New Risk To World Economy: Synchronized Housing Slowdown (#GotBitcoin?)

Global growth in home prices slows as world-wide residential investment continues to decline. New Risk To World Economy: Synchronized Housing Slowdown (#GotBitcoin?)

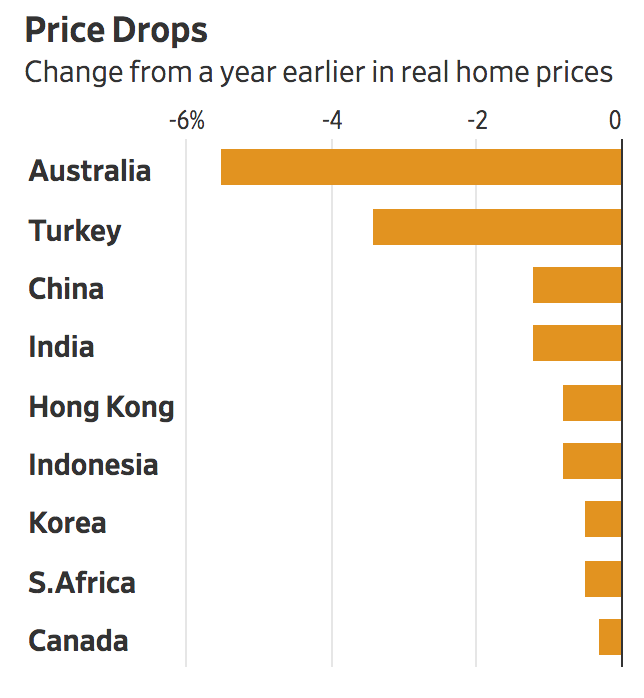

Housing markets across the world, from the U.K. to China to Australia, are losing steam, holding back prospects for the global economy that last year grew at its slowest rate since the financial crisis.

Across 23 countries, an index of inflation-adjusted home prices compiled by the Federal Reserve Bank of Dallas grew 1.8% in the third quarter of 2019 from a year earlier, down from a recent peak of 4.3% in 2016, according to an Oxford Economics analysis. In 18 large economies, world-wide residential investment dropped on a year-over-year basis for four consecutive quarters through September, the longest stretch of declines since the 2008-09 crisis, according to Oxford Economics’ analysis of national accounts.

Related:

Emergency Rental Assistance Program

Home Flippers Pulled Out of U.S. Housing Market As Prices Surged

Housing Insecurity Is Now A Concern In Addition To Food Insecurity

Smart Wall Street Money Builds Homes Only To Rent Them Out (#GotBitcoin)

No Grave Dancing For Sam Zell Now. He’s Paying Up For Hot Properties

Investors Are Buying More of The U.S. Housing Market Than Ever Before (#GotBitcoin)

Cracks In The Housing Market Are Starting To Show

Biden Lays Out His Blueprint For Fair Housing

Housing Boom Brings A Shortage Of Land To Build New Homes

Wave of Hispanic Buyers Boosts U.S. Housing Market (#GotBitcoin?)

Phoenix Provides Us A Glimpse Into Future Of Housing (#GotBitcoin?)

OK, Computer: How Much Is My House Worth? (#GotBitcoin?)

Sell Your Home With A Realtor Or An Algorithm? (#GotBitcoin?)

A key catalyst is the global slowdown over the past two years that kept a lid on housing demand and home-price gains. In large cities, affordability constraints are deterring many would-be buyers, and foreigners’ appetite for overseas properties has cooled. Heightened uncertainty, for example over the U.S. trade war with China, Brexit and protests in Hong Kong, continue to weigh on home-buyer sentiment.

“It matters because…the housing market is a big asset market which has quite large potential impacts on consumer spending,” said Adam Slater, an economist at Oxford Economics. “It tends to be a sector when it booms, it booms; when it busts, it busts.”

The slowdown isn’t flashing signs of turning into a bust. That largely hinges on global growth and uncertainty. The International Monetary Fund on Jan. 20 projected global growth would improve from 2.9% last year to 3.3% this year and 3.4% next, though that is still below the postcrisis average.

Even though homes aren’t tradable, like soybeans or car parts, home prices across the world have become increasingly synchronized. This reflects a variety of factors, according to the IMF, including the increasing tendency for economic growth and interest rates to move in parallel across nations.

