Ultimate Resource On Libor As It Transitions To Another Benchmark Index (#GotBitcoin)

Wall Street Banks Manipulated LIBOR In Rigging Us Treasury Auctions. Ultimate Resource On Libor As It Transitions To Another Benchmark Index (#GotBitcoin)

Annie Bell Adams 65-Year-Old Pensioner Leads LIBOR Class-Action Suit In New York Against 12 Major Banks.

As a result of the scandal, the Serious Fraud Office of Britain may pursue criminal prosecutions, and the United States Department of Justice’s criminal division is building cases against multiple financial institutions. It is the standard for $300 trillion of securities and loans. The Financial Times estimates as many as 100,000 plaintiffs will join in on the lawsuit.

Pension plans and municipalities have launched similar lawsuits attempting to recoup LIBOR-related costs, but it’s believed this lawsuit is the first time a person on the level of the individual homeowner has taken legal action in the unfolding story.

According to the Office of the Comptroller of the Currency, there were at least 900,000 outstanding home loans indexed to Libor originating from 2005 to 2009. The unpaid principal balance was $275 billion.

Dozens of consumer borrowers and credit-card users are seeking an injunction to end Libor, claiming the benchmark is the work of a “price-fixing cartel.” The plaintiffs are also seeking monetary damages.

Annie Bell Adams, on behalf of herself and all others similarly situated, Dennis Paul Fobes, on behalf of himself and all others similarly situated, Leigh E. Fobes, on behalf of herself and all others similarly situated, Margaret Lambert, on behalf of herself and all others similarly situated & Betty L. Gunter, on behalf of herself and all others similarly situated, Plaintiffs, represented by John Walter Sharbrough , John W. Sharbrough, III, PC & Stephen George Stim , Stimconsul Ltd. 110636484

Annie Bell Adams may have recently lost her house to foreclosure but she’s fighting back.

The 65-year-old pensioner is currently leading a class-action suit in New York against a dozen of the world’s largest banks for their alleged participation in the manipulation of the London Interbank Offered Rate (Libor) rate.

Adams’ lawsuit contends the Libor rate was raised artificially on the first day of the month, when her adjustable-rate mortgage rate was recalculated, thereby making her subprime loan payments substantially higher between 2000 and 2009.

Traders Manipulated Rates

Barclays has agreed to pay more than $500 miillion US in fines after internal emails revealed traders were claiming borrowing rates that were higher or lower than what they were actually having to pay in reality.

The Libor is the average interest rate at which international banks borrow from each other. It is calculated using major banks in London and is controlled by the British Bankers’ Association (BBA).

The Beginning of the Libor Scandal

The Libor scandal broke in June 2012 when British bank Barclays agreed to a $450 million settlement. This was in response to accusations by both British and American authorities that it manipulated the Libor rates. Questions are now being raised to why regulators did not put an immediate stop to the practice since evidence showed the Bank of England and the Federal Reserve of New York were both allegedly aware of the practice.

Since American financial institutions typically reference the Libor to set financial derivatives, mortgages and student loans, any manipulation of those rates can greatly impact a borrower’s payment. It is the standard for $300 trillion of securities and loans.

Adams, along with her four co-lead plaintiffs, has filed a class-action lawsuit against 12 banks, including: Citigroup Inc., HSBC Holdings Plc, Rabobank International Holdings BV, Credit Suisse Group AG, Deutsche Bank AG, Lloyds Banking Group Plc and Royal Bank of Canada.

The alleged artificial increase in Libor allowed banks to raise the interest rates on adjustable-rate loans. Since most adjustable-rate mortgages use the first of the month to reset rates, a manipulation of rates on that day would result in higher mortgage payments for countless people.

Altered Libor Rates And Their Effects

The lawsuit claims statistical analysis showed the Libor numbers consistently moved by 7.5 basis points on reset days between 2007 and 2009.

According to the lawsuit, the banks unjustly “enriched themselves” by manipulating the rate and thereby raising payments for homeowners with adjustable-rate loans and increase profits.

The complaint referenced traders’ emails published during the Barclays settlement. In one, the trader openly asked for a higher Libor rate because “We’re getting killed on our [three-month] resets.”

The plaintiffs, according to attorney John Sharbrough (Recently Dis-Barred Alabama-based lawyer), have each lost thousands of dollars because of this manipulation of rates. Libor manipulation claim lawsuits have been grouped together under one judge in the Southern District of New York. The banks have requested a hearing to dismiss the claims.

Insider dealing, the rigging or manipulation of benchmarks such as Libor, was deemed illegal as of last week. Backed by an influential European Parliament committee, traders who violate this new regulation could be sent to jail for a minimum five years. Less serious offenses would be eligible for a minimum two year sentence.

Traders outside of Europe suspected of similar crimes could face extradition, as long as regulators are willing to cooperate.

Updated: 1-20-2021

Wall Street Banks Manipulated LIBOR In Rigging Us Treasury Auctions (#GotBitcoin)

The antitrust probe was focused on whether Goldman Sachs traders colluded with others to fix prices in the $13 trillion Treasurys market.

Why Ditching Libor Is Vexing The Financial World

Declaring an end to Libor is one thing, making it happen another altogether. The deadline to drop the discredited London interbank offered rate is approaching at the end of 2021, leaving the financial world scrambling to adjust contracts on hundreds of trillions of dollars’ worth of products, from mortgages and credit cards to derivatives.

The risk of a chaotic transition has been likened to Y2K and the fear of computer systems misfiring at the end of the last millennium, only with the added challenge of a global pandemic thrown in. Whether the outcome will be as benign as Y2K turned out for the financial industry is about to unfold.

1. What’s The Worry?

As much as half of the outstanding Libor-priced contracts expire after the deadline. That means the clock is ticking to switch those agreements — often termed “legacy contracts” — to non-Libor rates. The process has been delayed somewhat by the pandemic, while the sheer breadth and scale of Libor’s use means that multiple industries and regulators are having to adjust.

In practice, some are doing so with more urgency than others.

2. What Is Libor And Why Is It Disappearing?

For about 50 years, Libor has helped determine the cost of borrowing around the world. It is a daily average of what banks say they would have to pay to borrow from one another and forms the basis for floating-rate or variable loans and bonds, as well as derivatives.

The London-based British Bankers’ Association formalized the gauge in 1986 when it needed a way to price interest-rate swaps and syndicated loans. But as markets evolved, the trading that helped inform banks’ estimates dried up. And ever since evidence emerged in 2008 that European and U.S. lenders had manipulated rates to benefit their own portfolios, the benchmark has been seen as tainted. By the end of 2016, a dozen banks had paid penalties approaching $10 billion.

3. Who Cares?

Lots of people do. They include pension and fund managers, insurance companies, lenders big and small and Wall Street banks that package loans into securities. Equipment leases, commercial paper, sovereign bonds, student and auto loans, bank deposits and mortgages are among the $370 trillion of financial products that the International Swaps and Derivatives Association says are tied to Libor and related interbank rates. The biggest use is for derivatives like interest-rate swaps, which companies, banks and investors use to hedge risk or to speculate.

4. What’s Taking Libor’s Place?

Central banks have been working to develop replacement benchmarks based on what are called risk-free rates. The goal is to find rates that are a truer reflection of the cost of capital, and are based on actual transactions.

The upshot is an array of acronyms with varying degrees of catchiness, including the U.S.’s Secured Overnight Financing Rate (SOFR), the U.K.’s Sterling Overnight Index Average (Sonia) and the Euro Short-Term Rate (ESTR).

5. How Do The Replacements Stack Up?

In one important aspect they fall short. Libor offers forward-looking rates — that is, rates that incorporate market expectations for the cost of borrowing over a particular time scale, from overnight to a year. By contrast, the new benchmarks mostly reflect overnight lending rates. SOFR, for instance, is based on the U.S. repo market, where cash is briefly exchanged for high-quality securities such as U.S. Treasuries.

In A Post-Libor World, Here Are The Benchmarks That Will Matter

6. Why The Trepidation Over Loans?

Rewriting legacy contracts so they track an overnight benchmark instead of, say, a three-month rate, would be hugely complicated and probably requires renegotiation. Lawyers say many such contracts may end up in court since getting unanimous agreement on a replacement or “fallback” rate would be difficult.

“The big elephant in the room is legacy transactions which have no fallback provisions,” said Y. Daphne Coelho-Adam, counsel at Seward & Kissel LLP in New York. “There is a risk of litigation.” Moody’s Investors Service has warned of increased credit risks due to slow progress on switching from Libor.

7. What About The Derivatives Market?

There’s less concern there. A protocol taking effect in late January will enable firms to incorporate so-called fallback language into contracts, so they can transition smoothly into replacement benchmarks. That will help firms avoid complicated renegotiations and a cliff-edge Libor scenario.

An estimated $200 trillion of financial contracts reference dollar Libor alone, with 95% of this exposure in derivatives, according to the Federal Reserve Bank of New York. Widespread adoption of the protocol is necessary to mitigate broader risks, according to the Financial Stability Board, an international body that monitors the global financial system.

A milestone was reached in October when interest-rate swaps on more than $80 trillion in notional debt switched to the new U.S. benchmark SOFR as the discounting rate.

8. What Are Governments Doing?

The U.K. is handing regulators extra powers to help with legacy contracts that can’t be easily renegotiated. In the U.S., planned New York state legislation would incorporate recommended fallback language for particular products in an effort to enable automatic transition to other rates.

However, lawmakers have been so preoccupied with Covid-19 that the draft law has been held up, fueling anxiety on Wall Street.

