Purchases With Plastic Get Costlier For Merchants—And Consumers (#GotBitcoin?)

Visa and Mastercard plan to raise fees on credit and debit cards, putting new strain on retail. Purchases With Plastic Get Costlier For Merchants—And Consumers (#GotBitcoin?)

Related:

Bitcoin Usage Among Merchants Is Up, According To Data From Coinbase And BitPay

The recession has changed consumers’ payment preferences, with more card purchases occurring online and via digital wallets.

Big networks and issuers are making it hard for merchants to use cheaper card networks.

Meanwhile, the crypto-currency industry drives cost to near-zero levels with various fintech solutions.

Credit-card companies are increasing a range of fees that U.S. merchants will pay to process transactions, a move likely to inflame already fractious relations between many businesses and card networks.

Related: Insecurity of Credit Cards

Capital One Reports Data Breach Affecting 100 Million Customers, Applicants (#GotBitcoin?)

British Airways Faces $230 Million Fine Over Data Breach (#GotBitcoin?)

Equifax And FICO Team Up To Sell Your Financial Data To Banks (#GotBitcoin?)

Cyber-Security Alert!: FEMA Leaked Data Of 2.3 Million Disaster Survivors (#GotBitcoin?)

BlackRock Exposes Confidential Data on Thousands of Advisers on iShares Site (#GotBitcoin?)

Amazon, Amid Crackdown on Seller Scams, Fires Employees Over Data Leak (#GotBitcoin?)

Thieves Can Now Nab Your Data In A Few Minutes For A Few Bucks (#GotBitcoin?)

Data Breach At Question-and-Answer Site Quora Affects 100 Million (#GotBitcoin?)

Venmo And Amazon Hit By Breaches And Fraudsters (#GotBitcoin?)

Google Exposed User Data, Feared Impact Of Public Disclosure (#GotBitcoin?)

Visa Inc. and Mastercard Inc., the two biggest U.S. card networks, are preparing increases to certain existing fees that will kick in this April, according to people familiar with the matter.

Some of the changes relate to so-called interchange fees. Card networks set the price of these fees, which merchants pay to banks when consumers shop with the cards they issue. Also due to rise are fees that card networks charge financial institutions for processing card payments on behalf of merchants.

Merchants often increase the prices consumers pay following such fee increases, in an attempt to protect their own profits. Roughly 1% to 2.5% of prices for goods and services go to cover card fees, according to people familiar with merchant pricing.

Consumers often pay for those fees whether they pay with cash or card. While big in the aggregate—merchants pay tens of billions of dollars in card fees annually—per-transaction changes are often minuscule and so go largely unnoticed by consumers.

A Visa spokeswoman said “Visa’s network fees are paid by our financial institution clients and used to enhance the safety, efficiency and innovation of our platform, and are set based on market conditions and to reflect the value we deliver.” She said the new price changes impact fees that Visa hasn’t adjusted in at least three years.

A Mastercard spokesman declined to comment.

Separately, returned merchandise purchased using Mastercard debit cards will in some cases become more expensive for stores, according to a person familiar with the matter. In some transactions, merchants won’t be reimbursed for the interchange fee that was paid on the initial transaction.

Meanwhile, Discover Financial Services , which is both a network and a card issuer, is preparing to increase certain interchange fees. This will include rewards credit cards used to shop at restaurants and when certain Discover credit cards are used for online shopping, according to a person familiar with the matter. A Discover spokesman declined to comment.

Card fees are a long-running point of contention as consumers shift more spending from cash to cards. Merchants say card-company charges are exorbitant and that there is little they can do in the face of price increases.

An additional bone of contention: Fees aren’t uniform. A small number of big merchants often incur lower fees due to the volume of transactions they handle, including giant retailers such as Amazon.com Inc., Walmart Inc . and Costco Wholesale Corp. that have negotiated special arrangements, according to people familiar with the matter.

For their part, card companies say credit and debit cards result in more sales for merchants than would otherwise occur and that expenses tied to fraudulent card purchases and other costs need to be covered.

