An $809 Car Payment, A $660 Income: What Could Go Wrong?

Some dealerships are dressing up borrowers’ car-loan applications with fake, inflated incomes.When Mirna López bought a used 2018 Nissan Pathfinder in May, she got a car loan with a monthly payment of $809. Her monthly earnings were about $660. An $809 Car Payment, A $660 Income: What Could Go Wrong?

Normally, lenders wouldn’t approve that. But an employee at Mac Mitsubishi, a dealership in West Hartford, Conn., filled out her loan application and stated she made $7,833 a month, according to Ms. López and a copy reviewed by The Wall Street Journal. Ms. López, 65 years old, said she didn’t realize that until months later.

Consumers are facing rising prices for cars and trucks, and relying on debt to buy them. Inflating a borrower’s earnings can allow a dealership to close a loan that otherwise wouldn’t happen.

Some dealerships around the country are dressing up car-loan applications with fake, inflated incomes, according to consumer lawyers who say it is a growing issue. Certain large lenders have cut back on some safeguards that could catch the forged applications, in much the same way some mortgage lenders stopped double-checking applications in the run-up to the financial crisis. Federal and state authorities have sued dealerships and lenders over these practices.

Sometimes, borrowers lie about their earnings. But some dealerships concoct numbers without telling the customers, according to lawsuits and interviews with customers and lawyers. Those borrowers often default on their loans within a few months, destroying their credit.

“The consequence for a lot of people is to ruin them financially for five to 10 years,” said Richard Feferman, a New Mexico lawyer who has sued dealerships and lenders in nearly two dozen such cases.

The scope of false applications is hard to quantify. PointPredictive, which sells software to detect loan fraud, estimates that more than a fifth of auto loans have inflated incomes. The company examined loans made over the past four years where lenders obtained borrowers’ personal records, and compared those with the income stated on applications. Its data can’t distinguish who is responsible.

Dealers and lenders can ask borrowers to provide documents such as W-2s or pay stubs. Over the past few years, though, some subprime lenders have stopped checking for them, according to S&P Global Ratings, partly in response to dealers demanding faster decisions.

Auto lenders verified income on about 7% of their loans on average since 2017, according to a Journal analysis.

The share of loans going delinquent soon after they are made is rising, particularly among subprime loans, according to credit-reporting firm TransUnion. That can be a signal of fraud, said Satyan Merchant, senior vice president of TransUnion’s auto business.

U.S. consumers held a record $1.3 trillion of debt tied to their cars at the end of September, according to the Federal Reserve Bank of New York, up from about $740 billion a decade earlier.

Buyers visiting a dealership typically disclose their income to a salesperson or an employee in the financing office. The dealership electronically sends a loan application to banks, credit unions and the finance arms of car manufacturers, which decide whether to fund the loan.

The problem loans often start with borrowers making bad decisions about what they can afford. Sometimes, borrowers don’t read their loan application or final contract.

But dealerships can compound the trouble. They can rush borrowers through the process or show them only a partial copy of the application, according to lawsuits and consumers. Sometimes, dealerships will fill out one application with correct information and submit an incorrect one to lenders. Some borrowers, including Ms. López, said their dealership told them they could return in a few months and refinance into a lower-interest loan, only to tell them later it wasn’t an option.

Dealerships now make more money arranging financing than selling vehicles. If a car loan goes bad, it isn’t usually the dealership on the hook. When a borrower defaults, the lender can repossess the car and try to resell it. Often, though, that isn’t enough to cover the borrower’s unpaid balance, and the lender can write off the loss and can send the borrower to collections.

The National Automobile Dealers Association, a trade group, said lenders can make dealers buy back a loan if they can prove the dealer committed fraud. A spokesman for the group said there is no evidence that income fabrication is a systemic problem.