9. How Else Has Covid-19 Changed The Landscape?

It disrupted the campaign to ditch Libor and even intensified its use. Both the U.S. and U.K. governments allowed Libor to be referenced as part of emergency loan programs to help keep businesses afloat. The Bank of England delayed plans to encourage banks to ditch the rate and the U.K. pushed back a deadline for lenders to cease issuing Libor-linked contracts.

10. How Will This Affect Regular Consumers?

There’ll be scrutiny over whether they will be forced to pay higher rates. Banks and asset managers face a greatly increased risk of fines, litigation and reputational damage if they poorly manage the transition for existing contracts and products, with regulators likely to watching closely whether they are treating customers fairly.

11. Will Libor Be History From 2022?

Regulators insist the transition won’t be delayed, but be prepared for a possible “synthetic” Libor. The U.K. regulator has hinted at the continued publication of the benchmark using a “more robust” methodology not based on bank submissions. This would only be applicable for legacy contracts that can’t switch to another rate. Details remain sketchy.

————————————–

The probe, which exposed weaknesses in the way the US Treasury prices the interest on the country’s debt obligations, has been an embarrassing one for Washington since it was first exposed in June 2015.

Investigators are hitting dry wells in their evidence hunt through thousands of pages of Bloomberg chats, plus dozens of interviews, to bring a clear case, one law enforcement official familiar with the probe told The Post.

“There just wasn’t enough there,” the person said.

The probe, which exposed potential weaknesses in the way the US Treasury prices the interest on the country’s debt obligations, has been an embarrassing one for Washington since it wasfirst exposed by The Post in June 2015.

Jacob Lew, then head of the Treasury under President Barack Obama, wanted a quick resolution to the probe soon after it was revealed, The Post reported in 2017

Since then, Lew was replaced by Goldman alumnus Steve Mnuchin, who is now Treasury secretary under President Trump. Another ex-Goldman partner who joined the White House, Gary Cohn, had overseen the division that submitted the bids to Treasury at the time.

No one has accused Lew, Mnuchin or Cohn of any wrongdoing in the matter.

While charges are unlikely to be filed, it’s not clear that banks won’t suffer some negative consequences.

A class-action lawsuit filed in 2015 showed that, after The Post first broke the story, banks changed their behavior in how they bid for Treasury bonds.

The suit, which was brought on behalf of pension funds and investors, also relied on a confidential informant who helped describe how the banks allegedly rigged the Treasury markets.

As recently as 2017, Department of Justice investigators were focused on a period from 2007 to 2011 when Goldman was particularly successful in bidding for Treasury bonds, sources told The Post in 2017.

Since then, however, a string of departures at the department also slowed the investigation, a third source told The Post.

The talks between Goldman and the feds have been “inactive,” another person familiar with the talks told The Post.

The investigation was one of many that looked into banks for potential conspiracies to rig markets in the wake of blockbuster interest-rate and currency-rigging probes that led to billions of dollars in fines and the resignation of top execs, including Barclays chief executive Robert Diamond.

Other banks, including Deutsche Bank, Royal Bank of Scotland, BNP Paribas, Morgan Stanley, and UBS, had trading and chat records subpoenaed by the Department of Justice.

In addition, the Securities and Exchange Commission and the New York Department of Financial Services were investigating the alleged rigging.

Spokespeople for the Department of Justice and the SEC didn’t return requests for comment, and a DFS spokesman declined to comment.

Wall St. Traders Secretly Used Chat Rooms To Rig Treasury Bond Prices:

Wall Street banks secretly shared client information in online chat rooms in order to rig auctions for the $14 trillion US Treasurys market, according to an explosive lawsuit filed in Manhattan federal court on Wednesday.

The move wrongly fattened the banks’ profits and picked profits from clients, the suit claims.

The new accusations, leveled by several pension funds and wealthy individual investors, are contained in an expanded class-action suit originally filed in July 2015 — and include an unusual twist: Some of the evidence came from confidential informants and one of the banks sued in the earlier action.

That bank is now cooperating with the plaintiffs in the massive civil action, and is providing an in-depth look into how Wall Street allegedly conspired to rig Treasury bond trades.

The revised lawsuit expands on details on how the banks conspired to set Treasury bond prices — like moves to manipulate the price of the bonds higher on days when there was a lot of demand, and vice versa, court papers claim.

The funds, representing retirees and public workers, also claim the banks conspired to rig the secondary Treasury markets beginning in the 1990s through tightly controlled electronic platforms that inhibited more competitive trading — a new allegation that wasn’t in the original suit but mirrors similar complaints filed against banks in other markets, like stock loans.

The amended suit tightens its focus on a select number of banks, naming Goldman Sachs, Morgan Stanley, the Royal Bank of Scotland, BNP Paribas, and UBS, among others, as the firms behind the rigging, which they allege occurred from Jan. 1, 2007, to mid-2015.

Last year, the judge presiding over the class-action suit had questioned whether the claims were strong enough to proceed.

The funds continue to allege the banks mined their own customers’ bids for Treasury bonds to get a bigger share of the auction, and sell the bonds for more profit.

Probes on the auction practices are being conducted by the Justice Department, the Securities and Exchange Commission and other federal, state and overseas regulators, sources said. No regulator has accused any bank of wrongdoing.

The banks named in the suit are primary dealers, which means they buy the debt directly from the Treasury and resell it to their clients at a pre-determined price.

Typically, the Treasury holds an auction, then banks submit their bids for US debt based on how much they think those bonds are worth. The Treasury then doles out the bonds proportionately to the bidders at the same price. The bank that asked for the best price gets the most bonds.

Traders at the Wall Street banks shared the prices that their clients had sought to buy the bonds, giving each of the banks in the alleged cartel a clearer picture of what they thought the market was, and a better chance at getting a bigger share of the bonds to sell, according to the complaint.

Details about bid prices are supposed to be a closely held secret.

Washington’s probe into the alleged rigging of the $13 trillion US Treasurys market by Wall Street banks has narrowed its focus to a handful of firms — including Goldman Sachs.

In addition, European authorities have opened their own investigation into possible Treasurys bid-rigging, sources said.

Investigators in the fraud division of the Justice Department have obtained chats and emails from Goldman that appear to implicate the company in manipulating the price of Treasury bonds, according to two sources familiar with the investigation.

Those chats and emails are being analyzed to determine if traders at other banks could be involved with any possible bid-rigging of US government debt, those two people said.

The identities of any traders in investigators’ cross hairs couldn’t be learned.

Goldman is said to be cooperating with the probe, one person said.

In June, The Post reported exclusively that Justice was in the early stages of investigating banks for rigging the price of Treasurys, the largest and most easily tradeable asset in the world.

Goldman is one of about 22 financial institutions that have been probed for any evidence that they may have manipulated Treasury auctions — a secretive process where banks and other financial services companies bid on the price of government debt, sources said.

Justice is also looking into whether there was price-rigging in the secondary market for Treasurys, where debt is sold at a premium, sources added. It’s unclear if investigators have yet found any improprieties or criminality.

Goldman, run by Chief Executive Lloyd Blankfein, is a major player in US government bond trading, and regularly submits bids for auctions.

In November, Goldman disclosed in a regulatory document that it was being probed for possible manipulation of government bond prices. Michael DuVally, a Goldman spokesman, declined to comment further.

Meanwhile, the European Commission, the law enforcement arm of the European Union, has opened its own investigation, joining Justice, the Securities and Exchange Commission, the Commodity Futures Trading Commission, and the New York Department of Financial Services, according to two sources.

The rigging investigation is the biggest scandal to hit the quiet but crucial Treasurys market since 1990 when Paul Mozer, a former Salomon Brothers partner, illegally cornered the government debt market. Mozer’s actions are known to readers of Michael Lewis’ “Liar’s Poker.”

Traders are thought to have rigged the market in two possible ways: by agreeing beforehand to keep bond prices higher than normal in order to boost profits in other positions that depend on higher rates, similar to how banks rigged the London-based Libor rate.

Banks also could have colluded to keep prices lower than normal to sell them at a higher price — and score a bigger spread — to their clients, who agreed to pay a fixed amount beforehand.

69% Of Reissued Treasury Auctions Were Suspicious, Suit Says

Same Type Of Analysis Caught Cheating In Currencies And Libor

The same analytical technique that uncovered cheating in currency markets and the Libor rates benchmark — resulting in about $20 billion of fines — suggests the dealers who control the U.S. Treasury market rigged bond auctions for years, according to a lawsuit.

The analysis was part of a 115-page lawsuit filed in Manhattan federal court on Aug. 26 by Quinn Emmanuel Urquhart & Sullivan LLP and other law firms. The plaintiffs built their case against the 22 primary dealers who serve as the backbone of Treasury trading — including Goldman Sachs Group Inc., JPMorgan Chase & Co. and Morgan Stanley — using data from Rosa Abrantes-Metz, an adjunct associate professor at New York University who has provided expert testimony in rigging cases.

Her conclusion: More than two-thirds of a certain type of Treasury auction appear to have been rigged. She found issues with other auctions, too.

“The only plausible explanation is that Defendants coordinated artificially to influence the results of the auctions in the primary market,” according to the complaint filed by the Cleveland Bakers and Teamsters Pension Fund and other investors.

The lawsuit, which seeks unspecified damages, comes as the U.S. Justice Department probes whether information in the Treasury auction market is being shared improperly by financial institutions, three people with knowledge of the investigation said in June. Treasury traders at some banks learn of customer demand hours before auctions, and were communicating with their counterparts at other firms via chat rooms as recently as last year, Bloomberg News reported earlier this year.