The pushback against card fees has been particularly pronounced outside the U.S. In recent years, interchange fees on debit and credit cards that are paid in many European countries have been lowered and capped. Visa and Mastercard recently reached a proposed settlement with European Union regulators to lower the interchange fees merchants in the region pay on debit and credit cards issued outside of the area.

In the U.S., the dollar amount of interchange fees paid by stores, which has been surging in recent years, is at the center of fights between merchants, card networks and large banks that issue cards. Banks are the ultimate recipients of these fees; card networks at times increase them so that banks will issue or retain cards on their networks.

Those fees help fund the points and cash back that banks pay to their cardholders when they redeem rewards. Card companies tend to increase at least some interchange fees every few years, while rewards programs have grown in popularity.

Large U.S. merchants, including Amazon, Target Corp. , and Home Depot Inc., are pursuing litigation against Visa, Mastercard and large banks aimed at eventually lowering these fees.

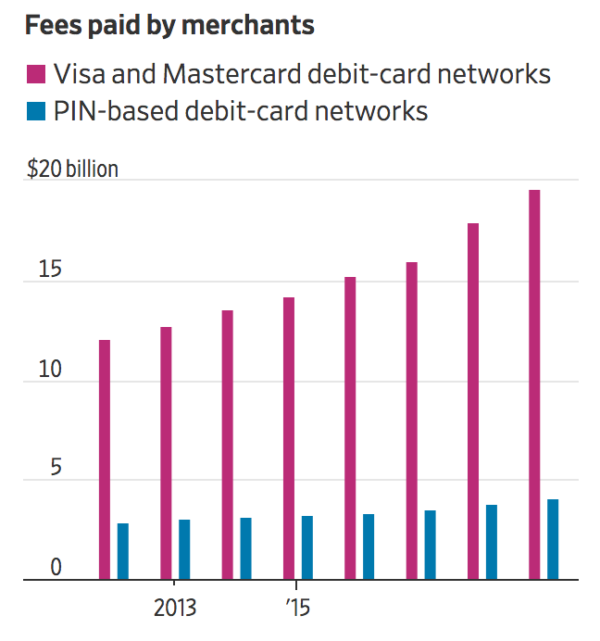

Merchants paid an estimated $64 billion in Visa and Mastercard credit and debit interchange fees last year, according to new data from an industry publication, the Nilson Report. That is up 12% from a year earlier and up 77% from 2012.

Other fees are on the rise, as well. Visa, the largest U.S. card network, is increasing several fees in April, according to people familiar with the matter. Unlike interchange fees that are paid to card issuers, these fees are collected by Visa.

Visa raised its “credit-card assessment fee” this year by 0.01% for most credit-card purchases made in the U.S.

While seemingly small on a percentage or flat-fee basis, the increased fees that Visa will put in place during the first four months of the year are expected to cost U.S. merchants at least an additional $570 million through April 2020, according to estimates by merchants-payments consulting firm CMSPI.

A Visa spokeswoman disputed the figure, saying it was inflated, but didn’t provide further detail.

But network fees aren’t the only additional charges merchants face. There are also other fees charged by firms that process merchants’ card transactions. Those, which include the network fees, totaled $14.8 billion on Visa and Mastercard debit and credit transactions in 2018, up 10% from a year earlier and 70% from 2012, according to the Nilson Report.

Updated: 6-21-2020

The Credit-Card Fees Merchants Hate, Banks Love and Consumers Pay

Growing and largely hidden interchange economy creates ‘a giant reverse Robin Hood’.

In Silver Spring, a Maryland suburb of Washington, D.C., cash is becoming a rarity as consumers increasingly rely on credit cards, apps and online purchases during the pandemic.

For Bump ’n Grind, an independent coffee and vinyl record shop, that is a growing burden. The shop, which roasts its own coffee beans, spent less on green beans last year ($12,827) than on the card-processing fees ($18,645) it pays to the financial institutions that enable cashless payments.

“That’s depressing,” said owner David Fogel. “All you know is at the end of the month they’re pulling out X thousands of dollars.”

