Scamming Grandma: Financial Abuse of Seniors Hits Record

A federal law enacted in May allows bank employees to report suspected cases of elder financial abuse to police and adult protective services. Scamming Grandma: Financial Abuse of Seniors Hits Record

Related:

Ultimate Resource For Money Laundering, Spoofing, Market-Rigging, Etc. In Banking Industry

Morgan Stanley To Pay $10M For Anti-Money Laundering Failures

JPMorgan To Pay $290 Million to Settle Jeffrey Epstein Accusers’ Suit

JP Morgan’s (Jamie Dimon’s) Total Fines/Settlements ($35 Billion And Counting)

Europe Goes Harder on Money Laundering With Record ING Fine

Money-Laundering Is Completely Out-Of-Control In Traditional Finance/Banking Industry

France Moves To Ban Anonymous Crypto Accounts To Prevent Money Laundering

The Money Laundering Hub On the U.S. Border? It’s Canada!

SEC And DOJ Charges Lobbying Kingpin Jack Abramoff And Associate For Money Laundering

Banks report 12% increase of suspected cases as they step up efforts to detect and stop fraud. Scamming Grandma: Financial Abuse of Seniors Hits Record

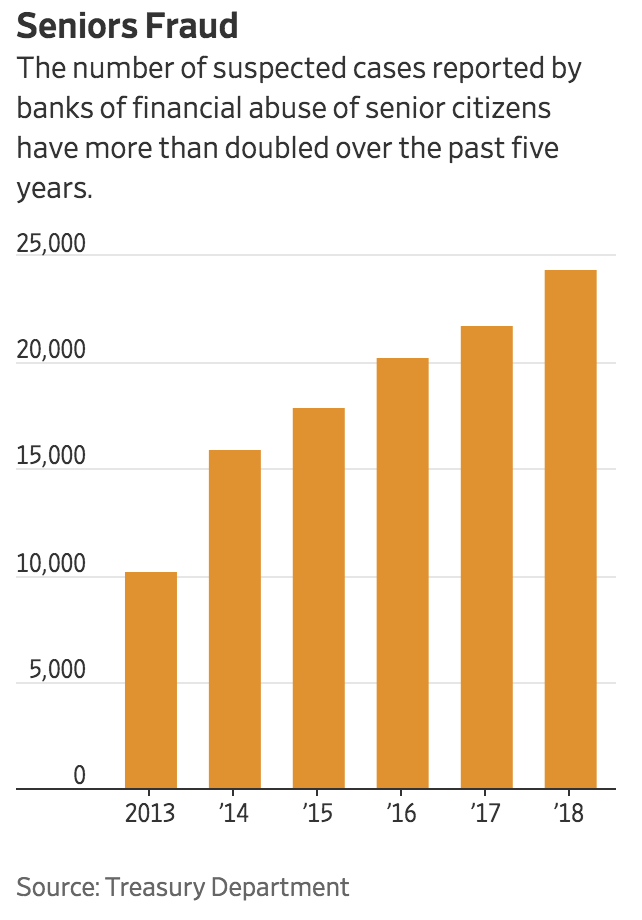

U.S. banks reported a record 24,454 suspected cases of elder financial abuse to the Treasury Department last year, more than double the amount five years earlier, according to government data.

The increase occurred as new federal and state laws are prompting banks to take a more active role in trying to address frauds and scams that target older customers. For their part, banks are beefing up training programs for employees on how to detect, stop and report issues without violating a customer’s privacy. Employees are even learning to recognize early signs of cognitive decline.

The issue of elder financial abuse is likely to grow even more pronounced. An average of 10,000 Americans turn 65 a day, a pace expected to continue through 2030. In that year, one in every five people will be 65 or older, according to the U.S. Census Bureau.

Meanwhile, people over 50 represent one-third of the population but account for 61% of bank accounts and 70% of bank deposits, according to 2017 research by the American Bankers Association.

“Anything having to do with elder financial abuse or exploitation affects a huge part of our customer base,” said Rob Rowe, associate chief counsel at the American Bankers Association.

The 24,454 suspected cases reported in 2018 is up 12% from 21,839 cases in 2017, the previous record, and more than double the number in 2013, according to Treasury Department data.

Last February, a customer in her late 70s walked into a New Canaan, Conn. branch of People’s United Bank, asking to wire $30,000 to her grandson. The customer said he had been in a car accident while vacationing in Mexico.

Where She Recently Has Been Looking Out For Scams Affecting Elderly Customers.

