A Hedge Fund Makes Billions Off Americans’ Underwater Mortgages (#GotBitcoin?)

Fir Tree bet that homeowners would keep paying loans, even against their interest. A Hedge Fund Makes Billions Off Americans’ Underwater Mortgages

Fortunes were made on Wall Street betting against sketchy mortgages before the housing bust a decade ago. In its aftermath, one firm has made billions taking the other side of that trade, scooping up battered home loans in a wager that plenty of Americans would keep paying them.

The payoff, years in the making for hedge-fund firm Fir Tree, is $2.6 billion and counting, according to an investor letter reviewed by The Wall Street Journal.

Fir Tree has reached the final stages of collecting on its gambit at a time when the housing market is at a crossroads following five years of sharp gains. In many cities, surging prices have strained affordability, while rising interest rates and high student-loan debt have made it difficult for the generation starting families to buy homes.

Fir Tree, which manages about $8 billion, favors complex trades that often involve legal action. It is a creditor in the decade-old battle over what is left of failed investment bank Lehman Brothers, has spent years trying to wring cash from Puerto Rico’s defaulted bonds and, during the recent oil bust, emerged from bankruptcy court holding the reins of energy producers.

Its mortgage wager was two-pronged: The firm relied on human nature—a belief that homeowners would stick with their mortgages, even if their houses were no longer worth what they owed—while it also took legal action to force banks to pay up for flawed loans that did default. So far, about half of the firm’s $2.6 billion profit is attributable to homeowners paying underwater mortgages. The rest has been redress for loans that defaulted, according to people familiar with the matter.

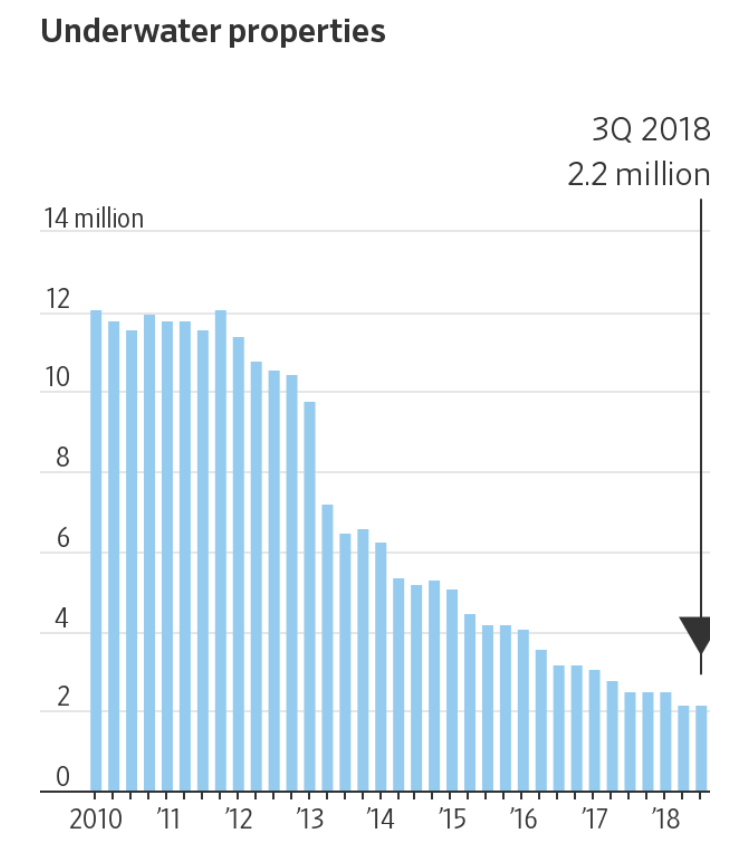

In 2010, at the depths of the crash, more than 12 million U.S. houses were worth less than the debt on them. In places like Las Vegas and Miami, about two of every three mortgaged homes were underwater.

Up From Underwater

Years of mortgage payments and rising property values have reduced the number of U.S. homes worth less than their debt.