Mr. Fogel closed his store for nearly two months during the coronavirus pandemic while continuing to roast and deliver beans. The coffee shop is now open for takeout. Depending on whether he can renegotiate his rent, Mr. Fogel said he may shut his store to focus on wholesale coffee beans.

The store is a microcosm of tensions sparked by the growing and largely hidden interchange economy: the stream of fees merchants pay to banks. The fees help drive the payments system. Merchants hate them; banks love them.

In the middle are consumers. The fees push up prices for everyone. They also fund a growing array of cardholder rewards—which flow largely to affluent customers.

When you buy something with a credit card, the merchant often remits around 2% of the price to the bank that issued it. The fee can be higher, at times around 3%, on more generous reward cards. The bank returns some of these “interchange fees” (also called swipe fees) to the cardholder in the form of rewards, including cash back, points or airline miles. (Separate, smaller fees are paid to the payment networks, such as Visa Inc. and Mastercard Inc., and to the financial institution that helps process the transactions.)

Because retailers’ profit margins are slim, they pass some of the fees to customers through higher prices, according to the National Retail Federation.

Customers typically pay the same price whether they use cash or a card. Economists say this equates to a transfer from users of cash to users of cards. How much? On average a cash-using household pays $149 a year and a card-using household receives $1,133, according to a 2010 study from the Federal Reserve Bank of Boston.

The discount to customers who often make hundreds of thousands of dollars a year “is a giant reverse Robin Hood moving billions of dollars a year,” said Aaron Klein, a fellow at the Brookings Institution specializing in the financial industry.

The card industry disagrees. “Americans of all income levels responsibly use and receive great value from their cards and rewards programs,” said Jeff Tassey, board chairman of the Electronic Payments Coalition, which represents financial institutions and card networks. “Bigger spenders will receive proportionately more rewards, which tend to be proportional to spending—how else would you do it?”

Most U.S. households that have credit cards have a rewards card, even those earning less than $20,000 a year, according to Greg Weed, director of card-performance research at Phoenix Marketing International, which tracks the credit-card market.

Merchants paid issuers $53.6 billion in Visa and Mastercard credit-card interchange fees in 2019, more than double what they paid in 2012, according to the Nilson Report, a trade publication. The growth reflects two things. First, credit-card use rose in recent years: Americans made 67% more credit-card payments in 2018 than in 2012, according to the Federal Reserve. Second, banks rolled out more cards with higher interchange fees to pay more rewards.

To help pay for rewards, banks also are charging higher rates. Average annual percentage rates for credit cards have risen more for those with the lowest credit scores: by about 4.2 percentage points since 2010, according to WalletHub.com, a consumer-finance website, compared with about 1.3 points for those with the highest credit scores.

Low-income consumers who have credit cards often find the costs they incur for carrying balances outweigh rewards. Tanya Villani of Bedford, Va., relies on credit cards to help pay for groceries, gasoline, car insurance and medical costs when her disability income of roughly $1,000 runs out every month. In January she was approved for a rewards card, a QuicksilverOne card from Capital One Financial Corp., which has a $300 spending limit. She currently owes around $300 and is paying interest of about 25%.

“I needed some kind of buffer for my income,” she said, “to last me to the end of the month.”

Merchants, who have battled card companies over interchange fees for decades, are using the impact on low-income consumers to help make their case.

Card networks bar merchants from accepting some but not all of their credit cards. A merchant who accepts Visa credit cards can’t turn down premium cards such as JPMorgan Chase & Co.’s Sapphire Reserve, which are often carried by wealthier Americans and have higher interchange fees. Roughly 63 merchants, including Amazon.com Inc., Lowe’s Cos ., Gap Inc. and Starbucks Corp. are suing Visa, Mastercard and card-issuing banks, alleging they collude to avoid competing over interchange fees. The merchants allege card fees are a hidden tax, including on lower-income consumers who are more likely to pay with cash.