Suspecting what is known as a “grandchild scam,” Rebecca Reed, an assistant manager, instead suggested the customer call her grandson. It turned out he had been at school all day—not in Mexico.

“We can see it when something is not right,” said Ms. Reed, who has received a Fraud Fighter award from the bank.

Yet elder financial abuse isn’t always so obvious and can raise privacy issues, or risk alienating customers. The delaying or canceling of transactions also could result in customers missing out on legitimate opportunities such as timely investments.

Legislators have tried to address some of these issues. A federal law enacted in May called the Senior Safe Act allows bank employees to report suspected cases of elder financial abuse to police and adult protective services. Some states have gone further: Tennessee and Texas, for instance, allow bank employees to refuse or delay transactions, or notify family members when elderly customers request suspicious money transfers.

Daughter Erika, Lost Over $80,000 In A ‘Grandchild Scam’ Last Year.

Thomas Flavin, a 76-year-old retiree in Watertown, N.Y., was a victim of a grandchild scam last year where a man posing as a lawyer said Mr. Flavin’s grandson needed money to cover bail, legal fees and vehicle repairs after causing a DUI accident in Tennessee, according to his daughter Erika Flavin. He got cash from his bank and sent it by FedEx to New York and Pennsylvania addresses, losing more than $80,000, most of his life savings.

Only later did he find out that there was no DUI and his grandson hadn’t been in an accident. “In a way, it feels like a sad death in the family,” he said in a statement, adding that his banker later said he thought something was fishy but wasn’t allowed to intervene. “If that banker had offered him information about these scams that were going on, things would have turned out very differently,” Ms. Flavin said.

Bankers and senior-citizen advocates say many cases of elder abuse involve family members or caregivers. Other scams use phone calls and emails to trick vulnerable seniors into making irreversible money transfers. Besides the grandchild scam, there are romance or online dating schemes in which victims are deceived into online relationships before being swindled out of their savings.

Bankers attribute an increase in social media use by older Americans for a surge in fraud cases targeting seniors. Others say seniors still have landline numbers listed in phone books, making them an easier target for telephone scammers.

“They might be lonely. They are willing to talk while most of us just have a cellphone or screen out calls,” said Laurel Sykes, senior vice president for Montecito Bank & Trust in California.

Coastal Credit Union in North Carolina now reports an average of one case of elder abuse to the Treasury Department every month, compared with one or two cases a year earlier this decade, says Arlene Babwah, vice president in charge of risk management. The credit union has conducted annual training on senior banking in recent years, and added more sessions this year based on employees’ job functions.

“You might want to train an underwriter or a loan officer to ask, ‘If you are 90 years old, why are you buying a Corvette?’” said Ms. Babwah. “If you notice that an ATM card was used after midnight and you have an 85-year-old customer, that’s a red flag.”

Bankers in some states have more powerful tools than others. A branch employee at First Farmers and Merchants Bank in Tennessee successfully intervened in a theft targeting a customer in her 90s, whose granddaughter was siphoning cash from the woman’s account to cover her drug habit, according to Sam Wantland, the bank’s corporate counsel.

The employee did so by refusing—as permitted by a Tennessee law—to honor a power of attorney the granddaughter produced, freezing the account and notifying another relative. “A lot of times, we know their sons and their daughters. We know who to reach out to and that’s been very helpful,” Mr. Wantland said.

Updated: 1-24-2021

How To Protect Seniors From Online Fraud And Phone Scams

Stay ahead of scammers by blocking their calls, sending their emails to spam and monitoring assets.

Scams targeting older adults take many forms, ranging from callers posing as grandchildren in need of financial assistance to emails directing people to fake bank websites where cons collect login credentials. The techniques evolve every year but the outcome is always the same: Many seniors end up losing money.

The isolation many older adults are experiencing during the pandemic has exacerbated the problem. Technology helps seniors stay connected with loved ones during a time of limited social interactions but it also opens new doors to scammers. Online puppy scams and romance scams are on the rise as bad actors seek to take advantage of people’s loneliness, according to the National Adult Protective Services Association.

Scammers initiated contact with older adults online more often than they did by phone for the first time ever in the second quarter of 2020, according to an October report from the Federal Trade Commission. Phone scams, though, still resulted in the highest monetary losses.

Older adults, defined by the FTC as those age 60 and over, were nearly six times as likely as younger ones to report losing money on tech-support scams. In all, older Americans reported fraud losses totaling $388 million through the third quarter of 2020, the latest data available from the FTC, up 23% from the same period a year earlier.

