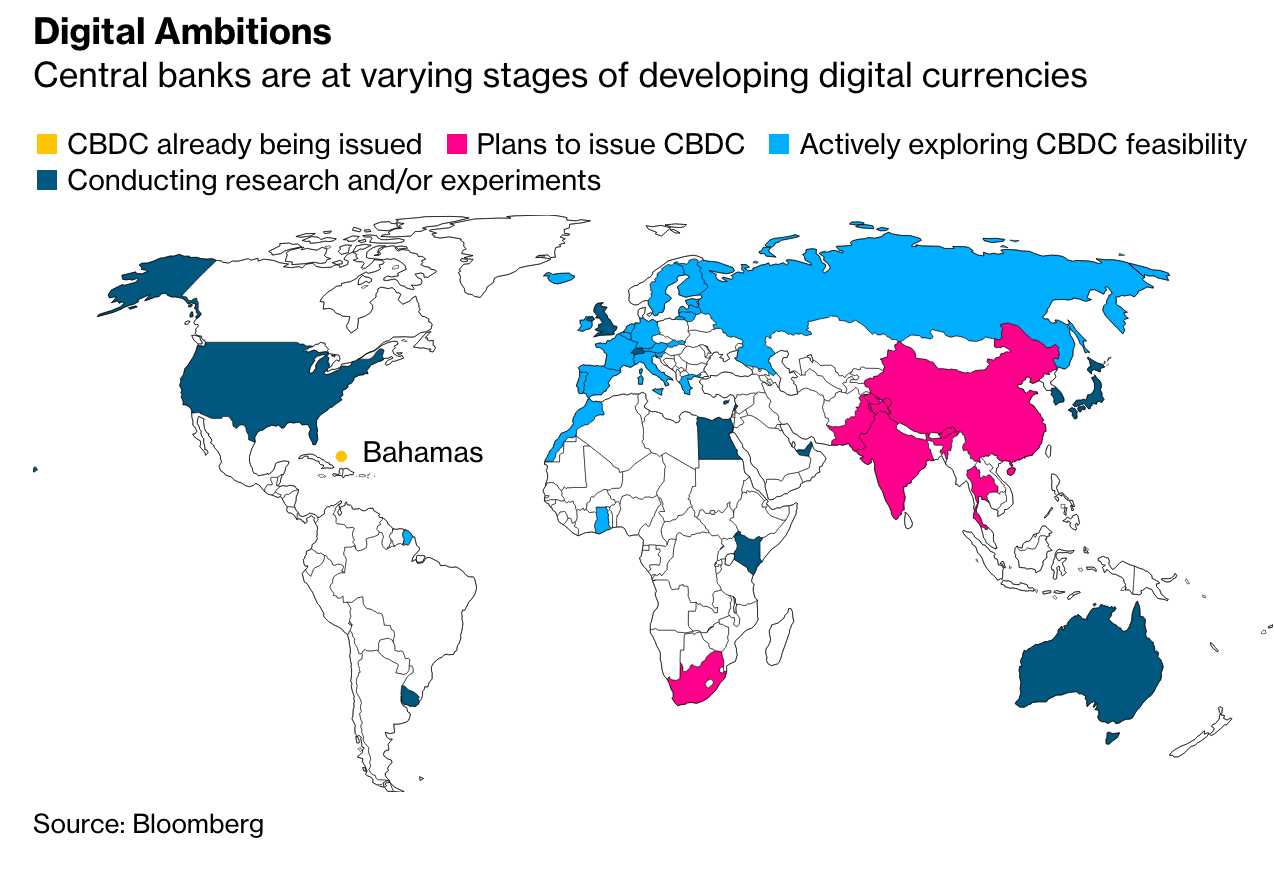

Eight out of 10 central banks surveyed says it is likely to roll out digital currencies within three years. There has been immense scrutiny on the Federal Reserve and central banks around the world over the last 18 months. Ultimate Resource On Central Bank Digital Currencies (#GotBitcoin)

Everyone from investors to business owners to retirees are trying to figure out what the central banks will do with interest rates and asset purchases, so they can better prepare their portfolios for the future.

It is easy to get lost in the day-to-day drama of what the central banks are going to do. Every mainstream media outlet is talking about the various scenarios. Investing forums and Twitter users are speculating on the color of the Fed Chairman’s tie or whether he uses the word “dovish” or not. Some analysts even spend time trying to measure correlations between the length of press conferences and future interest rate decisions.

It has become absolute madness. The financial world, and various related aspects of society, all patiently wait for the decisions of a small group of 12 people who emerge from the FOMC meetings. There are other people in the room during the meetings, but ultimately 12 people are deciding what will happen to trillions of dollars in assets and billions of people. (here is a 2016 FOMC meeting as an example)

It doesn’t have to be this way though. The elites who make up the minority don’t have to be the ones to make the decisions. In fact, I would argue that the world would be better off if humans weren’t in charge of making these decisions at all.

We know that human decision-making is flawed. We are emotional animals. We have bias. There is academic study after academic study that shows how humans are experts at poor judgement.

So What Does That Have To Do With Central Banks?

Central banks are supposed to have two core components to them — independence and predictability. José Manuel González-Páramo, a member of the Executive Board of the European Central Bank from 2004 – 2012, gave a speech in June 2007 titled “Inflation Targeting, Central Bank Independence and Transparency.” In that speech, he stated the following:

“Indeed, the principle of central bank independence in the pursuit of the goals of monetary policy has been codified in the legal systems of many countries. Perhaps even more importantly, there is evidence that the importance of this principle seems to be increasingly well understood by society at large.

According to all surveys among euro area citizens, an overwhelming majority of respondents support the pursuit of price stability as a goal of the European Central Bank (ECB) and back the ECB’s independence in order to guarantee the achievement of this goal….

…But I am not here to talk about politics. Indeed, one of the great advantages of central bank independence is precisely that we can ignore the political furor and concentrate on the welfare-enhancing objective of keeping inflation under control. At the same time, I could not agree more with the view that central bankers must strive to fully comply with the standards of transparency and accountability that democratic societies rightly demand from independent public agencies.”

Central Bank Independence Is Absolutely Crucial. Additionally, Jose Went On To Say The Following About A Central Bank’s Predictability:

“Going back to the subject of expectations, I have thus far focused on inflation expectations. Before concluding, however, I should like to mention another type of expectation which is of interest to central banks, namely expectations regarding future monetary policy rates. Such expectations provide benchmarks against which to assess various aspects of crucial importance for a central bank’s success, such as its transparency, its predictability, and the effectiveness of its communication strategy, among others.

As a result, expectations regarding future policy rates, whether taken from surveys or financial market data, are an essential source of information for assessing the degree of understanding of a central bank’s monetary policy strategy and conduct by market participants and external observers.”

These are the words from central bankers themselves — the independence and predictability of a central bank are essential to the organization’s effectiveness.

This Brings Me To A New Type Of Central Bank That Has Been Created. It Is Fully Automated, Completely Independent, And The Most Predictable Organization In The World. What Do I Mean?

A pseudonymous person or group created an automated central bank a little over a decade ago. They ensured that no one person or organization would ever own it or control it. The central bank is decentralized, which gives it complete independence.

This person or group also made sure to write the monetary policy for the central bank into software code and then ensured that no one would be able to change it unilaterally. As if that wasn’t enough, the creator(s) of this digital central bank also open-sourced everything so that it could be audited by anyone, at any time, from anywhere.

This digital central bank structure allows for the most independent and most predictable central bank in the world. In a sense, you can think of this new creation as an automated central bank that is superior to the human-led central banks that have existed for the last few decades.

So What Is This New Central Bank? Bitcoin.

Bitcoin is completely decentralized. It has a programmatic monetary policy. No one owns the network and no one controls it. The system is fully transparent and anyone can audit it. The monetary policy is written into software so you know every future monetary policy decision for the next century. Bitcoin is the most independent and most transparent central bank in the world.

As people begin to understand how this automated central bank works, they will slowly decide to start storing their economic value and personal wealth in the independent and predictable system. This difference is being highlighted even more recently with the undisciplined and variable decision-making that is happening.

Eventually the world won’t hang on every word of a press conference. We won’t rely on 12 people in a room making decisions for billions of people. The system will be more democratic. It will be more accessible. And ultimately, it will lead to a more prosperous world.

Independent. Predictable. Bitcoin

More than one-fifth of the world’s population could have access to digital money issued by central banks to pay for groceries, movie tickets and even homes in the next few years, as these institutions accelerate plans to issue official cryptocurrencies.

???????????? “One of the major central banks in the world will collapse in 2021. The central banks are leveraged at 50, 60, 70-to-1.