Abrantes-Metz’s analysis is similar to one used in lawsuits claiming bank and broker manipulation of the London interbank offer rate, or Libor. Those cases resulted in about $9 billion in settlements from the financial firms. Banks and brokers have paid about $9.9 billion in fines to global regulators related to manipulation of currency markets as of May.

Representatives of Goldman Sachs, JPMorgan and Morgan Stanley declined to comment on the Treasury lawsuit’s allegations.

The U.S. Treasury initially sells securities to the primary dealers who in turn sell them to clients, creating a secondary market for trading. Sometimes, after auctioning off debt, the government later issues an identical batch of securities — known as reissued Treasuries.

When the second set of Treasuries is issued, their prices and yields can be compared with the identical securities already trading in the secondary market. If there are pricing differences, that could be evidence of a problem. According to the plaintiffs, 69 percent of the auctions of reissued Treasuries from 2009 to 2015 appear to have been rigged, artificially boosting yields by 0.91 basis points.

The plaintiffs said there’s evidence of cheating from at least 2007 through earlier this year, when press reports revealed the Justice Department investigation into the auction process.

“These analyses reveal a consistent pattern: Treasury auction yields were artificially high (and prices correspondingly low),” according to the complaint. “Defendants then turned around and sold the Treasuries at higher prices (and correspondingly lower yields) in the secondary markets, reaping substantial profits.”

The data analysis showed similar discrepancies when prices at Treasury auctions were compared to those in the secondary market as well as the when-issued market. Treasury futures experienced similar downward pressure on prices leading up to auctions, the lawsuit claims.

Among the lawyers representing the investors is Daniel Brockett, a Quinn Emmanuel attorney who recently won a $1.87 billion settlement against Wall Street’s largest banks in a case alleging they conspired to limit competition in the market for credit-default swaps.

Brockett said in an interview that the new lawsuit alleges the artificially low auction prices grew in direct proportion to how many primary dealers were involved in an auction.

“No matter which way you measure it, they end up benefiting in ways that wouldn’t otherwise be possible in a liquid market of this size,” he said. The $12.8 trillion Treasury market helps sets interest rates on everything from home mortgages to credit cards and is often described as the largest, most-liquid market in the world.

Another group of investors, including Boston’s public employee retirement system, has filed a similar suit against Wall Street primary dealers. Experts interviewed by Labaton Sucharow LLP, the law firm that filed that suit, analyzed auctions and the market for when-issued securities, which are essentially agreements to buy or sell Treasury bonds, notes or bills once they’re issued.

They claim that banks colluded to push prices artificially low at auctions, and to drive prices for when-issued securities to artificially high levels, until December 2012, when news broke of investigations into how Libor was set.

“These scenarios all turn on a very simple conflict of interest,” attorney Michael Stocker said in a telephone interview. “You had banks who were auction participants who also had the power to move the prices that those markets depended on.”

Wall Street Banks Accused,Wall Street Banks Accused,Wall Street Banks Accused,Wall Street Banks Accused,Wall Street Banks Accused,Wall Street Banks Accused

A Justice Department spokesman didn’t return an email seeking comment, while EC spokesman Ricardo Cardoso declined to comment.

Each bank declined to comment on the lawsuit after it was first filed.

Updated: 1-3-2020

Regulators Ask Banks About Preparations for Libor’s Demise

Banks must show how they are managing risks stemming from the planned end of the benchmark rate next year.

Financial regulators are asking banks to show they have plans in place to manage the risks stemming from the planned demise of a key benchmark interest rate.

Regulators, which for months have urged banks and other financial services firms to prepare for the likely end of the London interbank offered rate in 2021, have recently begun asking for evidence of their preparations.

The New York State Department of Financial Services is requiring banks and insurers to submit plans for managing the risks associated with the end of Libor, the agency said in a letter last week. The Office of the Comptroller of the Currency, which oversees national banks, said in December that it plans to increase oversight of the issue and that examiners will evaluate whether banks have made an inventory of all contracts that could be affected.

The Federal Reserve’s supervisors have also begun asking banks about their plans, Vice Chairman for Supervision Randal Quarles said in June. The Federal Deposit Insurance Corp. declined to comment.

“They are all making similar noises: ‘We need you to pay attention. It is important. It isn’t going to go away,’ ” said Paul Forrester, a partner at law firm Mayer Brown LLP who focuses on corporate finance and securities.

Global banks face a particularly thorny challenge in moving away from Libor because they need to take into consideration the range of alternative rates that could be used in currencies across the world, Mr. Forrester said.

Major banks have made progress in preparing for the transition, according to Dan Stipano, former deputy chief counsel at the OCC. However, the coming transition to an alternative rate is rife with legal and operational risks for the industry, lawyers said.

“They need to give themselves a lot of lead time,” said Mr. Stipano, who is now a partner at Buckley LLP.

Updated: 8-20-2020

Libor Troubles Deepen As Deadline For Benchmark’s Demise Approaches

Regulators and investors say transition remains on track despite setbacks including the Covid-19 pandemic.

No one said replacing the London interbank offered rate would be easy, but many regulators and investors contend the cumbersome process remains on track despite setbacks including the coronavirus pandemic.

Deeply rooted in markets after decades and linked to trillions of dollars of financial products, Libor is slated for replacement by the end of 2021. Policy makers and regulators moved to scrap the benchmark after concluding it was balky and prone to manipulation, as exposed by a 2012 scandal that led to convictions for some traders and penalties for numerous banks.

If the transition doesn’t go as planned, it could leave everyone worse off. Consumers could end up on the hook for increased payments on credit-card loans and other borrowings, while small businesses could face higher fixed rates for loans. About $190 trillion of interest-rate derivatives and $3.4 trillion of business loans are tied to the rate.

Bankers and others in the market for short-term lending say a number of developments this year give them confidence that they can manage Libor’s demise and the transition to alternative lending benchmarks.

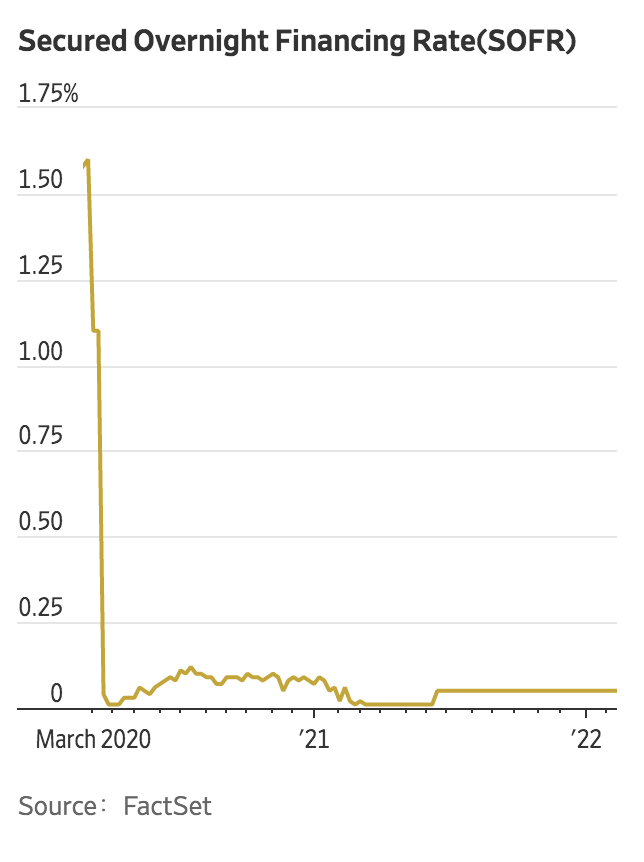

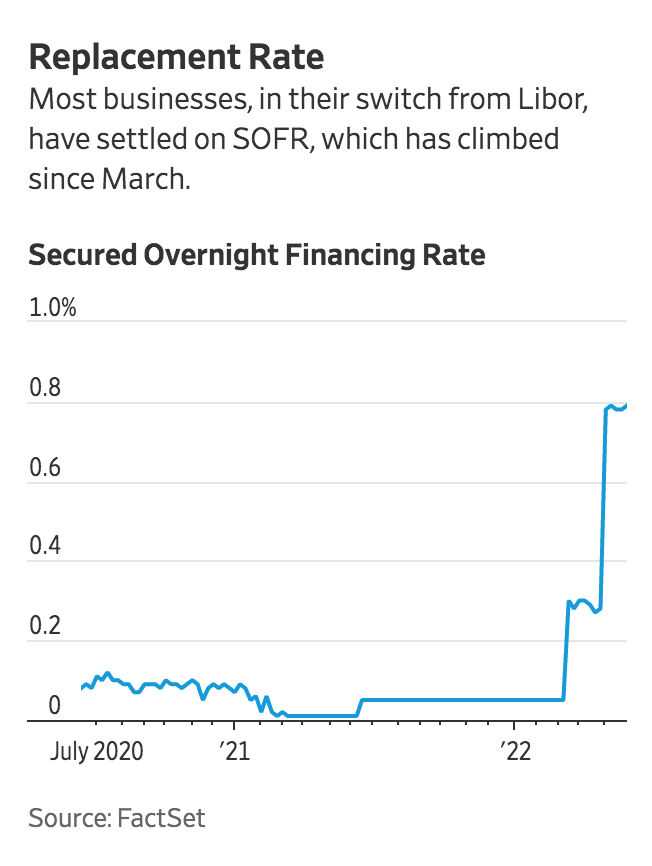

A Federal Reserve committee of regulators, banks and asset managers chose the Secured Overnight Financing Rate, or SOFR, as the official replacement.