There are ways to safeguard assets and to prevent such scams from occurring in the first place. Here are some tips, based on interviews with several elder-care experts.

Block Unwanted Phone Calls

In addition to adding a land line or mobile phone number to the National Do Not Call Registry, people also can check with their phone company or mobile provider about call-blocking services. AT&T, T-Mobile and Verizon all offer features for blocking robocalls.

People also can block unwanted calls on the mobile phones themselves: Apple devices running iOS 13 or later can silence unknown callers as can Android devices running Android 6.0 and newer. There are also a number of third-party apps that block robocalls, available on the Apple and Google app stores.

Reduce Electronic And Physical Junk Mail

If you receive something that looks like junk mail in your inbox, it’s best to mark it as spam so your email service’s spam filter recognizes it next time.

Even if an email looks legitimate, it’s always best to check the email address it came from before opening it or clicking on anything in the message. Emails sent from scammers usually contain various numbers or symbols rather than the simple email address of a legitimate institution.

The same goes for web addresses, which also can be spoofed. You can google the name of the bank website where you’ve supposedly been directed to see if it matches.

You can unsubscribe from marketing emails. Cyber safety firm NortonLifeLock shows how to do so on every major email service. When in doubt about an email, ask a trusted loved one, call the Senior Planet tech hotline at 920-666-1959 or call the AARP fraud watch helpline at 877-908-3360.

People also can request not to receive certain kinds of U.S. mail, as well as unwanted commercial email, through a service called DMAchoice. You can opt out of receiving prescreened credit and insurance offers by visiting http://www.optoutprescreen.com.

Elder-care experts suggest that people who receive in-home care switch to electronic bank statements or have their mail forwarded to a trusted loved one to avoid having mail containing account information available for caregivers and others to see.

While technology has invited new scams, most fraud against seniors is still perpetrated by caregivers and family members, according to the Justice Department.

Monitor Your Money

Seniors can safeguard their money by setting up direct deposits for income from Social Security, pensions and dividends so that physical checks aren’t sent to their home, where a caregiver or others could get a hold of them.

People should also keep an eye on spending activity by asking their bank and credit-card companies to send them—or trusted loved ones—alerts of suspicious activity or charges that exceed a certain amount. Most banks allow customers to create custom alerts. You can also lower the credit limit on credit cards to reduce the risk of loss, or use only prepaid cards such as a True Link Visa.

Some financial institutions recommend an app called EverSafe, which monitors bank and investment accounts across institutions and uses an algorithm that analyzes an individual’s spending history to detect changes in behavior, such as late bill payments, changes in interest rates and missed deposits.

It also monitors real-estate assets for title changes and lien filings. The hard part might be preparing yourself to allow a third party access to so much financial information—or persuading an aging parent to do so. The subscription-based service says it doesn’t store account information or enable money transfers through the app.

The app was created by Howard Tischler, a former executive at financial-services and background-check firms whose mother lost her life savings to scammers, and Elizabeth Loewy, former head of the elder-abuse unit in the Manhattan district attorney’s office. Seniors can designate trusted family members, accountants, lawyers and others also to receive alerts without giving them access to account numbers or balances.

Ms. Loewy said it isn’t enough for seniors to monitor their credit reports. “Most cases we saw in the DA’s office did not start in a credit report and, in some cases, the financial abuse never showed up in the credit report,” she said. “For example, if a dormant credit card is stolen and used, that won’t show up in your credit report.”

Consider Hiring A Care Manager

If your aging parents require in-home care and have cognitive problems—especially if you don’t live close enough to check in on them regularly—it’s a good idea to hire a care manager to oversee all aspects of their care.

Care managers are independent of the agency that provides the actual caregiving and act as a liaison between the care recipient, family members and anyone providing help, whether it’s a nurse, the person mowing the lawn or the estate attorney.

Care managers can also advise families on additional steps that should be taken to guard against fraud, such as locking up or removing valuable items from the home.

“The bottom line is to be proactive instead of reactive when it comes to fraud,” said Connie McKenzie, board president of the Aging Life Care Association.

If you suspect that you or a loved one has been the victim of fraud, you can call the National Elder Fraud hotline at 833-372-8311 and report it to the FTC by visiting the agency’s website or calling 877-382-4357.

Updated: 12-30-2024

Bank Insiders (Employees, Contractors And Staff) Are Leaking Data On Gammy’s Accounts As Scams Surge

Meanwhile, bank lobbyists are fending off legislative attempts to force firms to do more to protect customers or share their losses.