They’re leveraged more than Long Term Capital Management was at its highest point of leverage.”-@MaxKeiser

One in 10 central banks surveyed in 2019 said it was likely to offer digital currencies within the next three years, covering about 20% of the world’s population, according to a report from the Bank for International Settlements. The proportion of central banks likely to issue digital money almost doubled when the horizon was stretched to six years, the BIS said.

Federal Reserve Chairman Jerome Powell said in November the U.S. central bank doesn’t currently have plans to launch a digital currency. Doing so would be difficult in the U.S., with Americans remaining more committed to cash than other nations, he said.

The rising popularity of electronic payments, and the boom in private cryptocurrencies like bitcoin, has promoted authorities to pay more attention to digital currencies. The new tools could offer faster settlements of payments and the potential to allow people to bank directly with a central bank.

They may even offer monetary-policy benefits, if central banks could set rates on accounts that directly affect households, rather than using financial markets to transmit changes to borrowing costs for consumer and corporate loans.

Major technology companies, meanwhile, are interested in offering digital currencies. But Facebook Inc.’s plans to launch libra have drawn criticism from regulators and have led early partners to reconsider their support.

Central banks face big hurdles in offering dedicated digital currencies and related bank accounts to the general public, the BIS’s general manager, Agustín Carstens, said in December. Still, policy makers in the Caribbean, including the Central Bank of the Bahamas and the Eastern Caribbean Central Bank, are testing digital money, according to the BIS.

Some 66 central banks, representing 90% of the world’s economic output, took part in the survey in 2019, according to Switzerland-based BIS, which is owned by some of the world’s biggest central banks, including the Fed. A year earlier, only one in 20 monetary authorities were considering rolling out digital money in the short term.

In response to the rapid decline in the use of cash in recent years, Sweden’s Riksbank began working on its e-krona pilot program in 2017. Uruguay’s central bank, which piloted a program between late-2017 and mid-2018 that let individual users hold a maximum of 30,000 e-Pesos ($1,000) in a digital wallet, is considering its next steps.

Central banks in general have been hesitant about creating digital currencies, according to Darrell Duffie, a finance professor at Stanford University. Questions remain on how to monitor transactions to prevent fraud and whether such currencies would be linked to interest rates.

“It’s a responsibility I think central banks don’t want,” Mr. Duffie said.

Updated: 6-5-2020

Fed Paper: Central Bank Digital Currencies Could Replace Commercial Banks – But At A Cost

Central bank digital currencies might one day replace commercial banks. But that comes with risks, according to new research from the Federal Reserve of Philadelphia.

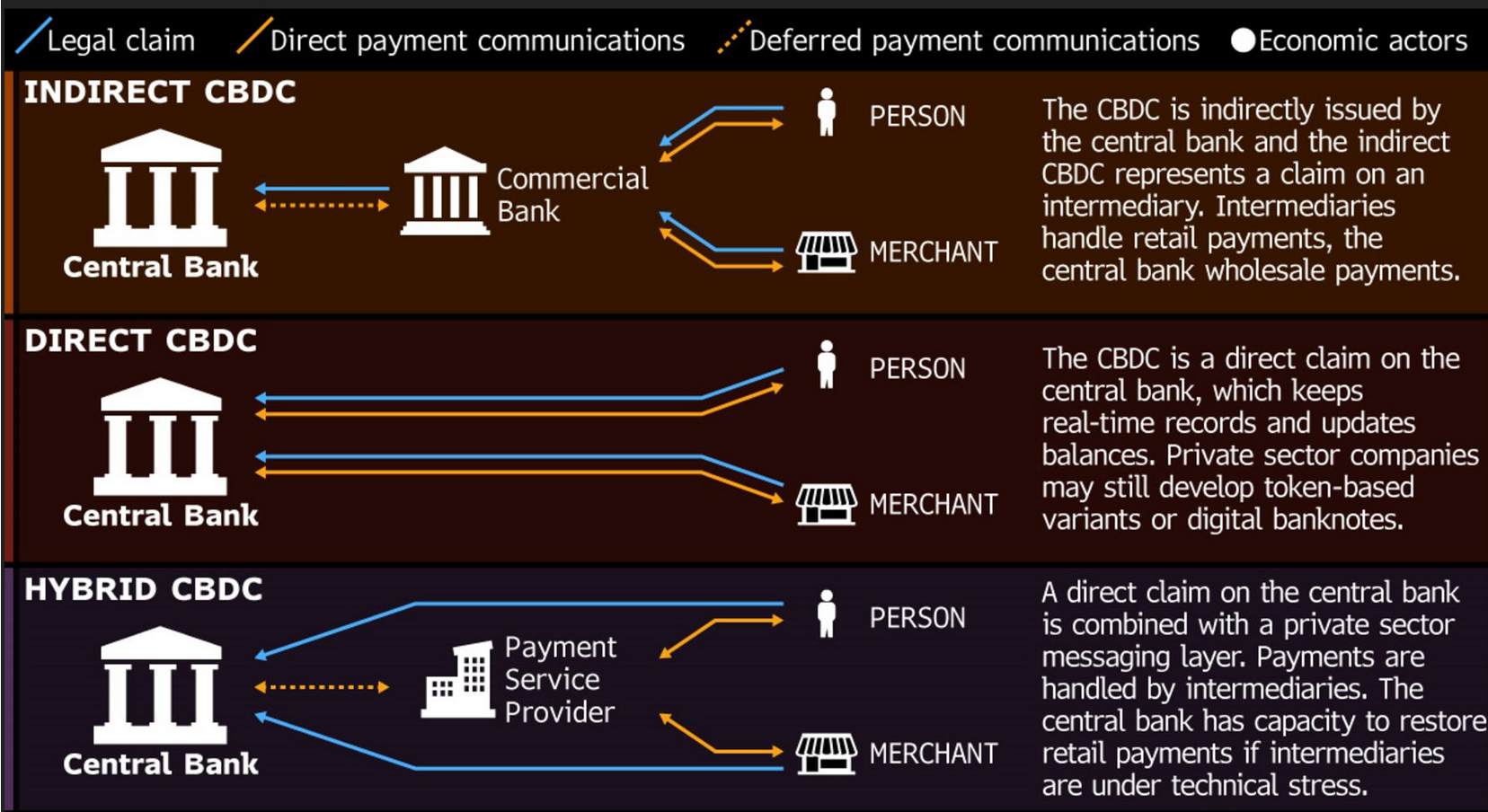

The 32-page research paper – titled “Central Bank Digital Currency: Central Banking for All?” – investigated the implications of an account-based central bank digital currency (CBDC), focusing on its potential competition with the traditional maturity transformation role of commercial banks.

“The introduction of digital currencies may justify a fundamental shift in the architecture of a financial system, a central bank ‘open to all,’” the paper, which was published on June 1, reads.

Questions posed by the research arm of the Fed, which were undertaken in collaboration with the Universities of Pennsylvania and Chicago, examined the ramifications of the introduction of a CBDC and how the opening of central bank facilities might affect financial intermediation.

Specifically, the questions were aimed at exploring the role CBDCs play in “giving consumers the possibility of holding a bank account with the central bank directly,” in essence replacing the role currently performed by commercial banks.

Maturity transformation refers to the practice by financial institutions of borrowing money on shorter timeframes than they lend out. This is often done through deposits from savers by converting that finance into long-term borrowings such as mortgages. It is the role of commercial banks to facilitate the needs of lenders and borrowers.

This process can backfire though, such as if there is a panic or bank run where all savers attempt to withdraw money at once or if the money markets suddenly dry up due to lenders no longer providing short-term loans to one another.

The paper determined the set of allocations achieved with private financial intermediation (commercial banks) could also be achieved with a CBDC, provided competition is allowed with those commercial banks and depositors do not panic. However, the paper also determined an associated cost involved.

“Our equivalence result has a sinister counterpart. If the competition from commercial banks is impaired (for example, through some fiscal subsidization of central bank deposits), the central bank has to be careful in its choices to avoid creating havoc with maturity transformation,” according to the paper.

In other words, if CBDCs did disrupt the role of commercial banks and allowed the borrowing of more money than is lent out, there’s a concern central banks could harm the money markets.

The paper also showed how the “rigidity of the central bank’s contract with investment banks” deterred panic runs and, as such, if depositors started to exclusively deposit with the central bank it could end up becoming a “deposit monopolist,” attracting deposits away from the commercial banking sector.

“This monopoly power eliminates the forces that induce the central bank from delivering the socially optimal amount of maturity transformation,” the Fed paper says.

Updated: 6-8-2020

Central Bank of Saudi Arabia Transfers Funds To Local Banks Over Blockchain

The Saudi Arabian Monetary Authority has transferred funds to local banks using blockchain technology.

The Saudi Arabian Monetary Authority (SAMA), the country’s central bank, announced that it used blockchain technology to deposit funds to local banks.