Merchants want the freedom to select which cards they accept and to negotiate interchange fees directly with card-issuing banks rather than Visa and Mastercard.

Card companies say this would confuse consumers. They say interchange fees help cover costs such as fraud, innovation, reissuing cards with updated features and charge-offs (losses on unpaid cardholder bills). They add that cards help avoid cash-related costs including theft.

Large merchants fare better in the interchange economy than small. Costco Wholesale Corp. switched its co-branded cards in the U.S. from American Express Co. to Visa in part because Visa lowered Costco’s interchange fees on all Visa-branded credit cards close to zero, according to people familiar with the matter.

Few small businesses have that negotiating power. Visa and Mastercard planned to increase interchange fees for many merchants beginning in July, and the changes in some cases would have been the hardest on small businesses, The Wall Street Journal reported. Visa and Mastercard have since said they delayed those changes until next year.

Some merchants bypass cards entirely, but that has become harder during the coronavirus pandemic.

Until it hit, Mississippi Records in Portland, Ore., only accepted cash, and credit-card fees were a big reason why, said owner Eric Isaacson.

The closure of his physical store from mid-March to June, and an 80% drop in revenue, meant that for the first time in his 17 years in business, Mr. Isaacson set up an online store and got a Square Inc. contactless card reader.

“It’s breaking my heart, but I’m doing it, people are so freaked out about money being dirty,” he said.

Mr. Isaacson reopened the store June 13, with only two people allowed inside at a time, wearing masks. The store now accepts both cash and cards, although Mr. Isaacson said he hopes to get rid of card payments at some time in the future.

Card executives say the pandemic shows how cards provide value to consumers and merchants.

Governments in many developed countries, including Australia and much of Europe, have capped credit-card interchange fees. The U.S. only has caps on debit-card fees.

To lower interchange fees, merchants are looking for a way around card networks.

Large retailers, including Walmart Inc. and Target Corp., urged the Fed to develop a real-time payments system as an alternative to card networks.

Separately, more merchants, led by gas stations and supermarkets, are pursuing their own payment apps and other options that lower the stores’ fees.

“Banks have no incentive to curtail [credit-card spending], because they make money on it, obviously airlines make money and merchants make money…so they don’t have an incentive to prevent people from using credit cards,” said Joanna Stavins, an economist at the Boston Fed and a co-author of the 2010 study.

Updated: 7-25-2020

Visa, Mastercard Debit Fees Are Hurting Retailers, Sen. Richard Durbin Says

Senator alleges big networks and issuers are making it hard for merchants to use cheaper card networks.

Democratic Sen. Richard Durbin is asking the Federal Reserve to probe allegedly anticompetitive practices that are forcing merchants to pay excessive debit-card fees levied during the coronavirus crisis by large networks like Visa Inc. and Mastercard Inc.

In a letter to Fed Chairman Jerome Powell, Mr. Durbin said practices by the large card networks and debit-card issuers are diminishing competition in the online payments marketplace and costing merchants potentially billions of dollars. The letter, which Mr. Durbin’s office sent late Friday, asks the Fed to determine whether the major card networks and debit-card issuers have a shared incentive to limit the transactions processed by lesser-known debit-card networks. The Wall Street Journal reviewed a copy of the letter.

The Illinois senator is the namesake of the Durbin amendment, a part of the 2010 Dodd-Frank Act that is best known for capping the swipe fees that merchants pay large banks when customers shop with debit cards. But it also requires that merchants have the ability to choose from at least two unaffiliated debit-card networks to route transactions. Some debit-card issuers appear to be violating that part, Mr. Durbin wrote. He didn’t name any specific banks or other card issuers.

“U.S. retailers and restaurants cannot afford to pay unnecessarily high fees for debit card transactions at a time when they have been hit hard by the pandemic and its economic effects,” said the letter, which was also signed by Rep. Peter Welch (D., Vt.).

The pandemic has also changed consumers’ payment preferences, and that in itself has caused some businesses to pay higher fees. More card purchases are occurring online and with digital wallets. Payments in stores are also shifting to cards that are tapped at stores’ payments terminals rather than inserted, as people try to avoid touching surfaces.