For global cities like New York, London and Vancouver, Canada, another factor is at work, according to the IMF. In the period of low interest rates following the global financial crisis, wealthy investors in the hunt for better yields swooped in to buy properties in major financial hubs. In effect, residential prices in those cities have become globally synchronized much as stocks and bonds are.

Now, home prices in large cities are pulling back, according to an index of high-end markets in 45 cities maintained by Knight Frank, a London-based real-estate consulting firm. The index grew 1.1% in the third quarter of 2019 from a year earlier, down from 3.4% in the same period in 2018 and 4.2% in 2017.

Lower housing investment directly subtracts from gross domestic product growth. Oxford Economics estimates that the housing slowdown cut growth in advanced economies by 0.3 percentage point between 2017 and 2019.

Homes, like stocks, are a part of consumers’ overall wealth, meaning the housing slowdown, in turn, could further eat away at global growth if homeowners feel less well-off and curb their spending. This appears to have materialized in some nations. Spending growth in Canada and Sweden slowed by more than 1 percentage point in 2018 as home prices declined, the Bank for International Settlements said in its 2019 annual report.

A flurry of property-market regulations is another factor chilling home-price gains. Vancouver introduced a foreign buyer tax of 15% in 2016 and raised it to 20% in 2018. Seoul tightened mortgage regulations and announced a price cap on residences. New Zealand banned overseas investors from buying existing homes in 2018.

Cooling home prices could have a positive effect: Pricey markets could become more affordable and make a collapse in the property market less likely.

The current slowdown looks different from the lead-up to the 2008-09 crisis, when a global credit boom went bust and real home prices declined as much as 6.6% across the world’s major economies, according to Oxford Economics. Policy makers are more alert to the risks of housing bubbles, and banks have made it more difficult to access mortgages. Though rising household debt presents risks in some countries, BIS said that in many nations at the center of the crisis, household debt-to-GDP ratios are below precrisis levels.

Home prices are outpacing income gains in many countries, but not by nearly as much as in the precrisis years, said Enrique Martínez-García, an economist at the Dallas Federal Reserve. “The housing market is not giving us red signals of danger as it did,” Mr. Martínez-García said.

Should the slowdown turn into a more serious bust, it would test central banks, many of which cut interest rates last year to buffer their economies. In theory, interest-rate cuts should spur demand for housing by making mortgages cheaper. That appears to have happened—to an extent—in the U.S. Since the Federal Reserve cut interest rates last summer, U.S. home buying is up. But, interest rates around the globe are near record lows. Mr. Martínez-García said there is a point at which lowering long-term interest rates can no longer effectively prop up residential investment. “We might be reaching that point,” he said.

And lower interest rates may be less effective given long-run restraints on housing such as the slower global growth expected over the next few years, property regulations and declining fertility rates. Supply is constrained in many cities where workers want to live. These factors are common to many countries, another reason the housing market is now globally synchronized. New Risk To World,New Risk To World,New Risk To World,New Risk To World,New Risk To World,New Risk To World

Related Articles:

Wave of Hispanic Buyers Boosts U.S. Housing Market (#GotBitcoin?)

Smart-Home Tech As A Selling Point, Not A Cost Cutter

Condo Conversions Near The End, A Casualty Of Rent Reform (#GotBitcoin?)

This Startup Wants To Sell You A Slice of A Rental Home (#GotBitcoin?)

Realtors And Developers Are Selling Wellness, Whether It Works or Not (#GotBitcoin?)

Uber Drivers Seek Extra Cash Working For House Flippers (#GotBitcoin?)

What’s Rent To Own & How Does It Work? A Guide To Renting Vs Buying

San Francisco’s Housing Market Braces For An IPO Millionaire Wave (#GotBitcoin?)

Affordable Housing Crisis Spreads Throughout World (#GotBitcoin?) (#GotBitcoin?)

Home Prices Continue To Lose Momentum (#GotBitcoin?)

Freddie Mac Joins Rental-Home Boom (#GotBitcoin?)

Retreat of Smaller Lenders Adds to Pressure on Housing (#GotBitcoin?)

OK, Computer: How Much Is My House Worth? (#GotBitcoin?)

Borrowers Are Tapping Their Homes for Cash, Even As Rates Rise (#GotBitcoin?)

‘I Can Be the Bank’: Individual Investors Buy Busted Mortgages (#GotBitcoin?)

Why The Home May Be The Assisted-Living Facility of The Future (#GotBitcoin?)

Leave a Reply

You must be logged in to post a comment.