An official statement published by SAMA said that the funds were a part of the bank’s initiative to enhance its “capabilities to continue its role in providing credit facilities.” The bank did not specify the exact amount of the fund transfer.

SAMA’s Involvement With Blockchain Technology

The Middle East is seeing widespread adoption of blockchain technology in the finance sector. SAMA has performed enormously in terms of using blockchain for remittances for banks located in Saudi and the United Arab Emirates.

In 2018, SAMA also partnered with the UAE’s central bank to develop a digital currency that can be used for cross-border transactions between the two countries.

Reflecting on their recent transaction and active involvement in the blockchain space, SAMA’s recent announcement stated:

“SAMA is one of the pioneer central banks to experiment [with] blockchain technology for money transfers, this move is one of the key innovative initiatives launched by SAMA in its program to enable and develop Fintech in the Kingdom.”

Blockchain In Finance

Increased involvement of governments and central banks in the blockchain sector is playing an important role in the adoption of the technology in finance.

Today, Cointelegraph reported that a major Turkish bank completed its first international trade finance transaction based on blockchain. Another report cited that almost 40% of fintech firms operating in Hong Kong were utilizing distributed ledger technology.

Updated: 6-8-2020

Chinese Bank Issues Commercial Paper Worth $16.9 Billion on Blockchain

A Chinese commercial bank issued China’s first asset-backed commercial paper worth $16.93 billion on a blockchain.

China Zheshang Bank, a national commercial bank, used blockchain technology to issue an asset-backed commercial paper, or ABCP. It was issued as a part of the National Association of Financial Market Institutional Investors’s (NAFMII) pilot project for ABCPs.

An asset-backed commercial paper is a short-term investment issued by financial institutions to help companies meet short-term goals.

Dubbed “Lianxin 2020 Lianjie First Phase Asset-backed Commercial Paper,” the period of the Lianxin ABCP is six months and the span of the next issuance is yet to be specified.

An official of the NAFMII noted that the use of blockchain technology would provide enterprises a “direct channel to markets, helping to greatly increase the accessibility of business financing.”

Helping Small And Micro Enterprises

Small, medium, and micro-enterprises usually face difficulties with bond issuance as they do not have any connection with open markets.

The launch of Lianxin ABCP will ensure that SMEs can seek easy financial support. The ABCP “increases the accessibility of financing for SMEs that have difficulty with financing via direct debt issuance,” an official stated.

It will also integrate supply chain finance with small, medium, and micro-enterprises to support them with their production.

China, Banks, And Blockchain

The central bank of China along with other major banks is spearheading blockchain innovation in traditional finance. On May 13, the People’s Bank of China’s deputy governor Fan Yifei urged that China needed to accelerate its blockchain adoption strategy. Only a day after that, Cointelegraph reported that the PBoC proposed a blockchain-based trade finance platform for the Guangdong-Hong Kong-Macao Greater Bay Area.

Earlier, in April, the Industrial and Commercial Bank of China released a white paper proposing the applications of blockchain technology in finance.

Updated: 10-11-2020

Central Banks Detail CBDC Expectations In Massive Joint Document

The report is a major step towards pushing central bank digital currencies forward.

With Central Bank Digital Currencies a point of focus across the globe, a number of countries’ banking authorities have jointly produced a document discussing the currency type at length.

The Bank for International Settlements told Cointelgraph in a statement that a group of seven central banks and the BIS had collaborated on the report, “identifying the foundational principles necessary for any publicly available CBDCs to help central banks meet their public policy objectives.” The BIS is a global institution helping out national central banks.

CBDCs have been a hot topic in 2020, with a number of countries expressing interest in the asset type. China has pushed forward with plans for its CBDC, the digital yuan, although China’s central bank did not contribute to the report. China is in the midst of testing its digital asset, and has completed approximately $162 million USD worth of digital yuan transactions.

The Bank of England, the U.S. Federal Reserve and the Bank of Japan sit among the governing bodies involved in crafting the document, titled: Central bank digital currencies: foundational principles and core features. However the statement from the BIS made it clear that the involved parties had not included opinions in the report regarding the launch of such a currency, nor did they specify any firm plans for producing such an asset.

The Report Clarified:

“This report is not about if or when to issue a CBDC. Central banks will make that decision for their jurisdictions (in consultation with governments and stakeholders). None of the central banks contributing to this report have reached a decision on whether or not to issue a CBDC.”

The report listed a trio of necessary fundamental principles upon which a future CDBC, and its related ecosystem, should be founded, if such an asset arises.

“A central bank should not compromise monetary or financial stability by issuing a CBDC; (ii) a CBDC would need to coexist with and complement existing forms of money; and (iii) a CBDC should promote innovation and efficiency.”

The document clarified that vital components of sound CBDCs include convertibility, convenience, security, speed, scalability, legal soundness and several other categories.

Brazil’s central bank has also expressed interest in a CBDC in recent months, although the report also did not list Brazil’s central bank as a contributor. In contrast, the Bank of Japan does grace the list of reported contributors. Japan boasts a team tasked with studying CBDCs.

Updated: 10-12-2020

Central Banks Haven’t Made A Convincing Case For Digital Currencies

It remains unclear what benefits e-money would bring to offset risks to bank funding and financial stability.

Central bankers should avoid getting too drawn into the bitcoin buzz.

On Friday, seven central banks—including the Federal Reserve—and the Bank for International Settlements published a report outlining common principles for issuing digital currencies to the public. Officials and corporations such as Facebook, inspired by cryptocurrencies, have spent years looking into the potential for technology to revolutionize money creation.

In a survey earlier this year, the BIS concluded that 20% of central banks are likely to launch a digital currency within six years. The risks posed by Covid-19 around the exchange of physical cash could heat up the race. China is furthest along and has launched a pilot program. Sweden’s Riksbank is also conducting its own test.

What remains unclear, though, is why this pitfall-ridden shift is necessary.

The most common justification, including in the latest report, is the decline in cash payments, which started well before Covid-19. The Riksbank’s haste to develop an e-krona has been fueled by Sweden becoming an almost cashless society.

But this doesn’t add up: If the shift to digital payments required digital currencies, why is it already happening via cards and mobile applications?

In papers published this year, Riksbank economists also claimed that, in a crisis, a digital currency might give households peace of mind that they could transfer their money into state-issued assets, and therefore be less afraid of leaving it in their bank.

The opposite seems much more likely: If a digital currency offered the advantages of both cash—anonymity and security—and a current account—the ability to transfer large sums with ease—nobody would choose to hold money in a bank deposit. Even outside of crises, this could leave banks without retail depositors, their most stable source of funding.

Indeed, many early supporters of digital currencies, such as the Bank of England’s Michael Kumhof, are also known for wanting to reduce the role of those forms of “money” not issued by governments. This would include deposits, which are issued by banks and used as money.

Reform proposals have so far been rejected by the public in places like Switzerland, but could be achieved in a roundabout manner if digital money issued by central banks ends up competing with bank deposits.

For banks, the funding gap would likely be filled by central banks and wholesale money markets. Far from increasing financial stability, as reformers claim, this would make banks more vulnerable. Lending to the real economy could be affected.

Friday’s report did highlight these risks, and established as a principle the need to “ensure the coexistence and complementarity of public and private forms of money.” Some central banks have floated proposals to cap e-currency holdings, so that bank deposits remain in use.

Yet there are few tangible benefits to weigh up against these risks. Policy makers have an abstract desire to broaden access to public money, but it is unclear why the “unbanked” would find e-money easier to use than a prepaid debit card.

The only real justification for digital currencies is privacy. But central banks don’t want too much privacy, either, given officials’ desire to increase know-your-customer and anti-money-laundering checks. The report said that “full anonymity is not plausible.”

Improving the payments systems that act as the lifeblood of the global economy is a worthy goal. The hype surrounding bitcoin and Facebook’s Libra, however, might be shifting the focus away from real-world problems that need fixing and onto untested solutions looking for a problem to fix.

Updated: 10-18-2020

In Thailand, A Free-Money Program Is Also A Data Experiment

The government is funneling assistance to the poor via cash cards—a convenient way to monitor spending despite privacy concerns.

Like many countries, Thailand is giving citizens cash transfers to help them ride out the coronavirus pandemic. But the military-backed government that rules the country is getting something potentially valuable in return: a huge volume of data on how millions of Thais spend their money.

Since 2017 Thailand has funneled assistance to its poorest citizens via so-called cash cards that are automatically loaded with a small amount of money each month. The cards are a more sophisticated version of the Electronic Benefit Transfer cards used to distribute food aid in the U.S., but linked to a much broader range of activities.

While the government says the information is needed to formulate better policies, privacy advocates are concerned—not least because the number of Thais who use the cards, about 14 million, is set to climb as more people thrown out of work by the Covid-19 pandemic sign up for assistance.