Merchants in recent years have said that these types of purchases limit their ability to route debit-card transactions on networks beyond Visa and Mastercard when those brands are on the front of the card. They have said that they often incur higher network fees as a result, compared with what they would generally pay on lesser-known networks like Shazam or NYCE.

From March through early May, online and other card-not-present debit-card purchases made up an estimated average of 24% of total U.S. debit- and credit-card payments, according to CMSPI, a merchants’ payments consulting firm. That was up from 14% as of Feb. 28.

“What was an issue beforehand is a real big issue now,” said Callum Godwin, chief economist at CMSPI.

The letter called Visa and Mastercard a “card network duopoly.”

Visa declined to comment. A Mastercard spokesman declined to comment, saying he hadn’t seen the letter.

Merchants do have routing choices, said Jeff Tassey, board chairman of the Electronic Payments Coalition, which represents card networks and issuers. “There’s nothing to suggest anyone isn’t fully adhering to the debit marketplace rules,” he said.

During the pandemic, online and contactless payments have helped small businesses to stay open, he said.

“Independent PIN debit networks failed to innovate and make the necessary investments in technology,” he said. “Now, at a time of rapid change and disruption, [they] are asking the government to force the transfer of intellectual property…developed through substantial investments by the payment networks and financial institutions.”

“Simply put, the independent PIN debit networks want to access the full benefits of the advanced payment networks, and merchants want to pay the cheaper PIN debit prices for those benefits.”

The Fed has received the letter and plans to respond, a spokesman said Friday.

Merchant trade groups, including the National Retail Federation, the National Association of Convenience Stores and FMI, which represents the food industry, in recent months have been speaking with congressional members’ offices about the issue, according to people familiar with the matter. Merchant lawyers and trade groups say both networks and issuers have played a role in the routing restrictions.

Most networks beyond Visa and Mastercard are so-called PIN debit networks. When consumers shop in stores and type in their PIN at checkout, those transactions generally travel over a PIN network.

Online purchases are harder to route this way. Few merchants use technology that lets shoppers input their PIN online. Also, some issuers haven’t enabled PINless functionality on their debit cards.

That functionality would allow debit transactions to be processed with PIN networks without the need for the cardholder to type in their PIN. When that functionality isn’t turned on, the transaction will usually automatically go through Visa and Mastercard. The absence of fully available PINless functionality costs U.S. merchants at least $2 billion a year in debit fees, according to CMSPI.

The letter said Fed intervention might be necessary “to prevent what appears to be the anticompetitive practice of major debit card issuers refusing to enable PINless debit functionality on their cards.”

Debit-card purchases on mobile wallets are also hard to route over other networks. Those generally involve tokens that are created by major networks that replace a card’s number when a payment gets processed.

Those networks can translate the tokens back into the actual account number to allow for the purchase to proceed. Merchants can send those payments to the PIN debit networks, but those networks then have to contact the major network, like Visa, on the front of the card to decode the token. Merchants and some smaller networks say the process isn’t easy to execute.

Network fees that merchants pay for online debit-card transactions average an estimated 0.28 percentage points compared with 0.20 points when a debit card is presented at checkout, according to CMSPI.

Purchases With Plastic Get,Purchases With Plastic Get,Purchases With Plastic Get,Purchases With Plastic Get,Purchases With Plastic Get,Purchases With Plastic Get,Purchases With Plastic Get,Purchases With Plastic Get,Purchases With Plastic Get,Purchases With Plastic Get,Purchases With Plastic Get,Purchases With Plastic Get,Purchases With Plastic Get,Purchases With Plastic Get,Purchases With Plastic Get,Purchases With Plastic Get,Purchases With Plastic Get,Purchases With Plastic Get,Purchases With Plastic Get,Purchases With Plastic Get,Purchases With Plastic Get,Purchases With Plastic Get,Purchases With Plastic Get,Purchases With Plastic Get,

Leave a Reply

You must be logged in to post a comment.