The Alternative Reference Rates Committee, consisting of major banks, insurers and asset managers alongside the New York Fed, have been rallying derivatives investors and users of Libor to be ready for the end. Fannie Mae and Freddie Mac have said they would stop accepting adjustable-rate mortgages tied to Libor by the end of 2020. Banks are spending millions of dollars and mobilizing everyone from lawyers to trading-floor staff.

But efforts were put on ice for more than a month as financial institutions grappled with tumbling stocks, margin calls and clients racing for cash as the coronavirus sent markets into a tailspin prompting unprecedented action by the Fed.

The temporary breakdown of U.S. Treasury markets in March led some to question the stability of SOFR, which is based on the cost of transactions in the market for overnight repurchase agreements, or repos. That is where financial companies borrow cash overnight using U.S. government debt as collateral.

SOFR dropped to 0.26% on March 16 before doubling the next day, only to fall again. Moves that week reminded investors of volatility last September, when SOFR surged above 5% because of idiosyncratic strains in the repo market.

“There is a growing consensus that SOFR as a replacement for Libor doesn’t really work,” said Scott Shay, co-founder of New York-based Signature Bank.

Smaller and midsize banks are favoring another benchmark: Ameribor. Established by Richard Sandor, a key player in the creation of futures markets in the 1970s, Ameribor is based on rates set on the American Financial Exchange, which he founded.

Smaller banks say Ameribor reflects the cost of funds in trading in financial markets for banks that aren’t among the Fed’s exclusive counterparties—also known as primary dealers.

Some wonder whether the deadline for the transition away from Libor will be pushed back. Investment-bank analysts and salespeople estimate that only a quarter of clients are ready for the benchmark to disappear.

“I think Libor will go away, but will everybody be ready for it in 18 months?” said Paul Noring, managing director at BRG, a consulting firm in Washington, D.C.

Tom Wipf, a vice chairman at Morgan Stanley who is chairman of the Alternative Reference Rates Committee, said that the move to SOFR was on track and that the committee was able to double the number of virtual meetings—with travel schedules restrained by lockdowns related to the pandemic—to get the job done.

He said policy makers weren’t pleased with Libor’s volatility during the March stress period, underscoring the need to make the transition in a timely manner.

“All the concerns that got us here in the first place were revealed again during that period of market stress,” said Mr. Wipf.

The U.K. regulator in charge of overseeing Libor made it clear a deadline extension was out of the question. Edwin Schooling Latter, a senior regulator at the Financial Conduct Authority, said in July that Libor’s death notice wouldn’t be pushed back by the impact of the coronavirus.

“The four to six months ahead of us are arguably the most critical period in the transition away from Libor,” Mr. Latter said in a speech.

Josh Younger, head of interest-rate derivative research at JPMorgan Chase & Co., said investors and asset managers saw significant risks of a delay until U.K. officials came up with a solution in June to overcome one of the biggest hurdles blocking a smooth transition away from Libor: so-called tough legacy contracts.

These include floating-rate notes that require bondholders to agree on a new reference rate, which is a nearly impossible task, according to lawyers at companies advising banks and clients.

To avoid litigation, the U.K. government said in June it would amend the rulebook, handing the FCA, the benchmark’s overseer, the power to craft what some call a “zombie-type” Libor that could exist for certain legacy contracts.

“Dealing with tough legacy contracts potentially accelerates the time frame over which this transition can happen,” Mr. Younger said.

Updated: 10-16-2020

Banks Brace For ‘Big Bang’ Switch On $80 Out $200 Trillion Worth of Swaps

The big bang is one of the most important steps in the Libor transition to SOFR.

It’s being called the “big bang,” and it has derivatives traders on high alert.

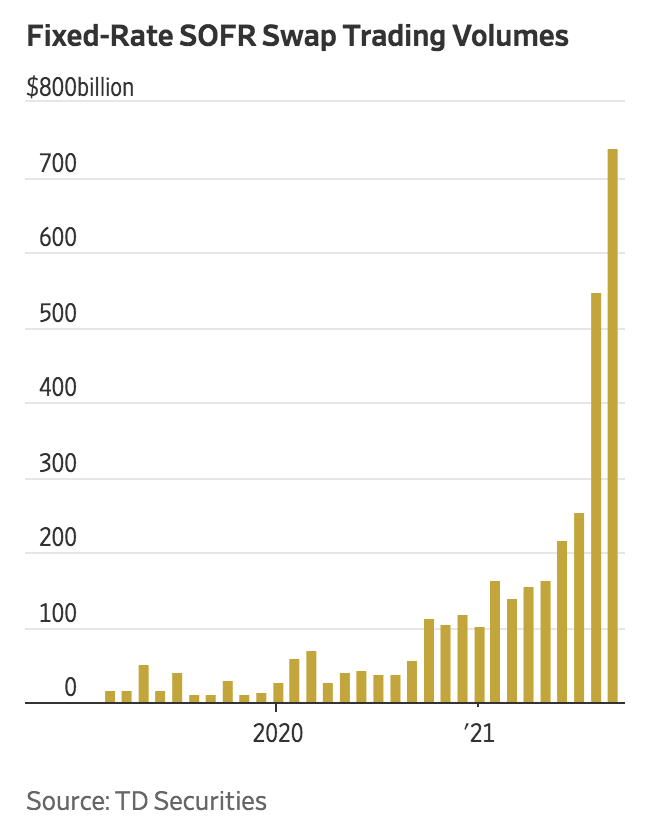

In a critical development in the global shift away from old benchmarks that was triggered by Libor’s shortcomings, interest-rate swaps on more than $80 trillion in notional debt will transition this weekend to a new rate for determining their value.

While the switch to the secured overnight financing rate, or SOFR, is expected to boost longer-term liquidity in the new benchmark, it also is fueling concerns about unruly price action because it is expected to trigger the sale of swaps on tens of billions of dollars of debt.

“The big bang is one of the most important steps in the Libor transition,” said Marcus Burnett, director of SOFR Academy, an education technology firm whose clients include banks and asset managers. “We expect rates desks from the largest banks in New York to be participating.”

The reset, which will see SOFR replace the effective federal funds rate in calculations that value swaps, is part of a push to make SOFR a standard U.S. reference rate in debt and derivatives markets. SOFR is intended to replace dollar Libor, which still underpins hundreds of trillions of dollars of assets such as mortgages in the U.S. and syndicated loans in Asia.

The big bang follows a smaller-scale pivot in Europe this July, a less-complicated switch that occurred without much impact on the market.

Interest rate swaps allow two parties to trade one stream of payments for another, over a set period of time. The most common variety, known as a vanilla swap, involves exchanging payments from a fixed rate for payments from an adjustable rate that is based on Libor or some other reference rate. Another kind, known as a basis swap, involves two adjustable rates.

While SOFR has struggled to gain traction since its introduction in 2018, analysts say the upcoming big bang has already triggered a shift toward more trading in SOFR-linked swaps.

This could help pave the way for a curve that reflects expectations for where the rate will be in the future, addressing one of the new benchmark’s key weaknesses.

The big bang “will have a very, very good impact on liquidity,” said Jason Granet, chief Libor transition officer at Goldman Sachs Group Inc.

Compensation

Still, in the immediate future there will be turbulence in pricing. Clearing houses are planning to effectively neutralize the changes in swap values caused by the big bang, and traders will see their positions automatically adjusted. LCH Ltd. and CME Group Inc. are preparing to distribute compensation from clients whose position values go up to those who see them decline.

LCH will facilitate payment of hundreds of millions of dollars in cash to cover lost value, and at least tens of billions of dollars in basis swaps to compensate for risk, said David Horner, head of risk at SwapClear, which is part of LCH.

However, some firms do not use basis swaps to hedge their discount-rate risk or are otherwise incapable of keeping them on their books, so they are expected to sell them. This Friday LCH will hold auctions in which 18 banks can close out $25 billion in unwanted basis swaps.

Buyers, ideally, would snap them up either as hedges against risk or for their own value. But the approach is largely untested since basis swaps were not distributed in the European version of the big bang.

“For about six months our members and clients have been able to look on their screens and see a forecast for the compensating cash payments and compensating swaps they will receive, so they are familiar with what’s about to happen,” said Horner. “It’s important for the market that it runs smoothly.”

CME will hold a similar auction on Monday. Clients have agreed to a maximum loss, said Sunil Cutinho, president of CME Clearing, and “if their positions cannot be auctioned off then they are fully protected and they can use their own private means to dispose of their positions.”

However, there are concerns about price swings in the market amid a surge in supply as some banks ditch basis swaps they received as compensation.

The big question is how well the auctions go. Clearing houses are not guaranteeing the minimum prices for the basis swaps, which could fall below the maximum that firms are prepared to tolerate, said Joshua Younger, a strategist at JPMorgan Chase & Co.

“Many would then likely unwind them in the open market and the price action could get very disorderly,” he said.

Firms need to understand they are facing more risk from this change first before they eventually get less risk, said Pieter Van Vredenburch, a principal at Market Alpha Advisors and previously a member of the Alternative Reference Rates Committee, which is guiding the U.S. Libor transition, when he worked for HSBC Holdings Plc in 2016.

“The big banks are very prepared for the big bang,” said Van Vredenburch. “But do I think the smaller banks are ready for this? Not even close.” When it comes to the overall switch to SOFR, he said, “there are so many nuances to the transition and the devil is in the details. There is nothing simple in all this.

Share Your Thoughts

Updated: 11-18-2020

Libor’s Survival Beyond 2021 Death Date Becomes Hot New Wager

Don’t count Libor out just yet.