“Any time you’re talking about the government’s collection and use of personal data, particularly a large volume of it, the risks are always higher,” says David Hoffman, a cybersecurity expert at Duke University who also chairs the National Security Agency’s advisory panel on privacy. “The dystopian possibility,” he says, is “that you get a tremendous view into individual citizens that then could be used for a variety of government law enforcement purposes, particularly around the area of silencing social dissent.”

That’s far from a theoretical problem in Thailand. The country has been rocked in recent months by unprecedented protests against Prime Minister Prayut Chan-ocha, a former general who led a 2014 coup d’etat, as well as against the monarchy, which has traditionally been treated as off-limits for criticism.

Some activists calling for greater freedoms have been arrested, and a sweeping cybersecurity law passed in 2019 gives law enforcement agencies the power to collect information or seize equipment to prevent cybersecurity threats. In August, Human Rights Watch warned that Prayut had “adopted a more hostile stance toward pro-democracy activists.”

The card system could become a powerful tool for the government to build loyalty and curb dissent. More than $5.6 billion has been spent through the program, which links transaction data to information about personal finances, education, and biometrics using an open-source analytics software called KNIME.

A range of services are offered through the card and an associated app, including an allowance for travel on public transit and access to job training and health care.

Officials say that strict privacy measures are in place and that data from the cards is being used only to serve their stated purpose: helping the millions of Thais who are poor enough to qualify for one.

“We now have a large enough database to come up with more targeted policies,” says Lavaron Sangsnit, a Finance Ministry official who oversaw the card system until September. “It’s not a one-size fits all approach anymore. All of our efforts will now have a razor sharp focus.”

No-strings-attached cash transfers have become more popular among development economists in recent years, guided by the principle that recipients are better able to decide what they need than bureaucrats. One of the best known is Brazil’s Bolsa Familia, which provides money to families who ensure their children attend school and get necessary vaccinations.

Other countries, meanwhile, have turned to sophisticated digital systems to deliver existing welfare benefits. In India, a biometric identification platform called Aadhaar has enrolled more than one billion people. While an undoubted technological success, Aadhaar has been dogged by problems with security, including data leaks and thefts.

There have also been allegations by privacy activists that it could be used for improper surveillance, which government authorities have disputed.

Heavily dependent on exports and tourism, Thailand’s economy is expected to contract by as much as 8.5% this year, putting some 8 million jobs at risk. That could drive more people’s annual income below 100,000 baht ($3,200), the threshold for receiving a cash card. To cushion the impact of the pandemic on the poor, the government has increased monthly payments by 500 baht for the final quarter of the year.

Members of the ruling Palang Pracharath Party have not been shy about trying to leverage the program for political advantage. During last year’s general election, some voters said they were told at rallies that they needed to elect government-aligned candidates to keep their card benefits, prompting an opposition lawmaker to file a complaint with the elections regulator. (The agency rejected the allegations.)

Since the cards and associated welfare policies are being implemented “at the discretion of the government,” it’s fair to question “whether this could be used for politics,” says Thon Pitidol, an economics professor at Thailand’s Thammasat University who studied the program’s implementation.

Many poor Thais are just happy to have the extra cash—no matter what it might mean for politics or privacy. Liamtong Namwicha, a farmer who lives in the northeastern Sisaket province, says he’s found the card “useful” since getting one more than two years ago.

Liamtong, who is currently receiving 800 baht a month, has been using it to buy groceries and household necessities from a store in his village, and says he didn’t know data on his habits was being transmitted to policymakers—but that he isn’t worried about it. “I only use the card to buy instant noodles, vegetable oil, and detergent,” he says. “These are necessary things, so I don’t mind if they know.”

Updated: 10-19-2020

Better To Get It Right Than To Be First With CBDC, Says US Fed Chair

The U.S. already has a “safe and active dynamic domestic payment system,” Powell argued.

The United States will not be issuing a digital dollar until the Federal Reserve resolves all questions around a potential central bank digital currency, or CBDC, according to the Fed’s chairman, Jerome Powell.

Powell claimed that he is not worried about other countries having a first-mover advantage when it comes to issuing CBDCs.

Speaking at a Monday panel on cross-border payments hosted by the International Monetary Fund, Powell said:

“We have not made a decision to issue a CBDC, and we think there’s a great deal of work yet to be done. […] In fact, I actually do think that CBDC is one of those issues where it’s more important for the United States to get it right than it is to be first.”

Powell elaborated that “getting it right” means that the U.S. is not only looking at the potential benefits of a CBDC but also the potential risks — particularly given the fact that the U.S. dollar is the world’s reserve currency.

The official noted that countries around the globe will have their own motivations for issuing a CBDC. He contended that the main focus for the U.S. would be determining “whether and how a CBDC could improve an already safe and active dynamic domestic payment system.” Powell continued:

“Unlike some jurisdictions, here in the United States we continue to see strong demand for cash. Moreover, we have robust and mature financial and banking sectors, and we have a highly banked population, so that many, although not all, already have access to the electronic payment system.”

The Fed chair emphasized that the bank will not make a decision on issuing the digital dollar until it resolves CBDC-associated risks involving cyber attacks, financial stability, privacy and security. He stated:

“In addition to assessing the benefits, there are also some quite difficult policy and operational questions. […] Just to mention a few, I would mention the need to protect a CBDC from cyber attacks and fraud; the question of how a CBDC would affect monetary policy and financial stability; and also, how could CBDC prevent illicit activity while also preserving user privacy and security.”

Powell’s remarks come amid a number of global jurisdictions actively exploring and piloting CBDCs. Countries such as Russia and Japan are among the latest countries to jump on the CBDC bandwagon, while jurisdictions such as China and Sweden began testing their forthcoming digital currencies in 2020.

Despite the technology’s growing popularity across the globe, citizens in the U.S. are also skeptical about the idea of the digital dollar. According to a recent survey, more than 50% of Americans are opposed to the U.S. Fed issuing such an asset. In late September, the Federal Reserve Bank of Cleveland revealed details of the Fed’s ongoing research into a potential digital dollar.

95% Of Winners In China’s CBDC Lottery Spent Digital Yuan Prizes

Some winners purchased additional digital yuan during the pilot.

The vast majority of China’s $1.5 million digital yuan lottery winners have received and spent their “red envelopes” of digital yuan.

As of Sunday, a total of 47,573 out of 50,000 lottery winners in China have received their prizes, Shenzhen authorities officially announced.

According to the announcement, the winners conducted a total of 62,788 transactions accounting for 8.8 million yuan ($1.3 million). This amount represents about 88% of the total 10 million yuan ($1.5 million) that was to be distributed in the giveaway pilot in Shenzhen.

Some winners have not only spent their “red envelopes” but also topped up their wallets, having purchased an additional 901,000 yuan ($134,000).

Shenzhen launched a pilot program to promote the digital yuan with a public giveaway on Oct. 9. Lottery organizers said they would take back the unused amount of the digital yuan packets if winners did not spend it by Sunday

As previously reported, a total of 2 million people applied to participate in Shenzhen’s digital yuan giveaway program as of Oct. 12.

China’s central bank digital currency — the digital yuan — began testing in April. Pilots were subsequently expanded to nine cities, including Shenzhen and Guangzhou as well as Hong Kong and Macau.

Leaders of Global CBDC Projects Talk Shop In Panel Today

Central bank digital currency interest continues gaining global traction.

As part of DC Fintech Week, a digital conference on the governmental side of the financial technology sector, several international leaders gathered for an Oct. 19 panel called: Central Banks, CBDCs and Cryptoeconomics.

“I don’t see technological barriers in this area, but I do see technological challenges,” Cecilia Skingsley, First Deputy Governor of Riksbank, the central bank of Sweden, said on the panel.

“The challenge is not so much technology in itself, but it’s more about — we have to choose what sort of policy objectives do we want to focus on, what is the problem we want to solve,” she explained. “Depending on what that is, and the purposes we want to serve, then you choose the technology after that.”

The panel saw discussion between four separate authorities on various aspects of CBDCs, including the global race toward toward such a currency, as well barriers. In addition to Skingsley, the panel hosted BIS executive committee member Benoit Coeure, Bank of England deputy governor Jon Cunliffe, and former U.S. CFTC chairman J. Christopher Giancarlo.

As far as the Bank of England is concerned, Cunliffe explained cash as a cumbersome part of the economy. “Physical cash is no longer convenient,” he said. “It’s becoming increasingly inconvenient for people to use in their everyday lives, and the COIVD crisis has accelerated that,” he added. “On the other hand, it’s becoming increasingly less acceptable to merchants for some of the same reasons, even merchants that are able to take physical cash.”

Giancarlo specifically pointed out the competitive atmosphere around launching a CBDC, noting that winning the race is not the most important point — sentiment U.S. Federal Reserve chairman Jerome Powell also recently expressed.