Such concerns now carry new urgency. US retirees sitting atop a record stockpile of wealth are facing an onslaught of elder fraud, with estimated annual losses soaring past $28 billion.

For con artists, tips on who has a lot of money can be invaluable.

* As Elder Fraud Explodes, Banks Beat Back Duty To Call Cops

* Prosecutions Across US Reveal Sales Of Customer Account Information Via Social Media, Dark Web

* Industry Has Fended Off Legislation That Could Boost Liability

US retirees sitting atop a record stockpile of wealth are facing an onslaught of elder fraud, with estimated annual losses exceeding $28 billion.

Maya Green’s (she is an outsourced employee of International call center operator Teleperformance) attorney, Joey Greenwald, said his client was low-level in the network and paid just a few hundred dollars for taking screenshots of accounts.

Greenwald said he was surprised his client was able to see so much information, noting she had a 10th-grade education and was working from home: “They hooked her up with a computer and a phone and she had all this access to customer accounts.” Greenwald said he’s not aware Green received any training on how to handle the data.

“To trust her with this kind of information was pretty appalling,” he said.

The new staffer was supposed to help Toronto-Dominion Bank spot money laundering from an outpost in New York.

She instead used her access to bank data to distribute customer details to a criminal network on Telegram, according to prosecutors in Manhattan. Local detectives who searched her phone allegedly found images of 255 checks belonging to customers, along with other personal information on almost 70 others.

It’s part of a little-noticed pattern popping up across US banking — from towers in Manhattan, to hubs in Florida and even suburban Louisiana.

As sophisticated scams targeting the life savings of Americans create headlines across the US, the industry’s lowest-paid employees keep getting caught selling sensitive customer information out the back door — emerging as a critical area of weakness in banks’ risk controls.

That’s an inconvenient trend as firms steadfastly argue to policymakers and the public that customers bear primary responsibility for ensuring they don’t get conned out of their savings. While many scams seemingly target people at random, some victims have said con artists who tricked them knew a lot about their finances at the outset.

“The more employees there are inside a company with access to sensitive customer information, the higher the risk that access is going to be abused,” said R.J. Cross, a privacy advocate at US Public Interest Research Group.

“Companies need to have technical measures in place to ensure employees and contractors can’t run off with people’s information or access data that isn’t necessary for their job duties.”

There have been warnings for years.

Almost a decade ago, New York’s then-attorney general, Eric Schneiderman, publicly urged major lenders including JPMorgan Chase & Co., Bank of America Corp. and Citigroup Inc. to strengthen internal defenses after an investigation found an identity-theft ring had enlisted tellers from the industry.

That built on a broader study by his office showing leaks by corporate insiders were already on the rise, with data “often obtained exclusively for fraudulent purposes.”

The recent spate of busts shows banks haven’t yet figured out how to stop employees from trying to monetize their access to highly valuable and sensitive customer information. Some connect with local conspirators on social media for schemes as mundane as faking checks.

Banks typically make those victims whole. But more sophisticated cons have proliferated in recent years, often leaving customers on the hook for their losses.

A few prosecutions, like the one against Wade Helms of Navy Federal Credit Union, illustrate how far data can flow.

Authorities in Escambia County, Florida, accused Helms of jotting personal information about customers in a notebook, creating a handle for himself on the dark web, and making it known he was seeking a buyer for information on clients at Navy Federal, the largest US credit union.

In one chatroom, Helms found someone who claimed to be a broker for stolen data. The two allegedly spoke by phone, then continued the conversation on a personal computer Helms kept next to his office desk.

The broker “wanted high-dollar account information because that would sell easier on the dark web,” according an affidavit for an arrest warrant for Helms. The broker created Telegram pages called “Navy Wave,” where screenshots of customer accounts were posted.

Some were provided by Helms, who had taken screenshots of customer banking statements and pictures of their identification, according to the warrant.

“Navy Wave” had multiple handles that began with @ScammingServices with more than 2,700 subscribers. By the time the credit union’s internal security discovered the breach, Helms allegedly had exposed as many as 50 accounts. At least five postings on the “Navy Wave” pages included Navy Federal accounts that Helms provided.

In a deal with prosecutors this year, Helms pleaded no contest to 11 charges, including illegal use of personal identification, and was sentenced to 10 years’ probation. He was also ordered to pay about $9,100 in restitution to Navy Federal.

A lawyer for Helms didn’t reply to messages seeking comment.

“Navy Federal takes all necessary precautions to protect our members’ personal and financial information,” a spokesperson for the credit union said in a statement. “We strengthen our processes on a constant basis to ensure member information is kept confidential and continuously monitor member accounts for unusual activity.”