The Consumer Financial Protection Bureau oversees auto lenders but not dealerships. The Federal Trade Commission last year accused dealerships in Arizona and New Mexico of making up car buyers’ incomes. Attorneys general in Delaware and Massachusetts fined Santander Consumer USA Holdings Inc. in 2017 for allegedly failing to catch income fraud at dealerships, but didn’t charge the dealerships.

General Motors Co. ’s AmeriCredit arm verified incomes on as much as roughly 70% of loans in some bond pools, according to the Journal analysis. The auto financing arms of CarMax Inc. and Ally Financial Inc. verified income on less than 1%. Some of the lenders said income verification is just one of many ways to catch potential fraud and that they have other safeguards.

The Journal analysis encompassed more than 6 million prime and subprime loans that were packaged into bonds and sold to investors by 10 lenders that disclosed such data through Finsight, which tracks bond deals.

Ms. López’s husband, Ramón, spoke with the bank that held her loan a few months after she got it. It was then she found out her application was wrong, she said. The Lópezes’ monthly earnings are still far below the income stated on the application even if Mr. López’s earnings and other income are factored in.

Ms. López said she didn’t closely inspect the application at the dealership because the financing office told her to sign quickly and took back the paper. Ms. López speaks little English, the language on the application.

This month, at her attorney’s advice, Ms. López left the car at the dealership one night after it closed. Her attorney sent a letter to the dealership and the bank stating she is revoking acceptance of the car due to fraud.

A lawyer for the dealership said Ms. López’s allegations aren’t consistent with the company’s business practices. A spokesman for the bank, BB&T Corp. , said it couldn’t comment on a customer but that it would terminate its relationship with any dealership where it found “a pattern of false loan applications.” BB&T has since been renamed Truist Financial Corp.

Grace Pazdan, an attorney at Vermont Legal Aid Inc., said she has had a number of clients whose car-loan applications contained inflated income. She is trying to advance state legislation that would require dealerships to provide buyers with their full loan application at the time of purchase.

Baxter Hansen of Gastonia, N.C., has been paying $493 a month for a Kia Sportage she bought new two years ago.

Ms. Hansen, 67, said she didn’t know her application said she had a monthly income of $4,800. Ms. Hansen, a stay-at-home parent for most of her life, had close to no income at the time. She is suing the dealership.

Capital One Financial Corp. , which approved her for a $28,000 loan, said it encourages customers who are facing financial difficulties to ask the bank for assistance. A lawyer for the dealership, Kia of Gastonia, and the former owner didn’t return calls for comment.

Ms. Hansen started working at Walmart. She says she hopes to pay off the loan in about 3½ years.

Updated: 2-15-2020

Dealerships Give Car Buyers Some Advice: Just Stop Paying Your Loan

Car sellers are telling hard-up borrowers to have their old cars voluntarily repossessed. Lenders and borrowers are losing out.

Joyce Parks was struggling to afford her Kia 000270 0.97% Soul when, she says, the dealership where she had bought it pitched her an unconventional idea: Stop making the payments.