“If there’s a winner, I don’t think the winner is necessarily who’s first and the loser is necessarily who’s last,” Giancarlo said during the panel. “What matters is, which central bank successfully incorporates its societal values in a successful development of CBDC,” he explained. “On the other hand, one can’t be too late to the game here,” he added.

Mentioning a report from the BIS from January 2020, Coeure reminded the audience that a large number of the world’s central banks consider CBDCs a worthwhile research effort. China has notably charged forward with its CBDC development in 2020.

Bitcoin Unlikely To Dodge Regulation For Long, Sweden’s Central Bank Says

Bitcoin and other cryptocurrencies are unlikely to escape regulatory oversight as supervisory authorities respond to the sheer popularity of the phenomenon, according to the governor of Sweden’s central bank.

Though monetary policy officials have voiced near universal skepticism toward Bitcoin and its rivals, cryptocurrencies have continued to build an enthusiastic following. That’s prompted some of the biggest names in finance to move in, as Wall Street banks such as Goldman Sachs Group Inc. offer trading services tied to crypto.

“When something gets big enough, things like consumer interests and money laundering come into play,” Riksbank Governor Stefan Ingves said on Monday. “So there’s good reason to believe that [regulation] will happen.” Erik Thedeen, the head of Sweden’s financial regulator, said on Tuesday that “it’s quite evident that some form of regulation is needed.”

Sweden’s financial markets minister, Asa Lindhagen, said the government is already in the process of tightening standards for crypto exchange platforms. But she called it a “work in progress at the international level.” She also said that addressing the risk of money laundering that cryptocurrencies represent is a “very important issue” that will require cross-border work.

It’s far from clear how to regulate a product that’s designed to evade the scrutiny of national authorities. But governments are already trying, with China in particular stepping up pressure on crypto loyalists. The People’s Bank of China recently told financial institutions that they’re not allowed to accept cryptocurrencies for payment, which followed a crackdown on crypto mining. There are signs, though, that traders are still active, underscoring the scale of the challenge.

In the U.S., Federal Reserve officials are in the process of studying “the various ways to address this issue,” Randal Quarles, the Fed’s vice chairman of supervision said in May. But federal agencies need time to ponder the right regulatory approach before they can then create a framework for oversight, he added.

In the European Union, the commission has put the matter to a hearing as it tries to figure out how best to create a regulatory framework for crypto assets. In September, it proposed a pilot regime for market infrastructures interested in trading crypto assets. Thedeen said an EU regulatory framework for cryptocurrencies is now “under way.”

On Tuesday, Riksbank Deputy Governor Per Jansson underscored concerns that Bitcoin and its peers continue to “fluctuate extremely,” with “nothing concrete or substantial” underpinning their actual value.

Sweden, like China, is one of the more advanced countries in its efforts to develop a central bank digital currency. That’s as monetary authorities try to prepare for the disappearance of cash as a payment form, and try to ensure that cryptocurrencies don’t fill the void. Ingves has previously estimated Sweden might have its own central bank e-krona in about five years.

Regulation of cryptocurrencies “will probably come at different times in different areas,” Ingves said.

What Bloomberg Economics Says…

“Fears of a ‘digital dollarization’ with a gradual loss of control over monetary conditions is one reason for central banks to introduce digital currencies of their own (as an alternative to private cryptocurrencies). As central banks accelerate moves toward a public digital payments option, it’s also likely that they will step up efforts to keep the volatile cryptocurrencies in check.”

Updated: 10-20-2020

The Bahamas Launches World’s First CBDC, The ‘Sand Dollar’

This makes The Bahamas one of the first countries in the world to officially launch a CBDC beyond a pilot program.

The Central Bank of the Bahamas has announced the country’s “Sand Dollar” — a state-backed virtual currency — is now available nationwide.

According to an Oct. 20 Facebook post from Project Sand Dollar, the central bank digital currency (CBDC) became available to all 393,000 residents of The Bahamas from roughly 10:00 PM UTC. This makes The Bahamas the first country in the world to officially roll out a CBDC.

China is currently testing a pilot program for its digital yuan with a $1.5 million giveaway, and Cambodia’s “Bakong” digital currency is expected to become operational in the coming months following its pilot launch in July 2019.

Sand Dollar transfers are made by mobile phone, with roughly 90% of the Bahamian population using mobile phones as of 2017.

According to the Sand Dollar website, residents of The Bahamas can use the digital currency at any merchant “with a Central Bank approved e-Wallet on their mobile device” and transaction fees are “negligible.” The central bank selected transaction provider NZIA as its technology solutions provider for the rollout of the digital currency.

The central bank of the Bahamas has been preparing for the launch of the CBDC for a few years. In 2019, it started a pilot program using 48,000 digital Sand Dollars on the islands of Exuma and Abaco, which have a combined population of fewer than 25,000 people. Each Sand Dollar is pegged to the Bahamian dollar, which is in turn pegged to the U.S. dollar.

The Sand Dollar is intended to drive greater financial inclusion within the archipelago nation of more than 700 islands, about 30 of which are inhabited. Cointelegraph reported in September that Chaozhen Chen, the assistant manager of eSolutions at the Central Bank of The Bahamas, said the CBDC would help provide “access to digital payment infrastructure or banking infrastructure” for underbanked and unbanked residents.

Updated: 10-26-2020

Bahamas Strikes First With Sand Dollar Amid US–China CBDC Faceoff

Fed Chairman Powell sees no urgency to develop a CBDC, but eventually, the world’s top central bank must act, say experts.

The Bahamas, an island nation in the West Indies, made digital currency history on Oct. 20 with the official launch of a new central bank digital currency, the so-called Sand Dollar.

It became the first country to roll out a CBDC available to all residents, and while the Bahamas is a small nation — with only 393,000 people — it appears to be an event of some global financial significance.

Or is it? “It could be if it succeeds,” Ross Buckley, KPMG-KWM professor of disruptive innovation at University of New South Wales, Sydney, told Cointelegraph. “Other small island nations — as in my backyard in the Pacific — are watching it carefully and could well follow suit.”

James Barth, a finance professor at Auburn University, placed the event in the context of a series of CBDC milestones, beginning with the launch of Bitcoin (BTC) in 2009 and including Facebook’s Libra announcement in 2019, China’s CBDC trials in April, and the European Central Bank’s statement about the possible issuance of a digital euro in October.

“These developments and the COVID-19 pandemic made it virtually certain that a country — most likely a small country — would go live with a central bank digital currency,” he said.

Some, however, said it was too early to tell. Hans Gersbach, an economics professor at ETH Zurich in Switzerland, told Cointelegraph: “First, we have to see whether it will function well in practice.”

Jay Joe, CEO of Nzia Limited — the technology solutions provider for the Bahamas rollout — told Cointelegraph that the Sand Dollar was introduced in the Bahamas to help facilitate financial inclusion across the nation:

“The Bahamas as a vast archipelago spreading across over 100,000 square miles of ocean, has many remote islands and communities where residents do not have access to formal financial services.”

Because of population sparsity, it often isn’t economically viable for banks to build branches and sustain infrastructure. The new CBDC “enables the people of The Bahamas universal access to digital payments and extends the reach of financial services to all corners of the nation,” Joe told Cointelegraph.

Among the key questions the nation’s central bank and others were looking to answer with the rollout, Joe said, were “how existing regulations and policies will be shaped, and, eventually, how the CBDC will be embraced by the people to some day become as ubiquitous as cash.”

A Sense of Urgency?

The global demand for online services has accelerated dramatically with the COVID-19 pandemic, and this is arguably driving the development of CBDCs around the world. As the deputy governor of the Central Bank of Canada, Timothy Lane, said recently.

“If we want to be ready to develop any kind of digital central bank product, we need to move faster than we thought was going to be necessary.” Barth further explained:

“The virus has shifted behavior in favor of more social distancing and therefore greater use of online communication and transactions, both domestically and globally. This certainly makes digital currencies more relevant as money and for payments.”

But this sense of urgency isn’t universal, as Jerome Powell, chairman of the United States Federal Reserve, said on Oct. 19 at an International Monetary Fund event. He believes that CBDCs face many critical challenges, such as preventing fraud and cyber attacks, ensuring financial stability, and protecting privacy, saying:

“There’s a great deal of work yet to be done. […] In fact, I actually do think that CBDC is one of those issues where it’s more important for the United States to get it right than it is to be first.”

The U.S. needn’t worry about losing the “first-mover” advantage with regard to a digital currency, Powell implied. Was he right?

“Probably in the immediate sense, yes,” according to Buckley, who added: “Longer term though if China or another nation allows its CBDC to be used in international trade, the U.S. will have to respond and quickly.”