Many investors feared homeowners who had paid top dollar before the bust or borrowed against properties at inflated values would soon default. It wasn’t hard to see why. Academics and lawyers argued many underwater homeowners should strategically default, especially if staying put imperiled their long-term financial health.

At the time, Fir Tree was looking to play the crash. It had been among those who bet on a mortgage meltdown and profited when the market imploded.

The firm noticed that panicked investors were dumping bonds packed with second mortgages. Those debts have secondary claims to properties that are collateral for first mortgages. If a property has lost value when the borrower defaults, there may be no value left once the first mortgage is paid.

Clinton Biondo, one of Fir Tree’s managing partners, said the firm figured the securities selling for cents on the dollar were so cheap, it could still break even if most of the loans defaulted.

It probably wouldn’t come to that, though. Fir Tree believed many Americans would pay regardless of the value of their house. “Even highly distressed borrowers pay off their obligations since they care about their credit,” Mr. Biondo said in an interview.

By 2013 Fir Tree, at a cost of about $1 billion, had acquired second-lien bonds with a face value of roughly $9 billion, according to people familiar with the matter.

For the most part, Fir Tree was right about borrowers. “People don’t walk away,” said Brent White, a University of Arizona law professor who advocated for strategic default. “They’ll say, ‘I made a promise to pay this mortgage and I’m going to keep this promise and it’s immoral not to.’”

He estimated in a 2010 paper that only about 3% of borrowers who could afford their mortgages walked away.

Al Wojtowicz was one of the 97% who stayed put—even when the value of his suburban Chicago townhouse halved to about $150,000. Making matters worse, the builder of his neighborhood went belly up before finishing it.

Yet Mr. Wojtowicz and his wife were employed—he’s a financial planner, she’s a physical therapist—and the home fit the family even after their second child was born. The couple reworked their loan through a government program to pay down more principal and a new builder eventually arrived to finish the neighborhood.

“It exacerbated the problem when people walked away,” Mr. Wojtowicz said.

In Mission Viejo, Calif., Cristie Connors and her husband were floored when the house across the street sold for $525,000. Theirs was smaller and they had paid $715,000. California law let them drop the keys in the mailbox and move without worrying about the bank coming after them.

“We looked at each other and said, ‘Are we crazy not to walk away? Where would we live?” she said

A bookkeeper, Ms. Connors crunched the numbers and decided renting wasn’t worth it once the mortgage-interest tax deduction for their California-sized loan was considered. “It didn’t make sense to put our family through the stress of moving,” she said.

The same thinking held sway with millions of other Americans who had both first and second mortgages. At Fir Tree, that meant interest payments were made on the bonds it held and they rose in value.

The firm’s gains didn’t stop there. It also went after banks over bad loans.

Big chunks of particular bonds Fir Tree owned gave it contractual rights to pursue banks that bundled flawed loans into bonds. It also approached the firms that had insured the bonds against losses.

Fir Tree enlisted a former mortgage originator to help it to mine tens of thousands of loan files for missing documents, misstatements and outright whoppers—like the self-employed window washer who declared annual income of $12,907 in a bankruptcy filing but was said to earn $78,528 on the application for an unpaid mortgage that had been tucked into a 2006 bond.

The window washer was offered as evidence in a case that resulted in an undisclosed settlement between Fir Tree and one of 14 banks from which it has squeezed restitution.

Related Articles:

‘I Can Be the Bank’: Individual Investors Buy Busted Mortgages (#GotBitcoin?)

OK, Computer: How Much Is My House Worth? (#GotBitcoin?)

The U.S. Housing Boom Is Coming To An End, Starting In Dallas (#GotBitcoin?)

Home Prices Continue To Lose Momentum (#GotBitcoin?)

Freddie Mac Joins Rental-Home Boom (#GotBitcoin?)

Retreat of Smaller Lenders Adds to Pressure on Housing (#GotBitcoin?)

Borrowers Are Tapping Their Homes for Cash, Even As Rates Rise (#GotBitcoin?)

Why The Home May Be The Assisted-Living Facility of The Future (#GotBitcoin?)

Your questions and comments are greatly appreciated.

Monty H. & Carolyn A.

Leave a Reply

You must be logged in to post a comment.