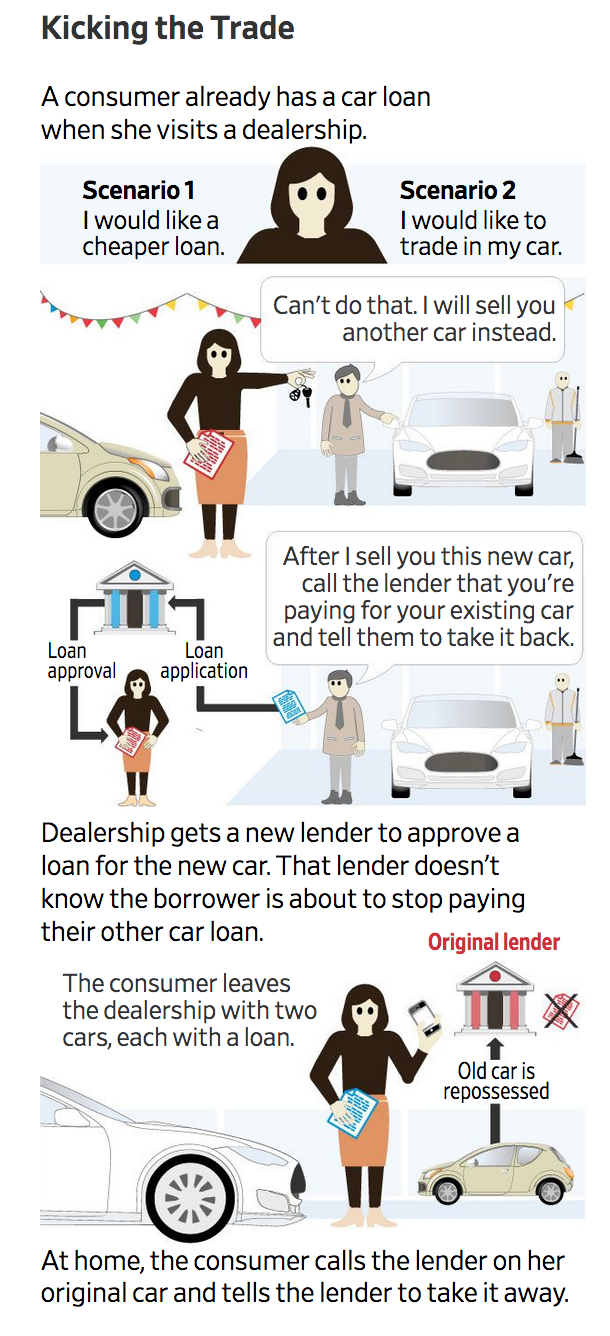

Ms. Parks, 63, says employees told her that she couldn’t trade in the Soul, but that she could buy another car. To get rid of the Soul, the dealership told her, she should have the lender repossess it, Ms. Parks said.

The trade-in, where a buyer hands a car back to a dealership and uses it as credit toward another one, is often a crucial step in car buying. But some dealerships are instead telling buyers to give their old cars back to their lenders—and selling them new ones—in a practice known as “kicking the trade.”

It is difficult to estimate how often this happens. Auto-sales veterans say the practice is an open secret in some showrooms. Broadly, vehicles are getting more expensive and Americans are struggling to afford them. Dealerships now make more money arranging financing than selling vehicles. If a car loan goes bad, it typically isn’t the dealership on the hook—it is the borrower or lender.

The National Automobile Dealers Association said there is no evidence to suggest “kicking the trade” is prevalent. Dealerships “could not sustain carefully cultivated relationships” with lenders “if they were to engage in the type of behavior alleged,” a spokesman said.

Consumer lawyers say they have seen more such cases. Five years ago, “it happened two or three times per year,” said Daniel Blinn, a Connecticut-based attorney who has sued dealerships and auto lenders. “Now, we hear it at least once per month.”

Credit-reporting firm TransUnion calculates that nearly 24 million U.S. vehicle loans were originated in 2018. About 300,000 of those vehicles were repossessed within 12 months, up 17% from 2014. Such a quick souring of the loan can be a signal of some sort of auto fraud.

Roughly a fifth of people who have had a car repossessed over the last several years take out another auto loan within a year of the repossession, TransUnion says.

Dealerships typically don’t make loans. When consumers need financing, a dealership electronically sends their loan applications to banks, credit unions and other lenders. They, in turn, decide whether to fund the loan.

Problems often begin with consumers who buy cars they can’t afford or sign loans they don’t understand. But dealerships can compound the trouble. Some dealerships are inflating borrowers’ incomes on loan applications so they can sell them bigger or more expensive cars, according to lawsuits and interviews.

When dealerships kick the trade, they typically get a lender to approve a loan for the buyer’s new vehicle. Next, the buyer generally goes home with two vehicles and two loans. It is only then the buyer asks the original lender to repossess the original car.