The U.S. draws extraordinary benefits from minting the world’s reserve currency, and the loss of exclusivity in that regard could cost the U.S. economy dearly. It would also have political consequences — for instance, placing many countries outside the scope of U.S. financial sanctions. Buckley believes that China’s “long game” is, arguably, to upend the U.S. dollar as the world’s reserve currency.

“It [China] hates that the global economic system is built upon the U.S. dollar, and it aims to build a parallel system that it controls,” he said, further adding: “This was the impetus behind the denomination of trade contracts of other country’s exporters and importers with China in renminbi.”

It was also a motivation behind the New Development Bank established by the BRICS states — Brazil, Russia, India, China and South Africa — and also for the Asian Infrastructure Investment Bank, continued Buckley, referencing another multilateral development bank whose creation was proposed by China in 2009 to make better use of Chinese foreign currency reserves amid a global financial crisis.

“A [Chinese] CBDC will interact really well with dematerialized digital trade documentation so if China allows DC/EP offshore it will be a total game changer. In time I think they will.”

Barth, for his part, agreed that the U.S. didn’t have to hurry to bring a CBDC to market, as the U.S is the world’s largest economy, accounting for 20% of global gross domestic product, and the U.S. dollar remains the world’s dominant currency.

“Chairman Powell is right that the U.S. does not have to worry about losing any ‘first mover’ advantage by rushing to issue a central bank digital currency.”

On the other hand, Sidharth Sogani, founder and CEO of analytics firm Crebaco Global, told Cointelegraph that being first to market among large economies does matter. “China is already testing its CBDC. They have integrated POS machines, mobile apps and many other source codes to develop apps on their CBDC.”

He further opined: “First mover advantage is crucial in this case — especially when you are competing with China.” Financially, the U.S. is still dominant, but with regard to CBDC technology, it trails — “And here China is going to lead for sure as they are ready with their CBDC and are the second biggest economy globally.”

Sogani explained this from the point of view of a bank customer: “If you are already having a great experience with Bank A,” which uses a Chinese CBDC, “will you open an account or download an app with Bank B — which does business with a U.S. dollar CBDC?” If/when China launches its CBDC, it will attract large numbers of global customers very quickly. “It will be difficult to catch them.”

The U.S. should have a CBDC ready to go — just in case — suggested Gersbach. “Preparation should be stepped up in order to follow fast if successful models of CBCDs are introduced.” But according to Barth, the big question is how the “CBDCs will affect money and payments, particularly the role of the government.”

Gersbach also outlined several other factors: “Preventing cyber attacks, privacy issues, and financial stability. Security of all kinds and financial stability are the two most important issues to be resolved.”

Sogani, assuming that CBDCs would be built on a blockchain platform, questioned how CBDCs would relate to Bitcoin and other cryptocurrencies. “It’s [a CBDC] a completely different thing, with different fundamentals and uses. Understanding the nitty gritty is the biggest challenge.”

How Close Is The First Mass CBDC?

It seems that the development of CBDCs around the world has picked up in 2020, and if this is the case, when might one see the first massive-scale CBDC? According to Barth: “Most of the major countries have been studying CBDCs for some time now.” He added:

“China, of course, has been engaged in trials but with no information provided about a nationwide adoption date. Nevertheless, it is likely to be the first major country to issue a CBDC, and if so, it is likely to trigger other major countries to follow suit.”

Regarding China, Sogani said: “Their legal framework seems to be in the making. It will launch it for the masses in a few months. I don’t see any other country as close to China’s development stage.”

Meanwhile, according to Buckley: “China intends clearly its digital currency/electronic payment project to dominate payments and money within China domestically, and they’ve been working on it for five to seven years.”

As long as the project remains domestic, there is no real challenge to the United States. But if China takes it global, “It will take the U.S. years of work to respond with a CBDC of its own, the so-called digital dollar,” said Buckley.

Meanwhile, Sogani sees big benefits, even for small countries — like the Bahamas — that take the digital path. “A CBDC enables a country’s currency to go global which the current financial ecosystem doesn’t offer.” To make an international transfer, ample paperwork needs to be signed and fees paid. “This is expensive. It takes up to two days and is complicated,” commented Sogani, adding:

“But if it is a CBDC, it can go directly to the mobile apps, and it can be tracked. Yes, there will be compliance but the SWIFT method, which involves nostro and vostro accounts, will be eliminated — making life simpler.”

Joe called the Bahamas’ rollout “the world’s first production-grade live implementation of a retail CBDC.” Asked if there were lessons here for other nations, the NZIA CEO told Cointelegraph that there were many, “including the importance of grassroots engagement and understanding of CBDC and its effects on the intermediated financial system,” further adding:

“A CBDC is more than elaborate software and mobile wallet systems. It needs to be designed from the ground up and built as part of a national payments infrastructure that addresses the needs of everyday people.”

In sum, there appears to be a certain global logic to recent events. Because the U.S. dollar, the incumbent global currency reserve, has much to lose by coming to market with a flawed CBDC, it appears to be moving cautiously, content to let smaller players such as the Bahamas do its beta testing.

Meanwhile, China, the challenger, is moving fast, but its DC/EP project is focused on the nation’s mass market for now. A truly global digital yuan may still be some years away.

“A CBDC is a total game changer that raises a host of tough issues,” concluded Buckley. “This is why no one country has yet done it. Central banks never like stepping into the unknown — it’s not in their DNA for good reasons. But I think China will force other nations’ hands.”

Updated: 10-21-2020

Brazil’s Central Bank Just Revolutionized Instant Payments

Its new digital app turns free money transfers into a public good.

Earlier this year, my kitchen sink sprang a leak. With Brazil bracing for coronavirus, how to find a repairman willing to risk Rio de Janeiro’s pathogen-friendly public transit for a one-off job in a stranger’s home? Lucky for me, Antonio was game.

A freelance plumber, Antonio is part of Latin America’s vast shadow economy, where today’s gig is tonight’s meal. Unfortunately, most Brazilian handymen prefer cash, just the sort of high-touch tender I had foresworn in times of Covid-19.

We settled on a bank transfer, and a few pecks at my phone app and a hefty transfer fee later, I’d whisked the money from my account to his. Or so I thought. Two days, four phone calls and several worried text messages from Antonio later, the funds finally landed.

Fortunately, those anxious days may be numbered. Next month, the Central Bank of Brazil will debut a new instant payments tool. Called PIX, it promises hassle-free transactions within seconds for anyone with a mobile phone and a bank account.

And it comes free of charge. The bank has already logged more than 39 million requests by prospective PIX clients, both corporate and individual, eager to lock in access “keys” to the service.

Brazilian banking was long due for a shakeup. Latin America’s signature economy boasts some of the world’s biggest and most lucrative banks, where dexterous moneymen finessed hyperinflation and the shell game of serial government stabilization plans through market acumen and innovation.

Yet these sophisticated brand banks still deliver many of their headline services on last century’s clock — Monday to Friday from 10-to-4, and 10-to-2 during the pandemic — and often at bruising lending rates and fees.

No wonder some 45 million Brazilians have no bank account, and 71% still prefer to do business in cash.

“Brazilian banking has long been dominated by a few big players who enjoy a practically captive clientele,” said Paulo Bilyk, chief executive of Rio Bravo Investimentos, a Sao Paulo asset management firm.

Reinforcing this sweetheart market is the cozy system that deposits the paychecks of 11.4 million relatively well-paid public employees in banks they did not even choose. “The new system facilitates exchanges by making it simpler, faster and cheaper to pay bills. That’s a win for the economy and for social inclusion,” Bilyk said.

Sensing the opportunity, regulators began preparing early last decade to disrupt the financial monopoly by greenlighting virtual banks, which peddle checking and savings accounts, credit and debit cards exclusively online and at considerable discounts. Investment in Brazilian fintech has since soared, from $52 million in 2015 to $1.6 billion last year.

Brazil is now home to the world’s largest digital-only bank, Nubank, with 20 million clients nationally and operations in Argentina, Colombia and Mexico.

Brazil is actually a relative latecomer to instant digital payments. Kenya launched its M-Pesa system (42 million subscribers) via mobile phone in 2007; India’s four-year-old Unified Payments Interface clocked 1.62 billion transactions in June; China’s two biggest digital wallet competitors, Alipay and WeChat Pay, have more than 2.2 billion active users.

Yet those are competitive businesses, each of which takes a cut per transaction. PIX, by contrast, is a public good, launched by the Central Bank and free of charge. The initiative was an attempt to lay the ground rules — and perhaps get a jump on the competition — in the relatively cloistered Brazilian economy for an aggressive frontier business dominated by international giants.

Tellingly, the Central Bank in June withdrew authorization for WhatsApp Payments, the Facebook-owned phone-based payment tool, a week after its Brazilian rollout.