The lender said it worked with law enforcement to help secure a conviction.

Incentivizing Firms

It’s challenging for companies to adjust to trends in crime, especially as firms are scaling up workforces with thousands of staff, including high-turnover jobs, said Jonathan Lopez, a former federal prosecutor who specializes in bank crime cases.

“The issue may not be one of a faulty program in many instances, but the sheer numbers of people involved,” said Lopez, a partner at Jacobson Lopez in Washington. “While zero fraud rates may be impossible, institutions should be incentivized to continue to strive to get their fraud rates and insider fraud rates as close to zero as possible.”

TD Bank’s recent $3.1 billion settlement with US authorities for failing to prevent money laundering revealed that executives’ focus on costs had contributed to weak internal systems. A result was a rash of crime that mostly went undetected until federal investigators tracking fentanyl sales on the East Coast took a close look at the bank.

The probe found several branch-level employees accepted bribes of cash and gift cards to open accounts and issue debit cards that were then used to move money to Colombia through ATMs.

The increased scrutiny also revealed that a New York-based branch manager stole more than $200,000 from an elderly client, using account information and a fraudulent email address to siphon funds even after the retiree died. The banker, later fired by TD, admitted to the crime and was sentenced to more than a year in prison. His lawyer said he stole the money to pay for his son’s college tuition.

Then in September, authorities in New York swooped in on Daria Sewell, a new employee in TD’s anti-money laundering operations, accusing her of storing images of customers’ checks on her phone. The breach exposed accounts to a network of New York-area fraudsters who were charged in a $500,000 check-fraud scheme, according to the Manhattan district attorney’s office.

Investigators said Sewell distributed information on Telegram with instructions on how to open bank accounts and move money from the TD accounts into them. Recipients allegedly then split profits with her.

Sewell has pleaded not guilty to unlawfully possessing personal information. A lawyer representing her didn’t reply to messages seeking comment.

“In both instances the employees were terminated and we cooperated fully with authorities in their investigations,” a TD spokesperson said in an email. “As we have consistently said, these individuals aren’t representative of our 30,000 colleagues in the US who serve our customers with integrity.”

Fraud Ring

Outsourcing can create more cracks in banks’ defenses.

In Louisiana, federal prosecutors traced a check-fraud ring to employees of international call center Teleperformance, where three employees in Shreveport were accused of selling the account information of elderly USAA customers.

The scheme went on for almost two years with the three — Arazhia Gully, Maya Green and Zarrajah Watkins — joining and offering information on customers with high account balances to a network of more than a dozen others, according to federal prosecutors. Some recipients used counterfeit checks to make withdrawals.

A portion of the proceeds was later deposited into the personal account of a Teleperformance employee and withdrawn at a nearby casino.

The trading of that data was similar to ordering from a menu at a restaurant, with outsiders choosing which accounts to exploit.

In an example provided by prosecutors, Gully sent a conspirator a text message containing the ages and account balances of eight USAA customers. The person responded with their pick: a 79-year-old with $442,000. Gully then sent a picture of a computer screen showing detailed account information. Another victim was a 95-year-old with $174,000.

“We fully cooperated with authorities to aid in the investigation and terminated the employees as soon as we were made aware of the incidents,” Teleperformance said in an emailed statement.

“We work closely with our clients to ensure we minimize our employees’ access to customer account information to include only the access needed to deliver the services and minimize the risk of fraud to the lowest possible level.”

A spokesperson for USAA declined to comment.

The three Teleperformance employees pleaded guilty to bank fraud conspiracy and are awaiting sentencing. Lawyers for Gully and Watkins declined to comment.

Related Articles:

A Retirement Wealth Gap Adds A New Indignity To Old Age (#GotBitcoin?)

Even A Booming Job Market Can’t Fill Retirement Shortfall For Older Workers (#GotBitcoin?)

Three Steps To Take If You’re Behind In Retirement Savings (#GotBitcoin?)

The New Retirement Plan: Save Almost Everything, Spend Virtually Nothing (#GotBitcoin?)

A Retirement Wealth Gap Adds A New Indignity To Old Age (#GotBitcoin?)

401(k) or ATM? Automated Retirement Savings Prove Easy to Pluck Prematurely (#GotBitcoin?)

How Aging Japan Defied Demographics And Revived Its Economy (#GotBitcoin?)

Your questions and comments are greatly appreciated.

Monty H. & Carolyn A.

Go back

Leave a Reply

You must be logged in to post a comment.