From traders scurrying to exit bets on a replacement for the benchmark, to analysts at Wells Fargo giving good odds it’ll keep going, there’s newfound uncertainty in markets over whether the beleaguered index will disappear at the end of next year like it was supposed to.

Eurodollar futures — among the world’s largest interest-rate derivative markets — sprang to life Wednesday after Libor’s administrator and U.K. financial regulators opened the door for the dollar version of the index to survive its previous Dec. 31, 2021, expiration date. The futures contracts reference three-month dollar Libor, set daily by ICE Benchmark Administration but which had been slated for extinction by global regulators.

The market priced in a longer timeline for the interest rate, and the move may have further to run. For dollar Libor, “the chance has increased significantly that it will survive past 2021,” Wells Fargo strategists Zachary Griffiths and Mike Schumacher said in a note. “We doubt that market prices fully reflect this likelihood,” and expect forward one- and three-month rates “to continue rising for early 2022 vs late 2021 dates.”

A series of bets set up to exploit the replacement of Libor got wiped out Wednesday. Traders rushed to buy March 2022 Libor contracts, driving down their spread over December 2021 equivalents, which had been steadily widening on expectations that rates would be higher after the benchmark switchover. The March contract was the most actively traded of the day on volumes almost four times higher than Tuesday, and a drop in its open interest suggested positions were being unwound.

A combined daily volume of 1.2 million futures across December 2021 as well as March and June 2022 contracts was only topped one other day this year on March 2. The surge in volume represented both outright buying and selling of the contracts and spread among the three tenors.

ICE Benchmark Administration Limited said it intends to cease publication of most major Libor benchmarks at the end of 2021, with the exception of the dollar variety where discussions are still continuing with key stakeholders. That was enough to raise the possibility among market participants that the replacement of dollar Libor may be on a different timeline.

The move toward Libor alternatives, such as the Secured Overnight Financing Rate, is a response to concerns about the benchmark, including revelations about manipulation in the wake of the financial crisis. For more than three years, global policy makers have been developing new benchmarks.

The Federal Reserve Bank of New York, meanwhile, on Thursday tweeted a reiteration of its support for a “smooth transition for consumers, businesses and market participants” away from Libor in dollar-related markets, noting that the clock is ticking for the beleaguered benchmark.

Traders had been using spread trades to bet on expected rates moves around the transition period — buying or selling one contract against another to capture relative changes between the two, rather than directional moves.

While it’s possible that market watchers have read too much into Wednesday’s statement, the ambiguity over a timeline suggests Libor fixings for early 2022 may take place under the current methodology, instead of the incoming method of SOFR plus a spread.

This is also reflected in the narrowing of the difference in premiums between the December 2021 and March 2022 contracts against the overnight rate or FRA/OIS.

March 2022 FRA/OIS, which is determined by expectations of where ISDA’s fallback rate will be, narrowed as much as 1.7 basis points Wednesday. That came as traders bet the continuation of the Libor benchmark will push the premium toward December 2021 FRA/OIS, which is based on Libor expectations and is around six basis points lower.

Updated: 11-30-2020

Libor’s Likely Reprieve Is a Welcome Acknowledgment of Reality

Libor is flawed. But better to let it wither on the vine than try to force its early abolition.

The overseers of three-month dollar Libor are considering a stay of execution for the benchmark interest rate for trillions of dollars’ worth of securities that was scheduled to expire at the end of next year. It’s a welcome acknowledgment of the reality that the financial industry has failed to embrace any potential replacements for the suite of interest rates once dubbed the world’s most important numbers.

The London interbank offered rates dictate the pricing of everything from mortgages to corporate loans to derivatives contracts, across a range of maturities and currencies. But they’re flawed: The wholesale interbank lending market on which they were based dried up in the wake of the global financial crisis, while many of the banks responsible for setting their values have paid billions of dollars in fines for rigging the benchmarks in their own favor.

So market regulators have proposed alternatives, including the Secured Overnight Financing Rate in dollars and the Sterling Overnight Interbank Average Rate in U.K. markets. But adoption has been slow, particularly in the U.S. market. For example, in the week ended Nov. 20 almost $2.5 trillion of dollar interest-rate swaps tied to Libor were traded, compared with just $70.5 billion contracts that referenced SOFR, according to figures compiled by the International Swaps and Derivatives Association. So far this year, $96 trillion of Libor swaps outstrip the $1.8 trillion of SOFR trades.

What’s more worrying is the patchy preparations for Libor to be turned off. A Duff & Phelps survey published in September of more than 100 companies, including hedge funds, private equity firms and banks, showed that while two-thirds hadn’t completed planning for the change, one in five hadn’t even started the process of making the transition away from Libor. The pandemic may be more of an excuse than a reason for the lack of activity, but that doesn’t make the issue any less real.

The proposal by the ICE Benchmark Administration Ltd. would see three-month dollar Libor continuing until the middle of June 2023, along with its six- and 12-month flavors. That 18-month extension would mean the vast majority of existing contracts tied to Libor would have expired by the time the benchmark ceased to exist. There’d be no need to rewrite an untold number of agreements signed when Libor looked set to last.

That’s a sensible way to deal with the issue, given that market participants continue to question the usefulness of the replacements. For one thing, the new benchmarks are based on overnight borrowing costs, making it tricky (though not impossible) to calculate the matrix of longer-term tenors that the market relies on. Perhaps more importantly, the credit risk currently reflected in Libor is absent from the new values, leading to a complicated system of adjustments needed to compensate for discrepancies between the different benchmarks.

I argued in May that Libor should be reprieved. The overseers of Libor in other jurisdictions, notably the U.K., should reconsider their end-2021 deadline in light of the U.S. decision to think again (although ISDA’s figures suggest that the City of London has been more responsive to the Financial Conduct Authority’s urgings, with SONIA swaps this year worth more than $15.6 trillion outpacing the $12 trillion of sterling Libor interest-rate derivatives).

Market regulators may feel slightly embarrassed at having to backtrack. But allowing a longer period for the universe of legacy contracts to shrink while continuing to urge financial firms to stop writing new business tied to Libor is a smart strategy. It sure beats the potential disruption of forcing the market to switch before it’s ready.

Updated: 1-20-2021

Libor Overhaul Gets Boost In Cuomo Bid To Avert Transition Chaos

New York Governor Andrew Cuomo has proposed legislation that would help prevent hundreds of billions of dollars of financial contracts from descending into chaos when the London interbank offered rate expires.

Provisions to help troublesome Libor-linked contracts switch to replacement rates are contained in Cuomo’s state budget plan, which was published on Tuesday. Bankers, investors and regulators see such proposals as crucial to ensuring that a large swath of the global financial system isn’t disrupted.

Various tenors of dollar Libor may be given a reprieve until mid-2023, in part to allow legacy contracts that lack a clear replacement rate to die off naturally. While that would help reduce the threat to financial stability, the most challenging floating-rate debt and securitizations — as well as Libor-based mortgages and student loans — will run on past the new deadline, making legislation critical. As home to the world’s biggest financial center, much of the debt falls under New York law.

“This legislative proposal is essential in order to provide legal certainty and minimize the adverse economic impacts for legacy Libor contracts,” said Tom Wipf, vice chairman of institutional securities at Morgan Stanley and chairman of the Alternative Reference Rates Committee, the Federal Reserve-backed body guiding the transition. The governor’s decision to include it in his budget plan “marks notable progress,” he said.

The U.K. hasn’t faced the same complications around sterling Libor, partly because of its different exit strategy. Proposals to keep publishing a “synthetic” Libor number that doesn’t require trading data from panel banks would help legacy contracts that can’t transition to avoid a cliff-edge scenario at the end of 2021, when the U.K. benchmark will likely retire.

In New York, the bill would allow contracts to instead use the replacement rate recommended by the Fed Board, New York Fed, or the ARRC. The proposal includes language providing some safety measures, allowing the use of the replacement rate only in situations where it is reasonable and comparable to Libor.

The replacement benchmark should not “prejudice, impair, or affect any person’s rights or obligations under or in respect of any contract, security or instrument,” according to the bill language.

Policy is often negotiated alongside fiscal plans in the New York state budget process, which is kicked off by the governor. The final budget deal is due by March 31, the end of the state’s fiscal year. The Libor discontinuation legislation would take effect immediately after the passage of the budget, according to the bill language.

“It’s an important first step,” said Priya Misra, head of global rates strategy at TD Securities in New York, and also a member of the ARRC. “Hopefully it passes in the New York legislature and then can become a template for other states, too.”

Do You Consider Bitcoin As A Hedge Against A Rigged And Failing Financial System?

Updated: 1-1-2021

Finance Executives Look To Advance Libor Transition In 2021

The interest-rate benchmark is being phased out, forcing companies to update contracts and adjust funding projections.

Efforts to skip the London interbank offered rate for new transactions by end of next year are forcing finance executives to take stock of their contracts, communicate with banks and investors and adjust their interest-rate cost calculations.

Global policy makers decided to do away with Libor, an interest-rate benchmark underpinning trillions of dollars worth of financial instruments, after concluding it was prone to manipulation. Banks face a Dec. 31, 2021, deadline to replace Libor with alternative rates for new contracts following a yearslong transition effort.

A majority of financial and nonfinancial companies recently said their Libor transition plans are ahead of schedule, according to a survey by consulting firm Accenture PLC released earlier this month. In some cases though, the pandemic has caused delays.

Corporations including Walt Disney Co. , network-equipment maker Juniper Networks Inc. and cancer treatment firm Varian Medical Systems Inc. have started alerting investors to the pending changes and the potential challenges as they shift to a new rate regime.