A rare oasis of institutional continuity in the Brazilian policy desert, the Central Bank has already helped promote a more inclusive financial market by eschewing the monetary populism that has kept inflation high and lending dear.

Brazil’s interest rates hit record lows this year. The surging digital culture — 150 million internet users and 205 million mobile phones in a country of 212 million people — has only sharpened the public appetite for innovation.

“Brazilian society is much closer to China than to the U.S. or Europe,” said Claudio Lucena, technical director for the National Data Protection Institute. “We have millions of low-income people with limited access to market information, but who have mobile phones. For them, reducing the cost of banking could be a major incentive.”

Legacy banks, understandably, are less enthusiastic. They stand to forfeit a bundle in fees for moving money. The bank transfers nest egg has grown 31% since 2017, according to Moody’s Investors Service, which says banks could forfeit as much as 8% of their annual winnings in traditional transfers to PIX users.

The Sao Paulo market research company Eleven Financial Research projects a much smaller hit of around 1% of their yearly fee income. “Traditional banks might have wished that PIX had never come along,” said Bilyk.

Indeed, they had no choice. The Central Bank has ordered all financial institutions with more than 500,000 clients to offer account holders the option to sign up for the no-charge pay app. Lenders have joined the October scramble to lock up PIX accounts.

Brazil’s enterprising bandits have been right behind them, hoping to lure unwitting early adopters to divulge their identities and banking information on fake websites. “The rollout for PIX will probably be gradual,” said Eleven Financial’s head of equity research Carlos Daltozo. “Security and fraud are key concerns.”

Instant payments won’t revolutionize Brazilian productivity, stanch fiscal incontinence or fix the regressive and enterprise-choking tax system.

“We basically know what we have to do put the economy right,” Bloomberg Economics analyst Adriana Dupita told me. “But by making it easier and more affordable to pay bills and transfer money, you invite more people into the system and make financial transactions more accessible.”

At a time when Brazilian politics has devolved into a contest over how to spend more, a tool allowing individuals to spend better is already a blessing.

Updated: 10-21-2020

Brazil’s Central Bank Just Revolutionized Instant Payments

Its new digital app turns free money transfers into a public good.

Earlier this year, my kitchen sink sprang a leak. With Brazil bracing for coronavirus, how to find a repairman willing to risk Rio de Janeiro’s pathogen-friendly public transit for a one-off job in a stranger’s home? Lucky for me, Antonio was game.

A freelance plumber, Antonio is part of Latin America’s vast shadow economy, where today’s gig is tonight’s meal. Unfortunately, most Brazilian handymen prefer cash, just the sort of high-touch tender I had foresworn in times of Covid-19.

We settled on a bank transfer, and a few pecks at my phone app and a hefty transfer fee later, I’d whisked the money from my account to his. Or so I thought. Two days, four phone calls and several worried text messages from Antonio later, the funds finally landed.

Fortunately, those anxious days may be numbered. Next month, the Central Bank of Brazil will debut a new instant payments tool. Called PIX, it promises hassle-free transactions within seconds for anyone with a mobile phone and a bank account. And it comes free of charge.

The bank has already logged more than 39 million requests by prospective PIX clients, both corporate and individual, eager to lock in access “keys” to the service.

Brazilian banking was long due for a shakeup. Latin America’s signature economy boasts some of the world’s biggest and most lucrative banks, where dexterous moneymen finessed hyperinflation and the shell game of serial government stabilization plans through market acumen and innovation.

Yet these sophisticated brand banks still deliver many of their headline services on last century’s clock — Monday to Friday from 10-to-4, and 10-to-2 during the pandemic — and often at bruising lending rates and fees.

No wonder some 45 million Brazilians have no bank account, and 71% still prefer to do business in cash.

“Brazilian banking has long been dominated by a few big players who enjoy a practically captive clientele,” said Paulo Bilyk, chief executive of Rio Bravo Investimentos, a Sao Paulo asset management firm.

Reinforcing this sweetheart market is the cozy system that deposits the paychecks of 11.4 million relatively well-paid public employees in banks they did not even choose. “The new system facilitates exchanges by making it simpler, faster and cheaper to pay bills. That’s a win for the economy and for social inclusion,” Bilyk said.

Sensing the opportunity, regulators began preparing early last decade to disrupt the financial monopoly by greenlighting virtual banks, which peddle checking and savings accounts, credit and debit cards exclusively online and at considerable discounts. Investment in Brazilian fintech has since soared, from $52 million in 2015 to $1.6 billion last year.

Brazil is now home to the world’s largest digital-only bank, Nubank, with 20 million clients nationally and operations in Argentina, Colombia and Mexico.

Brazil is actually a relative latecomer to instant digital payments. Kenya launched its M-Pesa system (42 million subscribers) via mobile phone in 2007; India’s four-year-old Unified Payments Interface clocked 1.62 billion transactions in June; China’s two biggest digital wallet competitors, Alipay and WeChat Pay, have more than 2.2 billion active users.

Yet those are competitive businesses, each of which takes a cut per transaction. PIX, by contrast, is a public good, launched by the Central Bank and free of charge.

The initiative was an attempt to lay the ground rules — and perhaps get a jump on the competition — in the relatively cloistered Brazilian economy for an aggressive frontier business dominated by international giants. Tellingly, the Central Bank in June withdrew authorization for WhatsApp Payments, the Facebook-owned phone-based payment tool, a week after its Brazilian rollout.

A rare oasis of institutional continuity in the Brazilian policy desert, the Central Bank has already helped promote a more inclusive financial market by eschewing the monetary populism that has kept inflation high and lending dear.

Brazil’s interest rates hit record lows this year. The surging digital culture — 150 million internet users and 205 million mobile phones in a country of 212 million people — has only sharpened the public appetite for innovation.

“Brazilian society is much closer to China than to the U.S. or Europe,” said Claudio Lucena, technical director for the National Data Protection Institute. “We have millions of low-income people with limited access to market information, but who have mobile phones. For them, reducing the cost of banking could be a major incentive.”

Legacy banks, understandably, are less enthusiastic. They stand to forfeit a bundle in fees for moving money. The bank transfers nest egg has grown 31% since 2017, according to Moody’s Investors Service, which says banks could forfeit as much as 8% of their annual winnings in traditional transfers to PIX users.

The Sao Paulo market research company Eleven Financial Research projects a much smaller hit of around 1% of their yearly fee income. “Traditional banks might have wished that PIX had never come along,” said Bilyk.

Indeed, they had no choice. The Central Bank has ordered all financial institutions with more than 500,000 clients to offer account holders the option to sign up for the no-charge pay app. Lenders have joined the October scramble to lock up PIX accounts.

Brazil’s enterprising bandits have been right behind them, hoping to lure unwitting early adopters to divulge their identities and banking information on fake websites. “The rollout for PIX will probably be gradual,” said Eleven Financial’s head of equity research Carlos Daltozo. “Security and fraud are key concerns.”

Instant payments won’t revolutionize Brazilian productivity, stanch fiscal incontinence or fix the regressive and enterprise-choking tax system. “We basically know what we have to do put the economy right,” Bloomberg Economics analyst Adriana Dupita told me. “But by making it easier and more affordable to pay bills and transfer money, you invite more people into the system and make financial transactions more accessible.”

At a time when Brazilian politics has devolved into a contest over how to spend more, a tool allowing individuals to spend better is already a blessing.

Updated: 10-26-2020

Digital Yuan Will Work With WeChat And Alipay, Says Bank Exec

Details regarding the digital yuan’s characteristics are taking shape.

The forthcoming digital yuan will reportedly be compatible with major payment networks within the country.

Mu Changchun, the head of the People’s Bank of China’s digital currency research institute, said that the central bank-backed digital yuan will be compatible with major mobile payment wallets like WeChat Pay and Alipay.

According to a report from South China Morning Post, Mu said during a conference that the digital yuan will not compete with WeChat Pay and Alipay:

“They don’t belong to the same dimension. WeChat and Alipay are wallets, while the digital yuan is the money in the wallet.”

These recent statements would appear to contradict earlier reports from local sources suggesting that China may launch its digital currency as an alternative to the two payment giants.

The digital yuan is currently accessible to limited users through an exclusive mobile wallet application. At the conference, Mu said that the mobile wallets for digital yuan face the age-old problem of counterfeiting, stating that there were multiple fake digital yuan wallets in the market.

Mu said it would only be possible to reduce the impact of counterfeit wallets if all parties involved, from the central bank to the users, take necessary cautions.

On a different note, Mu said that the digital yuan operates on a centralized infrastructure, differentiating it from private currencies like Facebook’s Libra and Bitcoin (BTC).

China has progressed rapidly with its central bank digital currency initiative. Last week, it published a draft law to provide a regulatory framework and legitimacy for its digital yuan. At present, the central bank is conducting pilot tests across the country for its CBDC.