Connex Credit Union sued Connecticut dealership Barberino Nissan in 2016, alleging the dealership “repeatedly told customers to just deliver the keys to Connex.” Barberino denied the accusations but agreed to a settlement roughly a year ago, according to the dealership’s lawyer.

Lenders generally say they will cut ties with dealerships that do this. Often, though, the lenders aren’t aware it is happening.

Ms. Parks, a former dietary aide in Gastonia, N.C., said she told dealership employees she couldn’t afford the used Nissan Rogue they wanted her to buy. She said she signed a bank loan for it because she felt out of options.

Ms. Parks then told Kia Motors Finance, the lender on her Soul, she wanted to return it. The dealership told her not to mention she had just bought another car, she said.

After a few months, Ms. Parks couldn’t make the payments on the Rogue either. It was repossessed too.

Ms. Parks now drives a used Nissan Murano her family bought her. Her credit score has plunged. She owes at least $15,000 on the Soul and Rogue, according to her credit report.

She is suing the dealership, Kia of Gastonia. It shut down last year. A lawyer for the dealership didn’t return requests for comment.

When a lender takes back a vehicle, it typically tries to sell it, but that is often not enough to cover the outstanding loan. Sometimes borrowers don’t realize they are responsible for their remaining debt even after they get rid of the vehicle tied to it.

Perla Amante of Hawthorne, Calif., struggled to pay for her Kia Sorento after her husband died in 2018. At her dealership’s instructions, she said, she signed a loan for a Kia Forte and then called the Sorento’s lender, Ally Financial Inc., to say she no longer wanted it.

Ally told her she would be billed for the amount left over after Ally resold the car. Ms. Amante, 70, a retiree who worked in customer service, said the dealership hadn’t mentioned this risk. She contacted a lawyer, who got the dealership to take back the Forte.

When Whitney Davis’s Hyundai Sonata was having mechanical problems in 2016, she returned to the Connecticut dealership where she bought it used.

The dealership told her it would take the car and sell her another one, she said. But after she signed a loan for a used Nissan Altima, she was told she couldn’t trade in the Sonata, she said. When she explained she couldn’t afford two car loans, an employee told her to have the Sonata’s lender take it back, she said.

“He made it seem like it was something they deal with a lot,” said Ms. Davis, who is 29 and an office manager.

The Sonata’s lender took back the vehicle and soon informed Ms. Davis she still owed nearly $9,000. Her credit score plummeted.

An owner of the dealership, Car Nation in Middletown, Conn., pleaded guilty in federal court in December to a charge related to giving false information about loan applicants to auto lenders. Trent LaLima, an attorney for the owner, said his client didn’t cheat any car buyers and “would never have tolerated any such activity.”

The dealership has shut down. An attorney for the dealership disputed Ms. Davis’s account but wouldn’t give details.

Ms. Davis recently got a loan for a used Jeep Grand Cherokee.

Related Articles:

Christianity Today — Founded By Billy Graham — Calls For President Trump To Be Removed From Office

Big Banks Prepare Living Wills Or Emergency Liquidation Plans (#GotBitcoin?)

Federal Reserve To Let Inflation Run “Hot” Going Into Next Recession (#GotBitcoin?)

Steyer Buys Trump Slogan URL “Keep America Great” On Cyber Monday

Body Of FBI Agent Found In Ukrainian Village

Trump Fails To Convince Investors To Place $3.4 Trillion Into Stocks (#GotBitcoin?)

Trump’s LACK Of Infrastructure Investment Is Putting American’s Lives At Risk (#GotBitcoin?)

Cost of Infrastructure Fixes Is Going Up While Trump Procrastinates (#GotBitcoin?)

Trump Administration To Try Again To Fulfill Infrastructure Pledge (#GotBitcoin?)

China Outspends US When It Comes To Building The World’s Infrastructure (#GotBitcoin?)