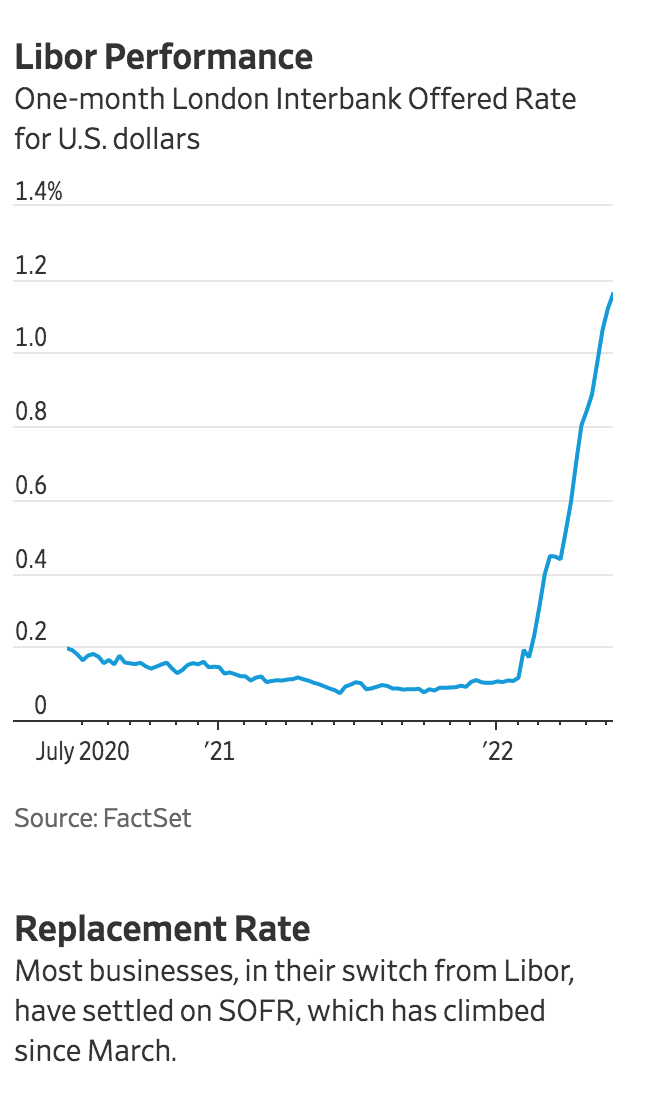

Businesses face potential adjustments to interest costs, arising from Libor being calculated differently than its likely successor in the U.S., the Secured Overnight Financing Rate, or SOFR.

For one, the immediate cost of borrowing may be cheaper. While Libor is derived from daily price quotes provided by a panel of banks, SOFR is based on the cost of transactions in the market for overnight repurchase agreements, or repos. Financial companies already use the repo rate to borrow cash, using U.S. government bonds as collateral. SOFR is considered a less risky rate, which means overall interest costs for companies could be lower than under Libor.

But SOFR currently doesn’t allow for predictive, forward-looking rate calculations, a notable deviation from Libor, which can be calculated three, six or 12 months out. This limits the insight treasurers can glean into future interest-rate costs.

Timken Co. ’s Chief Financial Officer Philip Fracassa is working to ensure that the North Canton, Ohio-based maker of engineered bearings and power-transmission products shifts its contracts to SOFR. “The discontinuation of Libor requires a lot of restructuring of debt agreements,” Mr. Fracassa said.

He doesn’t expect big changes to Timken’s interest costs as part of the transition, but foresees additional paperwork, including updating contracts and policies. “There’s a lot that you’ve got to do,” he said.

Finance executives also need to deal with existing contracts that cite Libor. That can be tricky—especially in cases where some of these debt instruments are held by hundreds of investors who all need to agree to the changes. Transaction lawyers suggest that finance chiefs create an inventory of agreements that reference Libor, and take a look at when they run out and who the other party is. The cut-off date for existing contracts to stop referencing Libor is June 30, 2023.

“The issue for treasurers and CFOs is managing the transition across the whole company,” said Michele Navazio, a partner at law firm Seward & Kissel LLP. “It is not going to happen simultaneously, which could add to the complications.”

Serena Wolfe, CFO at Annaly Capital Management Inc., a New York-based mortgage real-estate investment trust, hopes legislators will make it easier for companies to deal with some of these legacy contracts. A potential fix for certain residential credit securitizations currently is being debated by New York state lawmakers.

Annaly Capital has a Libor working group, which found that recent upgrades to the company’s technology systems will make it easier to manage the data required to transition away from Libor, Ms. Wolfe said. Other companies, especially those still relying on manual data entry and Microsoft Excel, could find that harder, she said.

Dealing with two benchmark rates—SOFR for new contracts after Dec. 31, 2021, and Libor for legacy contracts until June 30, 2023—won’t be a problem for Annaly Capital, Ms. Wolfe said, adding that the company already holds swaps which cite different rates.

For some businesses though, the dual rates will present a challenge, said Venetia Woo, lead Libor adviser at Accenture. “Corporates now have two expiration dates for Libor contracts and they need to determine if the economics to convert [by year-end] outweigh the burden of running two operations,” she said.

Updated: 1-11-2021

Libor Proving Hard To Kill In $200 Trillion Derivatives Market

It’s one of the most confounding questions facing regulators in the fight to phase out the London interbank offered rate.

How do you wean everyone from asset managers and traders to corporate treasurers off derivatives that are so ubiquitous, they’ve become part of the fabric of the financial system?

For the better part of three years, U.S. officials have been preaching patience. Libor-based interest-rate swaps, futures and options, among the most liquid markets in the world, would gradually give way to new securities tied to new benchmarks, they said, including the Secured Overnight Financing Rate, dollar Libor’s anointed successor.

Yet activity in those markets isn’t disappearing. What’s more, acceptance of alternative products has been slow. While some headway has been made, average open interest in three-month SOFR futures barely topped 5% that of eurodollar contracts last month. And recent high-profile milestones in the Libor transition that were expected to jump-start trading in the new instruments have delivered relatively modest boosts so far.

As the Federal Reserve’s year-end deadline to halt new Libor contracts creeps closer, some are beginning to express concern that the slow pace of progress could undermine efforts to ensure a smooth transition, posing a risk to financial stability.

While few expect a delay similar to the one announced in November for legacy contracts that can’t be shifted to SOFR, it’s another example of the difficulties regulators have had in getting critical corners of the financial world on board.

“We’re in this classic chicken-and-egg scenario, where participants don’t want to trade because liquidity is low, but there’s not going to be enough liquidity unless people trade it,” Thomas Pluta, global head of linear rates at JPMorgan Securities, said of SOFR derivatives. “It’s increasing, but quite frankly there’s an awful lot more that needs to be done for this transition to happen.”

More than $200 trillion of financial instruments globally are tied to dollar Libor, with the vast bulk of that exposure in the form of derivative contracts, according to the Bank for International Settlements. The products are used by money managers to bet on the direction of monetary policy and corporations to hedge their interest-rate exposure.

Some market watchers predict the shift to SOFR derivatives will ramp up in the coming months after the Fed made clear late last year that it still expects banks and other regulated firms to stop entering into new Libor-based transactions by the end of 2021.

“That will force the issue quite a bit,” said Tyler Wellensiek, a managing director in rates sales at Barclays Plc. Nonetheless, she acknowledged that “there’s definitely a lot more work to do in SOFR liquidity.”

Officials at the Alternative Reference Rates Committee — the Fed-backed group tasked with overseeing the Libor transition in the U.S. — point to the gradual increase in SOFR activity across the swaps curve since the middle of last year as evidence that the benchmark is gaining traction among derivatives traders.

“The depth of liquidity has improved a lot,” said Tom Wipf, ARRC chair and a vice chairman of institutional securities at Morgan Stanley.

Add to that another potential boost in activity in the coming months with the setting of the International Swaps and Derivatives Association’s spread adjustment — used to determine fallback rates for Libor contracts maturing after the benchmark is phased out — and SOFR’s proponents see reasons to be encouraged.

Curve Delay

Still, there’s no guarantee the fixing of the spread adjustment will spark a surge in trading.

Other recent milestones in the Libor transition, including the so-called big bang shift by derivatives exchanges to SOFR for calculating the value swaps, and ISDA’s publication of a highly anticipated legal protocol to help convert Libor-linked contracts to SOFR, have produced relatively fleeting boosts so far.

Just 5.6% of all U.S. dollar risk in cleared over-the-counter and exchanged-traded interest-rate derivative transactions was tied to SOFR in November, according to data from ISDA and Clarus Financial Technology. While that’s almost double the 3% of trading activity that referenced the rate in June, it’s well off the record 9.7% reached in October, when global clearing houses made the shift to SOFR.

JPMorgan’s Pluta said he had expected the big bang to be “a catalyst for lots of different market participants to start trading SOFR actively,” but “many participants just did what they needed to do, and then reverted for the most part to Libor.”

Should the shift to SOFR derivatives struggle to gain pace in 2021, it could delay the ARRC’s ability to develop a forward-looking term reference rate, according to Marcus Burnett, the director of SOFR Academy, an education technology firm whose clients include banks and asset managers.

That may in turn discourage underwriters and issuers in the loan market from pricing new deals based off of the alternative benchmark.

“Without that, it’s less likely that we’re going to have a robust liquid and institutional-sized lending market based on SOFR,” Burnett said. “Without the lending market, we can’t have a broad-based transition.”

Some are already concerned that it could threaten the orderly functioning of markets.