In one of the largest pilot tests, local authorities distributed $1.5 million worth of digital yuan to 50,000 of the 1.9 million people who signed up for a giveaway.

Updated: 11-2-2020

China’s Digital Yuan Pilots Have Processed $300M So Far, Says PBoC Head

China’s digital yuan pilot program is picking up speed.

The governor of China’s central bank has given more details about the country’s ongoing digital currency pilot.

Yi Gang, governor of the People’s Bank of China, said that the digital yuan pilots have processed over four million transactions to date, totaling more than 2 billion yuan ($299 million). The official delivered his latest remarks at the Hong Kong Fintech Week conference on Nov. 2, Bloomberg reported.

According to Yi, the pilots have been going smoothly so far, having rolled out for extended testing in four cities.

Growth in demand for digital and contactless payment methods amid the coronavirus pandemic have posed major challenges for central banks, as they try to juggle user security with convenience, Yi said.

The official noted that fintech companies have some key advantages over commercial banks in terms of building a customer base and managing risks.

The PBoC launched the first pilots for its forthcoming digital yuan in April 2020. The initial trial reportedly included four major cities: Shenzhen, Chengdu, Suzhou and Xiongan. The program was reportedly expanded to nine cities, including Guangzhou, Hong Kong and Macau.

In early October, the PBoC officially announced that the digital yuan wallets processed $162 million in transactions between April and August 2020.

Major tech companies have already begun preparing for the seemingly inevitable launch of the digital yuan. Huawei recently announced that its newest smartphone, Mate40, will feature a wallet for the currency and allow users to transact with it, even when they are offline.

Reserve Bank of Australia Forms Partnerships To Research CBDC

The project will “explore if there is a future role for a wholesale CBDC in the Australian payments system,” according to the RBA.

According to a Nov. 2 announcement from The Reserve Bank of Australia, or RBA, the financial institution will be partnering with the Commonwealth Bank, National Australia Bank, the financial services company Perpetual, and software company ConsenSys on a project to explore the potential use of a wholesale central bank digital currency in the country using “Ethereum-based distributed ledger technology.”

The RBA stated it would be researching the development of a proof-of-concept for “the issuance of a tokenized form of CBDC.” It specifically mentioned wholesale market participants potentially using the digital currency for tokenized syndicated loans on an DLT platform and exploring the implications of delivery-versus-payment security settlements with cross-chain atomic swaps.

“With this project we are aiming to explore the implications of a CBDC for efficiency, risk management and innovation in wholesale financial market transactions,” stated Reserve Bank of Australia Assistant Governor Michele Bullock.

“While the case for the use of a CBDC in these markets remains an open question, we are pleased to be collaborating with industry partners to explore if there is a future role for a wholesale CBDC in the Australian payments system,” he added.

The move is part of an ongoing about-face for the RBA when it comes to CBDC policy. On Oct. 14, the head of payments policy at the RBA said the bank would continue to research CBDCs despite the financial institution stating there was not a strong policy case for issuing one in September.

As alternatives to issuing a CBDC, the bank has pointed to the success of the country’s efficient, real-time New Payments Platform, and stated it is willing to provide access to fiat banknotes “for as long as Australians wish to keep using them.”

The central bank said the project will be finished by the end of the year and it will issue a report in 2021.

Updated: 11-9-2020

US Fed Economists Are Exploring The “Intrinsic” Value Drivers Of CBDCs

Fed economists are beginning their deep dive into CBDC research, hoping to identify the “intrinsic” value drivers of a digital dollar.

The United States Federal Reserve has broadened its research on central bank digital currencies, or CBDCs, in a new review that was posted to its website Monday.

In a report titled “Central Bank Digital Currency: A Literature Review,” Fed economists Francesca Carapella and Jean Flemming compile research exploring the potential impact of a digital dollar on commercial banking and monetary policy. The review provides a theoretical underpinning for understanding how CBDCs could influence consumer adoption and financial stability.

The Authors Write:

“From a theoretical standpoint, the introduction of a central bank digital currency (CBDC) raises long-standing questions relating to the provision of public and private money […] and the ability of the central bank to use CBDC as a means for transmitting monetary policy directly to households.”

A literature review is essentially an environmental scan on a particular topic that is used to justify the need for additional research. The Fed’s report identified the “intrinsic features of CBDC” as the most important research question to tackle moving forward:

“As with any new literature, many questions remain. We believe the most crucial question is which intrinsic features of CBDC as a means of payment and a store of value are important for households’ portfolio choices as to which monies to use.”

On Aug. 13, the Fed released an original research paper comparing CBDCs with other payment methods. Authors Paul Wong and Jesse Leigh Maniff concluded that a CBDC would “never be able to fully replicate” all the features of cash and real-time gross settlement services but that it could enhance both modes of payment.

Although CBDCs have been described as the central bank “arms race” of the decade, the Fed is in no rush to adopt the so-called digital dollar. Fed Chair Jerome Powell said last month that a CBDC is unlikely to be rolled out anytime soon because the U.S. already has a “safe and active dynamic domestic payment system.”

Powell emphasized that resolving risks to privacy and security is more important than having a first-mover advantage in this space.

China, meanwhile, is taking a far more active approach in rolling out its digital currency. Last month, the People’s Bank of China concluded its largest pilot project on the digital yuan by distributing online wallets to 50,000 randomly selected consumers.

Updated: 11-10-2020

Lebanon To Launch Digital Currency In Face Of Economic And Financial Turmoil

Lebanon’s central bank governor says the country, whose lira has been in freefall, is preparing to launch a digital currency in 2021.

Lebanon’s central bank plans to launch a new digital currency in 2021 as part of a broader effort to combat a parallel economic and financial crisis that has engulfed the country.

Central bank governor Riad Salameh told a gathering of officials Monday that “We must prepare a Lebanese digital currency project” as a way to shore up confidence in the banking system.

“As for the monetary supply in the Lebanese market, it is estimated that there are $10 billion stored inside homes,” Salameh said, according to the state-run National News Agency.

The central banker added that a digital currency project launched in 2021 will help implement a cashless financial system to enhance the flow of money locally and abroad.

Lebanon relies heavily on remittances from its vast global diaspora. In 2019, personal remittances represented nearly 14% of Lebanese gross domestic product, according to the World Bank. That figure was as high as 26.4% in 2004.

Salameh says Lebanon will maintain its gold reserves as a hedge against a wider market crisis. If such a crisis occurs, the central bank can liquidate its bullion on foreign markets for immediate relief.

Banque Du Liban, the country’s central bank, has been kicking around the idea of a state-run digital currency since at least 2018. Efforts appear to have accelerated earlier this year after violent protests and silent bank runs brought Lebanon’s financial system to a halt.

Faced with a dollar crisis, banks tightened restrictions on foreign currency transactions, with at least one major institution limiting withdrawals to just $400 a month. A plunging Lebanese lira made it almost impossible to transact in the local currency.

In June, protestors set fire to the central bank in Tripoli in a show of anger over the collapse of the lira, which had long been pegged at 1,500 per U.S. dollar. The lira would eventually plunge to more than 5,000 per dollar before restabilizing.

The growing confusion over Lebanese fiat triggered a wave of Bitcoin buying among locals, with peer-to-peer marketplaces like Localbitcoins seeing a sharp rise in activity.

Political chaos is nothing new for Lebanon. The tiny Mediterranean country has struggled to form an identity following its 15-year-long civil war. A sectarian power-sharing system ruled by feudal elites has made governing the country extremely difficult, even during periods of relative calm.

Updated: 11-10-2020

US Central Banker Urges Digital Dollar Development

FOMC member Robert Kaplan believes the Fed should prioritize creating a digital dollar.

President of the Dallas Federal Reserve Robert Kaplan believes the US central bank should begin work on a digital currency immediately, a clear indicator that some policymakers view this as an urgent matter.

Speaking Tuesday at a virtual conference hosted by Bloomberg, Kaplan reportedly said:

“It is critical that the Fed focuses on developing a digital currency in the coming months and years.”

The central banker’s remarks were part of a broader discussion on the economy and fiscal policy.

Kaplan is a member of this year’s Federal Open Market Committee (FOMC), the organization tasked with setting monetary policy. The 2020 Committee slashed interest rates to record lows in March as part of a synchronized policy response to Covid-19.

Kaplan and the rest of the FOMC have been instrumental in flooding the market with liquidity since Sept 2019, when irregularities in the overnight repo market caused short-term interest rates to spike.

Blockchain technology is certainly on policymakers’ radar. Last month, Fed Chairman Jerome Powell said that 80% of central banks around the world are exploring the potential utility of a CBDC.

While the Fed has given no indication of whether it will pursue a digital dollar, it has deployed economists to explore the subject in greater detail.