U.S. Factories Contract As Does Small Business And Global Firms

Historic Asset Boom Passes By Half Of Families (#GotBitcoin?)

Parts Of America Are Already In Recession (#GotBitcoin?)

A Manufacturing Recession Is Here. Now What? (#GotBitcoin?)

Argentina’s Economy Is In A Technical Default (#GotBitcoin?)

Trump Blames Business Setbacks On Incompetency Vs Recession He’s Causing (#GotBitcoin?)

India’s Spending Spree Slows As Debt Problems Become More Widespread (#GotBitcoin?)

Home-Price Growth Slows To Levels Not Seen Since 2008 (#GotBitcoin?)

Trump Claims “Billions” In Trade Tariffs While Diverting Hurricane Relief Funds For Border Detention

Bond Yields Sink To New Lows, Federal Deficits Skyrocket And Trump Back-Tracks On Tax Cuts

What Are YOU Doing NOW To Prepare For The Incoming Recession? (#GotBitcoin?)

Trump And Publicans Will Have Zero Chance Of Re-Election During Coming Recession

Majority Of Americans Stressed Over Being In A Mass Shooting – Trump To Blame?

As Global Order Crumbles, Risks Of Recession Grows (#GotBitcoin?)

U.S. Mortgage Debt Hits Record, Eclipsing 2008 Peak

U.S. Stocks & Treasuries Flash Recession/Depression #GotBitcoin?

Investors Ponder Negative Bond Yields In The U.S. (#GotBitcoin?)

Lower Mortgage Rates Aren’t Likely To Reverse Sagging Home Sales (#GotBitcoin?)

Financial Crisis Yields A Generation Of Renters (#GotBitcoin?)

Global Manufacturing Recession Weighs On US Economy (#GotBitcoin?)

Falling Real Yields (0.241% ) Signal Worry Over U.S. Economy (#GotBitcoin?)

Donald Trump’s WH Projects $1 Trillion Deficit For 2019 (#GotBitcoin?)

U.S. Home Sales Stumble, As Pricey West Coast Markets Suffer Declines (#DumpTrump)

Lower Rates Have A Downside For Bank’s Mortgage-Servicing Rights (#GotBitcoin?)

Central Banks Are In Sync On Need For Fresh Stimulus (#GotBitcoin?)

Weak Corporate Earnings Signal A Weak Economy (#GotBitcoin?)

Price of Gold, Indicator Of Inflation And Recession Surges (#GotBitcoin?)

Recession Set To Materialize In Approximately In (9) Months (#GotBitcoin?)

A Whiff Of U.S. Recession Is In The Air Again. Credit Trumponomics

Trump Calls On Fed To Cut Interest Rates, Resume Bond-Buying To Stimulate Growth (#GotBitcoin?)

Fake News: A Perfectly Good Retail Sales Report (#GotBitcoin?)

Anticipating A Recession, Trump Points Fingers At Fed Chairman Powell (#GotBitcoin?)

Affordable Housing Crisis Spreads Throughout World (#GotBitcoin?) (#GotBitcoin?)

Los Angeles And Other Cities Stash Money To Prepare For A Recession (#GotBitcoin?)

Recession Is Looming, or Not. Here’s How To Know (#GotBitcoin?)

How Will Bitcoin Behave During A Recession? (#GotBitcoin?)

Many U.S. Financial Officers Think a Recession Will Hit Next Year (#GotBitcoin?)

Definite Signs of An Imminent Recession (#GotBitcoin?)

What A Recession Could Mean for Women’s Unemployment (#GotBitcoin?)

Investors Run Out of Options As Bitcoin, Stocks, Bonds, Oil Cave To Recession Fears (#GotBitcoin?)

Goldman Is Looking To Reduce “Marcus” Lending Goal On Credit (Recession) Caution (#GotBitcoin?)

Leave a Reply

You must be logged in to post a comment.