“On some level it has to have implications for financial stability because of the uncertainty it generates,” Anne Beaumont, a partner at law firm Friedman Kaplan Seiler & Adelman in New York, said of SOFR’s modest progress so far. “You’re already going to have this fragmented world of new instruments linked to SOFR and legacy ones that rely on fallbacks.”

While recent jumps in SOFR trading that coincided with transition milestones have proven that banks can scale up their execution, the data suggest many likely aren’t seeing significant demand from clients for SOFR transactions and risk management, according to Chris Barnes, a senior vice president at Clarus.

SOFR still needs to gain significant traction to ensure a smooth transition, he said, especially with the possibility looming that the Fed will limit trading of Libor-linked derivatives in less than a year.

“Twelve months is an incredibly short period of time to try and change the precise product that people are trading,” Barnes said. But “if we as a market, as an industry can’t get behind a change in four years, that’s not a great sign.”

Updated: 3-9-2021

Libor Is Going Away For Real

Libor Is Canceled

I Guess They Were Serious About That, Huh:

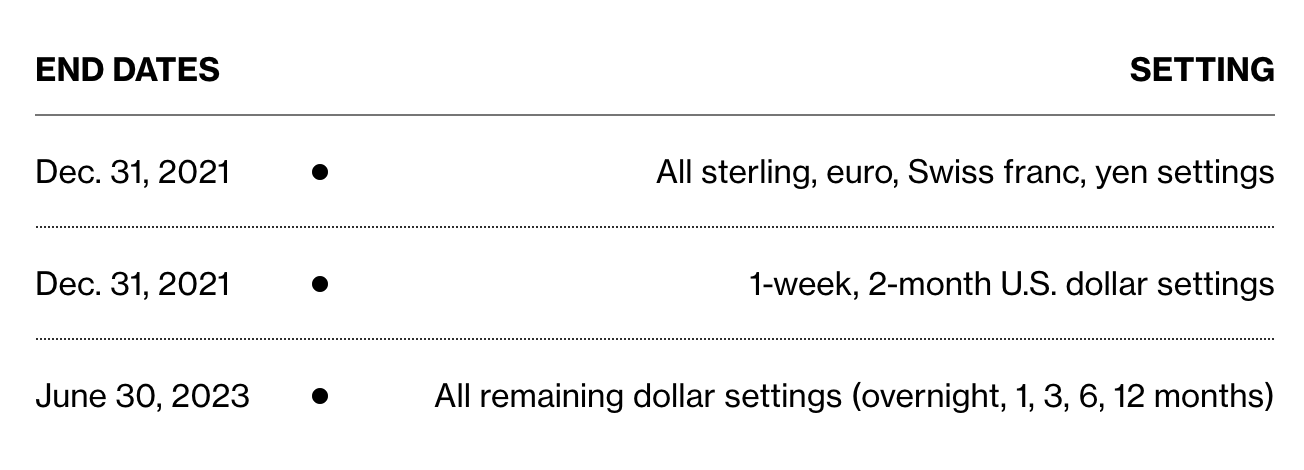

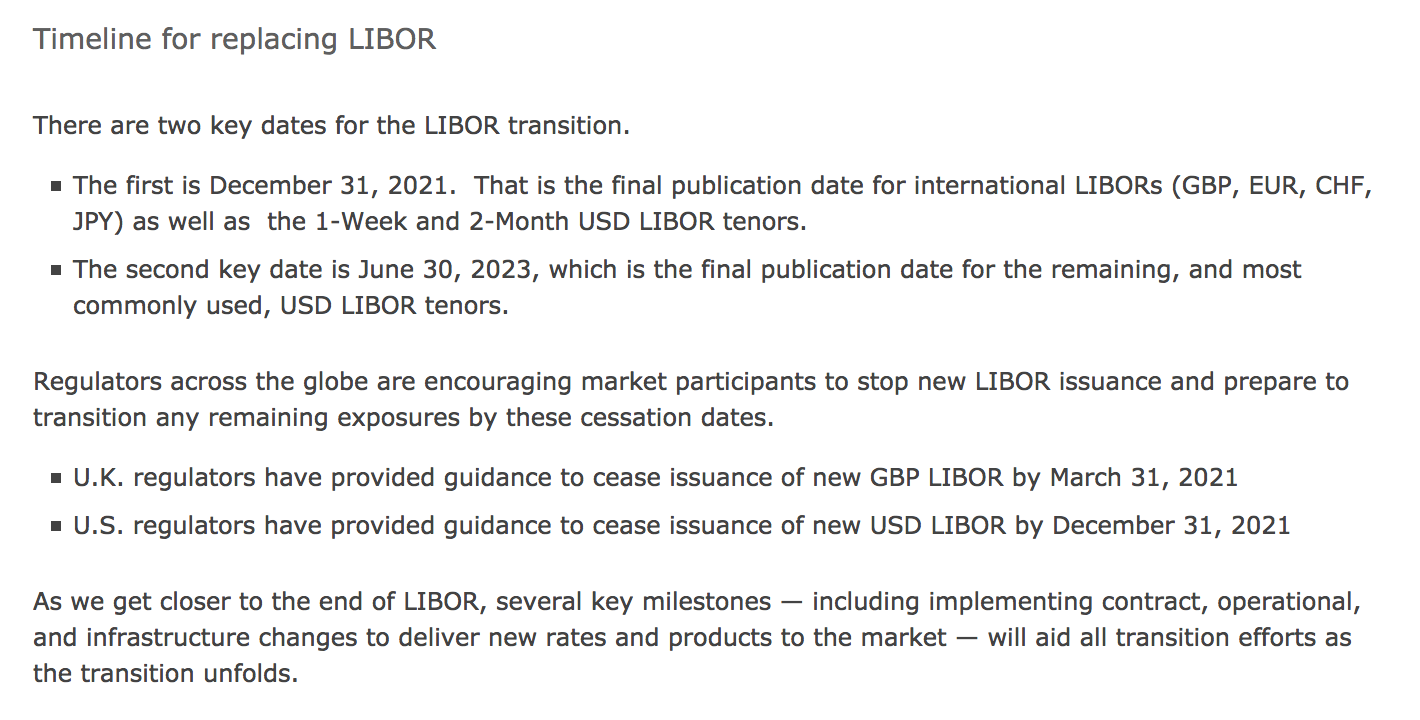

* Regulators kicked off the final countdown for the London interbank offered rate Friday, ordering banks to be ready for the end of a much maligned benchmark that’s been at the heart of the international financial system for decades.

* The U.K. Financial Conduct Authority confirmed that the final fixings for most rates will take place at end of this year, with just a few key dollar tenors set to linger for a further 18 months.

Here is the FCA’s announcement, and here is one from Intercontinental Exchange Inc., which actually administers Libor.

And here are two announcements—“LIBOR Cessation and the Impact on Fallbacks” and “ISDA Statement on UK FCA LIBOR Announcement”—from the International Swaps and Derivatives Association, which administers the market for interest rate derivatives.

One thing that is happening here is that ICE will stop calling up banks every day and asking them “at what rate can you borrow unsecured from other banks” and then using their answers to calculate Libor. That’s what ICE does now, and what the British Bankers’ Association did before ICE. It has become an increasingly untenable way to calculate an interest-rate benchmark, insofar as:

(1) the banks were lying about their borrowing costs for a while and

(2) the interbank unsecured funding market is a lot less robust than it was back before the financial crisis, so it’s hard to answer that question truthfully even if you’re trying to. So, at the end of the year, it will mostly stop, though it will keep going for the main tenors of U.S. dollar Libor until June 2023.

Another thing that is happening here is that ICE will stop publishing Libor, sort of. Actually it will keep publishing some Libor rates for a while after it stops collecting them, though with an asterisk. (The asterisk says that the new Libors will not be “representative.”)

They will be “synthetic” Libor: Instead of being based on a poll of banks’ borrowing costs, the new rates will be computed based on “a forward-looking term rate version of the relevant risk-free rate plus a fixed spread aligned with the spreads in ISDA’s IBOR fallbacks.”

In the U.S., for instance, Libor is supposed to be replaced by SOFR, the Secured Overnight Financing Rate, a risk-free rate based on the cost of borrowing secured by U.S. Treasuries. When Libor is replaced by “synthetic Libor,” the synthetic Libor will be:

(1) SOFR,

(2) compounded in arrears to get a term rate,

(3) plus a spread.

The spreads are based on the historical differences between Libor and the relevant risk-free rate; here they are. 1 So for instance when ICE stops polling banks for 3-month U.S. dollar Libor, 3-month dollar “synthetic Libor” will just be SOFR, compounded for three months, plus 0.26161%.

I have written before that Libor is a “function call”: You write in a contract that the interest rate will be Libor, and then you go and pull Libor in from ICE (or from a Bloomberg page that gets it from ICE), and you don’t really care about the guts of how ICE calculates Libor. Right now ICE calculates Libor through this rickety mechanism of calling up banks and asking them to make up numbers.

In the future it will calculate Libor by looking at published risk-free rates—which benchmark administrators calculate by looking at real transactions in secured funding markets—and adding a number to them.

In theory Libor could just keep going forever, in this vestigial way: The “real” benchmark would be SOFR or whatever, and then Libor would just be a minor arithmetic manipulation of SOFR, SOFR plus 0.26%. You could still write loans or derivatives that reference Libor, and everyone would know that “Libor” is a weird archaism for “SOFR plus 0.26%.”

But The Regulators Don’t Want That Either:

* The BOE will hold executives to account for progress in the transition under the U.K.’s regulatory regime for senior managers, according to people familiar with the matter. If firms fail to take appropriate steps, there is the potential for measures such as capital sanctions, though these would come further down the line.

* Progress toward replacement benchmarks, such as the Secured Overnight Financing Rate in the U.S. and the Tokyo Overnight Average Rate in Japan, has been sluggish, and there are hopes Friday’s announcement could accelerate the process — particularly in the vast global derivatives market. …

* The Fed, for its part, is intensifying its scrutiny of banks’ efforts to shed their reliance on Libor, and has begun compiling more detailed evidence on their progress.

* “In the months ahead, supervisors will focus on ensuring that firms are managing the remaining transition risks,” said Randal Quarles, vice chair for supervision at the Federal Reserve Board and chair of the Financial Stability Board.

We’ve had several years now of regulators saying “you have to stop using Libor,” and Libor is still pretty popular, but maybe this will do it. I wonder if old-school bankers will cling to Libor in a sort of hipsterish way.

Maybe the senior banker will say “ah yeah their term loan is at Libor plus 50” and the analyst will be confused and go back to her desk and ask the associate “hey what does Libor plus 50 mean” and the associate will be like “it means SOFR plus 76, that’s just how people talk sometimes.”

Updated: 3-11-2021

Why Won’t Libor Die? It’s Complicated

The broken interest rate benchmark still dominates derivatives trading. Regulators may need to be more forceful in persuading banks to drop it.

The funeral dates for Libor are finally set, with some sensible concessions that keep part of the suite of interest rates alive for longer than initially planned. Those exemptions must be strictly controlled so as not to impede a much broader acceptance of the replacement benchmarks. For now, that’s proving harder than even those most resistant to change might have expected. So market regulators need to step up efforts to force bankers and financiers to embrace Libor’s successors.

The London interbank offered rates fell into disrepute for being easily rigged by the traders charged with submitting borrowing costs. Plus, the underlying wholesale funding market they’re based on melted away during the global financial crisis. In mid-2017, the U.K.’s Financial Conduct Authority said they’d be phased out by the end of 2021.

Since then, different alternatives have been created for different markets. In dollars, the replacement rate is the Secured Overnight Financing Rate, known as SOFR. In the U.K. markets, it’s the Sterling Overnight Index Average, dubbed Sonia. But the switch has been very, very slow, increasing the risk that a last-minute scramble to adapt to the changeover could lead to unwanted and potentially costly market distortions.

Just 10% of the total risk in the global market for interest-rate derivatives was tied to the replacement rates in both December and January, according to figures compiled by the International Swaps and Derivatives Association. Although the 2020 monthly average of 7.8% was an improvement on 2019’s 4.7%, the percentage peaked at 11.6% in October.

Those figures mask important regional differences. In the year ended Feb. 26, the notional value of trades in dollar-denominated interest-rate derivatives tied to Libor was more than $20.8 trillion, dwarfing the $472 billion that referenced SOFR, according to ISDA data. U.S. swap traders still haven’t kicked their Libor addiction. But figures for January suggest the U.K. regulator’s efforts to encourage sterling traders to switch to the new interest-rate flavor are showing signs of success.

Even in sterling, though, the most active market remains beholden to Libor. Just 20% of the risk traders took in three-month interest-rate futures was connected to Sonia rather than Libor in January, according to Intercontinental Exchange Inc.

Beyond the excuse of inertia, the market’s caution in adopting the new benchmarks is understandable. The replacement rates are based on overnight lending, which has made it tricky to calculate the matrix of different maturities to match Libor.

Moreover, speculation that some of the more important rates might get a stay of execution proved correct. While the bulk of the Libor spectrum will be phased out at the end of this year, the key one-, three-, six- and 12-month dollar rates will survive until mid-2023, allowing the bulk of existing financial contracts to mature without needing to be changed. That’s a smart concession to market reality.

The FCA estimates the value of outstanding financial contracts that still reference Libor is about $260 trillion, with cleared interest-rate swaps and exchange-traded derivatives accounting for about 80% of that total. The figure, though, excludes the bond, loan and mortgage markets.

And those are where life gets trickier. The FCA is considering allowing synthetic Libors — based on the new rates but adjusted for maturity and with an added credit spread — to take the contractual place of the current rate in contracts that can’t easily be switched to the replacement benchmarks. It’s a legal sleight of hand that slides the new borrowing costs into existing contracts, covering hard-to-adjust legacy documentation that might not even surface until after Libor’s demise.

But regulators should take a hard line on restricting what qualifies for that special treatment, otherwise firms will have an excuse not to make the change and Libor will linger on indefinitely. Banning new contracts from referencing Libor was a good start, but forcing banks and insurers to list their exposures to the old benchmark by category would do wonders.

It would focus attention on the need to revise the terms of those trillions of dollars of outstanding obligations. Goldman Sachs Group Inc. for example, said this week that it’s still deciding how to deal with about $29 billion of Libor-linked bonds and preferred shares that run past Libor’s expiry date.

With the FCA’s final timetable for Libor’s endgame, regulators will be hoping the pace of adoption of the new reference rates accelerates. If it doesn’t, more stick might be needed to shift market players out of the status quo. Enlightened self-interest would suggest it’s time to euthanize Libor.

Updated: 3-21-2021

Libor Wall Street Fix Gets A Boost As N.Y. Senator Backs Move

A key New York state lawmaker is supporting legislation intended to protect hundreds of billions of dollars of contracts from legal chaos when Libor is phased out as an interest-rate benchmark, marking a potentially crucial step toward securing its passage.

Democrat Senator Liz Krueger, the head of the finance committee, said in an interview that she is in favor of provisions contained in Governor Andrew Cuomo’s proposed budget that would allow existing contracts to use replacement indexes recommended by regulators. She said failing to enact that could give large companies power to impose their own changes instead, potentially to the peril of consumers.

Bankers, investors and regulators see such proposals — which will help troublesome Libor-linked contracts switch to replacement rates — as crucial to ensuring that a large swath of the global financial system isn’t disrupted.

Krueger’s support matters because she previously challenged similar reforms proposed by the Alternative Reference Rates Committee, the Federal Reserve-backed body guiding the transition, on the grounds that they could put retail consumers at a disadvantage.

Krueger said in the interview that she has thoroughly examined the plan in Cuomo’s budget and concluded it is “legitimate” and adequately protects consumers. The deadline for passing the budget is April 1.

“It still needs to be negotiated,” she said, adding that she’s hopeful it will make it into the final budget.

While most Libor indexes will be retired at year-end, various tenors of the dollar-denominated benchmark may be given a reprieve from the phase out until mid-2023, in part to allow older contracts that lack a clear replacement rate to expire naturally.

While that would help reduce the threat to financial stability, the most challenging floating-rate debt and securitizations — as well as Libor-based mortgages and student loans — will be in place after Libor is no longer used, making legislation critical.

Backing from the committee head makes the law more likely to pass, according to Priya Misra, global head of interest rate strategy at TD Securities and a member of the ARRC, the Fed-backed transition planning group.

“We are down to the wire with the New York state legislation and it is extremely important to address the problem of legacy cash products with inappropriate fallback language,” she said. Passing the law “would be a win-win since it helps bring clarity for issuers and investors.”

Tom Wipf, vice chairman of institutional securities at Morgan Stanley and chairman of the ARRC, said the body “welcomes all support for the legislation, which is essential to providing legal certainty and financial stability.”

Lawyers say even if the law passes, separate legislation is likely to be needed to protect sections of the market that fall beyond Wall Street. Federal Reserve Chair Jerome Powell said in February that national legislation would be the best solution.

“Once you have legislation in New York, you have a template that other states can piggy back off and hopefully even have a federal legislative solution,” said Y. Daphne Coelho-Adam, a counsel at Seward & Kissel LLP. “It gives everyone ability to look forward without hitting that wall or going off a cliff.”

Libor Enters ‘Final Chapter’ As Global Regulators Set End Dates

Regulators kicked off the final countdown for the London interbank offered rate Friday, ordering banks to be ready for the end of a much maligned benchmark that’s been at the heart of the international financial system for decades.

The U.K. Financial Conduct Authority confirmed that the final fixings for most rates will take place at end of this year, with just a few key dollar tenors set to linger for a further 18 months.

The move comes in the wake of major manipulation scandals and the drying up of trading used to inform the rates, which are linked to everything from credit cards to leveraged loans. Global regulators have made a concerted effort to wind down the benchmark in 2021, with the Federal Reserve and others pushing market participants toward a slew of alternatives.

“Outside the U.S. dollar markets, this marks the end game,” said Claude Brown, a partner at Reed Smith LLP in London.

“The rate that linked the world, and then shocked the world, will leave this world in 2021.”

Libor is deeply embedded in financial markets. Some $200 trillion of derivatives are tied to the U.S. dollar benchmark alone and most major global banks will spend more than $100 million this year preparing for the switch. Other players — from corporations to hedge funds — will also be affected, with many only beginning to shift from legacy contracts.

Bank of England Governor Andrew Bailey said this was now the “final chapter,” and there’s no excuse for delays.

The BOE will hold executives to account for progress in the transition under the U.K.’s regulatory regime for senior managers, according to people familiar with the matter. If firms fail to take appropriate steps, there is the potential for measures such as capital sanctions, though these would come further down the line.

Progress toward replacement benchmarks, such as the Secured Overnight Financing Rate in the U.S. and the Tokyo Overnight Average Rate in Japan, has been sluggish, and there are hopes Friday’s announcement could accelerate the process — particularly in the vast global derivatives market.

“This was the much anticipated final piece of clarity the market needed to really kick on,” said Kari Hallgrimsson, co-head of EMEA rates at JPMorgan Chase & Co. “We would expect liquidity for trading the new rates to keep increasing from here on out.”